Recently, international news has been dominated by the Iran situation and Trump's erratic stance on the war's direction.

Yet one event, which dominated headlines in 2025, is now rarely mentioned by mainstream media—on February 14, due to a deadlock between Democrats and Republicans over the Department of Homeland Security (DHS) funding bill, a partial shutdown of the DHS officially began.

As of now, the shutdown has not ended.

During this nearly two-month shutdown, over 100,000 DHS employees have been unable to receive their salaries, and nearly 11% of Transportation Security Administration (TSA) employees have been absent. In New Orleans, passengers waiting for security checks have formed lines winding from inside the terminal to the outdoors, even looping seven times in the parking lot before reaching the entrance.

For the United States, which has almost no high-speed rail network and relies heavily on air travel, disruptions to the civil aviation system are crippling. Even Elon Musk publicly offered to pay the salaries of affected TSA employees out of his own pocket.

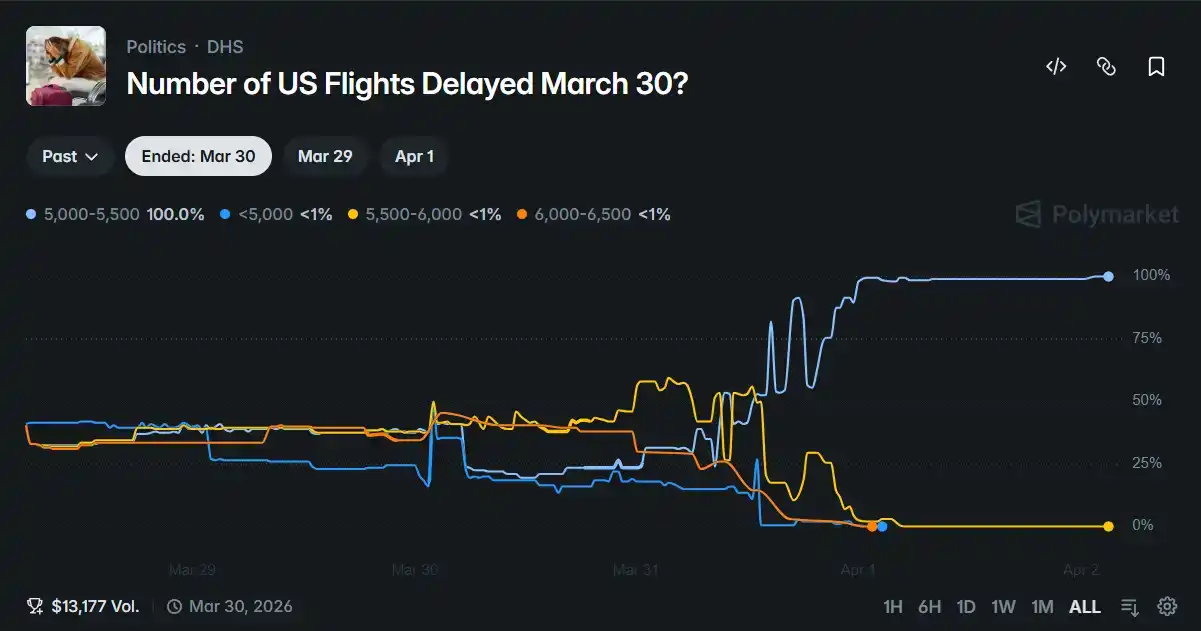

Also starting in March, the prediction market Polymarket launched a weekly updated prediction event for "number of U.S. flight delays this week"—traders can bet on how many flights will be delayed each week; predicting correctly earns money, while predicting wrong results in a total loss.

Beyond such purely entertainment-focused events, Polymarket has also listed several topics with considerable reference value. Through the probabilities reflected by these topics, we can attempt to interpret the true current state of the government shutdown and even U.S. domestic affairs.

The Shutdown Game Between the Two Parties

The duration of this shutdown has already broken the previous record of 35 days set by Trump. Amid the widespread flight delays and the near-collapse of the security screening system, when the shutdown will end is the most pressing question for those affected within the United States.

Polymarket currently has a related event: "DHS shutdown will end by ___." As of the time of writing, the probability of the shutdown ending between April 5 and 8 is 44%, while the probability that it will not end in April is 14%.

Betting on these two time nodes are many "smart money" traders—seasoned participants with high past prediction accuracy and strong profitability in the political sector. Behind such trading profiles lies a clear logic: if the shutdown does not end during the window of April 5 to 8, the likelihood of reaching an agreement within the month will significantly decrease.

April 5 to 8 coincides with Congress returning from recess, when both parties will once again place the funding bill on the table. If an agreement can be reached within a few days after returning, and the bill passes both the House and Senate before being signed, the shutdown will end.

However, if this window is missed again, the House and Senate will subsequently become engrossed in other agenda items. Without strong political pressure, the motivation for the two parties to return to the negotiating table will greatly diminish.

Musk's "Offer to Pay" and ICE's "Filling In"

Due to continuous TSA employee resignations causing severe delays at major airports, Elon Musk stated on March 21 that he was willing to pay TSA personnel's salaries, which led to the Polymarket trading event "Will Musk pay TSA employees' salaries?".

However, shortly after Musk's post, the White House declined the offer citing legal compliance and conflict of interest concerns: according to U.S. federal law, government employees cannot accept external compensation related to their official duties;加之 Musk's deep involvement in federal government contracts, direct payment of salaries faces serious conflict of interest challenges.

Although the refusal was legally justified, ordinary people still need to make a living. To minimize the impact of the aviation system's paralysis on the midterm elections, Trump ordered the deployment of Immigration and Customs Enforcement (ICE) agents to airports in March to replace TSA employees who had left due to unpaid salaries.

But the scene that unfolded once these ICE agents entered the airports made the entire shutdown event seem even more absurd.

After Trump took office, ICE, to meet the goal of "arresting 3,000 people daily and deporting a million people annually," has been drastically compressing recruitment and training processes—planning to hire ten thousand additional law enforcement officers and shortening the originally scheduled 16 weeks of in-person training to 8 weeks.

In short, the professional competence of these ICE agents themselves is already questionable.

TSA security work requires systematic training, covering core skills such as X-ray machine operation and explosive detection, for which ICE agents simply lack the qualifications.

Thus, a historic scene unfolded: TSA employees, while working unpaid, had to demonstrate security procedures to ICE agents and teach them how to maintain order. Most ICE agents did not actually conduct security checks but instead patrolled the terminals, using their law enforcement status to question and deport suspected illegal immigrants.

Data confirms the outcome of this farce: after ICE's deployment to airports, flight delay conditions did not significantly improve. By the end of March, the U.S. aviation system still experienced thousands of daily flight delays, with Atlanta Airport's TSA absenteeism rate nearing 40% and single-day flight delays exceeding 350. These numbers indicate that these ICE agents, who were supposed to act as a buffer for the shutdown, did not serve any expected purpose.

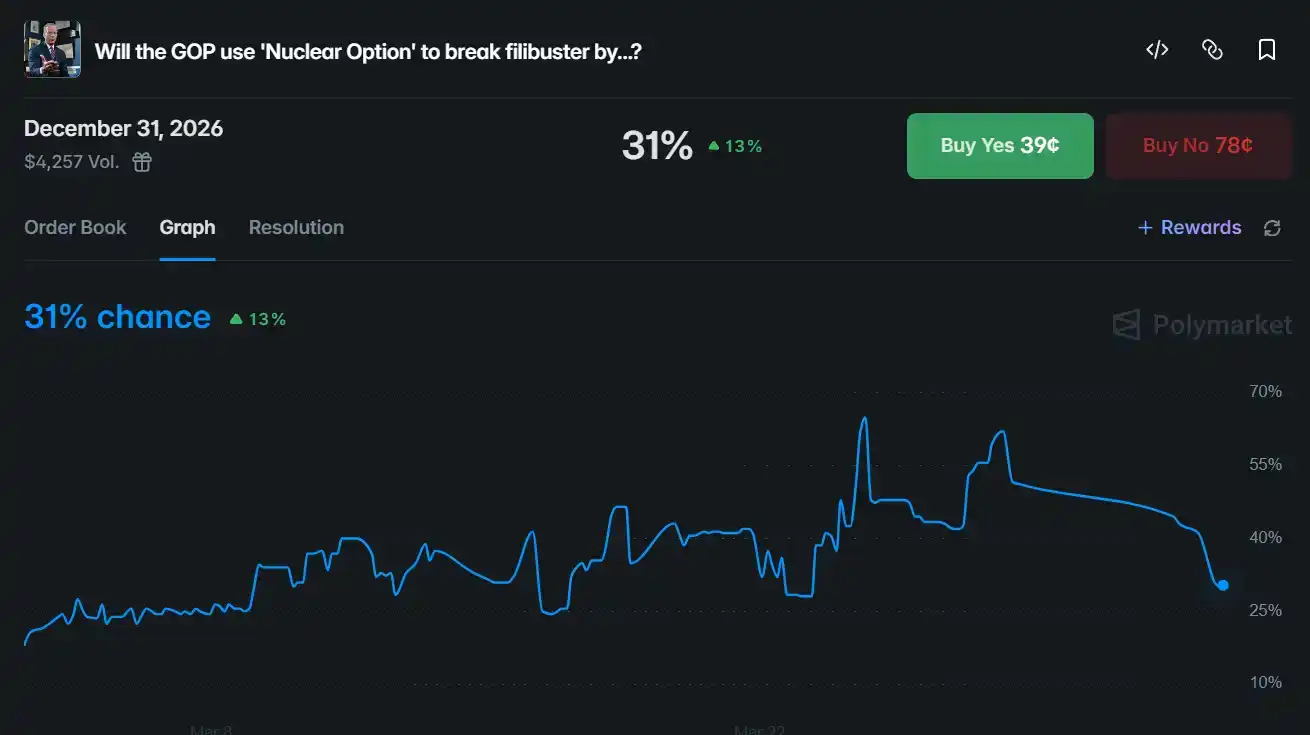

The "Nuclear Option" to Break the Deadlock

Another trading event related to this government shutdown is "Will Republicans use the 'nuclear option' to break the filibuster before December 31, 2026?", with a current probability of 31%.

At first glance, the term "nuclear option" sounds intimidating; but in U.S. politics, it is not a literal nuclear weapon but rather one of the few yet highly destructive procedural trump cards available to Republicans.

In the U.S. legislative system, the House of Representatives is responsible for proposing and drafting appropriations bills, while the Senate is responsible for deliberation and voting. Typically, ending debate and proceeding to a vote in the Senate requires 60 votes—this means the minority party needs only 41 votes to block any bill by indefinitely prolonging debate through a filibuster.

The "nuclear option" provides a path to bypass this threshold: a senator raises a procedural appeal, and a simple majority (51 votes) overrules the presiding officer's decision, thereby forcibly lowering the vote threshold required to end debate from 60 votes.

Currently, Senate Republicans hold 53 seats; once the nuclear option is triggered, the Democrats' ability to obstruct will be nearly zero.

But the reason the "nuclear option" is called "nuclear" lies in the high cost it imposes on the user:破坏 Senate rules会被选民视为滥用权力; more crucially,一旦共和党未来失去多数席位, the same rules could be used by Democrats for retaliation.

The pit dug today might be filled by oneself tomorrow. The 31% probability is the market's true pricing of this dilemma.

Even as this shutdown deadlock remains unresolved, Trump must simultaneously deal with the escalating situation with Iran.

On one side is the high-pressure game of diplomacy and military action, on the other are airport lines, unpaid wages, and partisan bickering—the troubles this U.S. administration needs to manage simultaneously are far greater than what headlines suggest. Crises in domestic and foreign affairs never wait for the other to be resolved first.

Amid such turmoil, the rich array of political and current events prediction events on prediction markets will continue to serve as an objective mirror, helping us capture the true trajectory of these narratives.