Author: Ching Tseng

Compiled by: Deep Tide TechFlow

Deep Tide Guide: Investor Ching Tseng categorizes crypto companies into four quadrants: crypto-native/traditional finance-oriented, with traction/without traction. In 2025, 84.7% of 118 token issuances broke their issue price. Crypto-native projects without traction are massively destroying capital, while traditional finance-oriented companies with traction are capturing the $18 billion RWA market. This article clarifies where the money is flowing and which tokenomics models have failed.

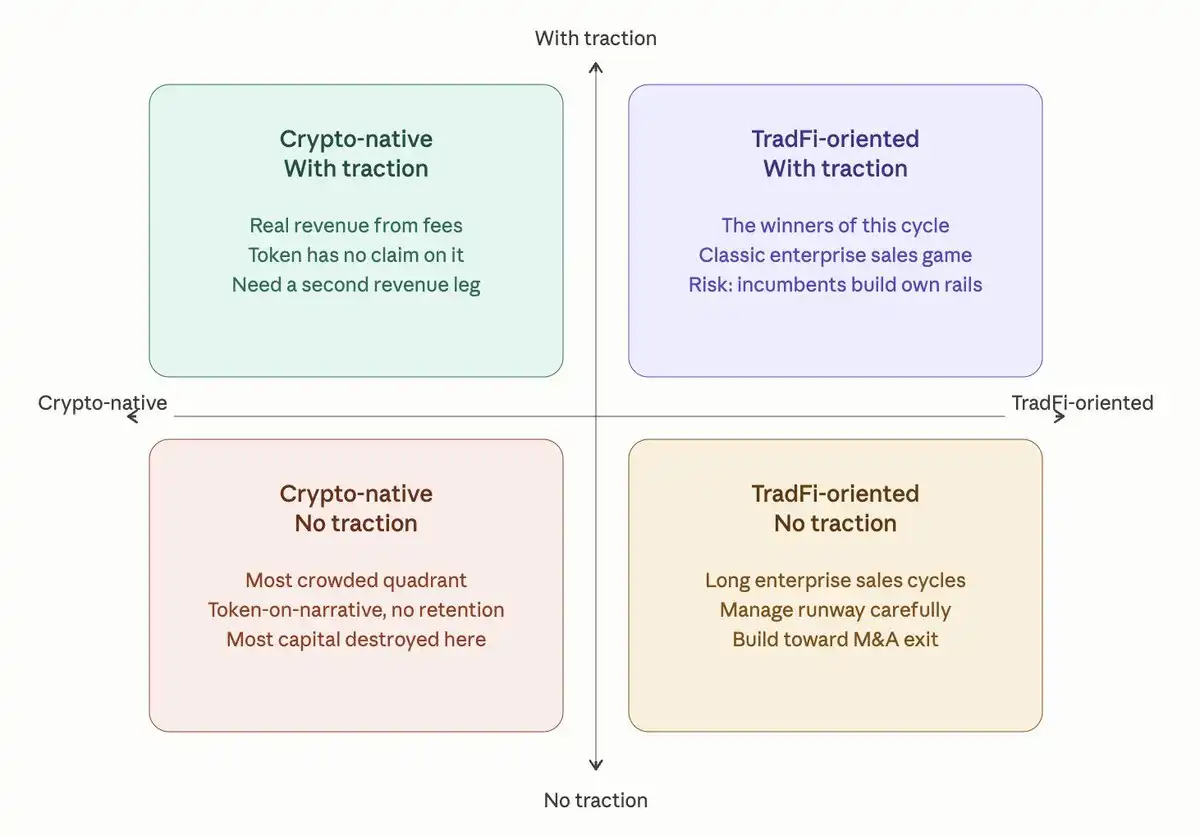

Sitting on the investor side this year, I found that almost every crypto founder I met can be classified into one of four categories. The two axes are simple: crypto-native vs. traditional finance-oriented, with traction vs. without traction. Four quadrants, covering about 75% of the market.

The challenges faced by each quadrant are completely different. Here is my breakdown.

Crypto-Native, Without Traction

This is the most crowded quadrant and the area where capital is being destroyed most severely.

These teams are still showcasing TVL numbers that were inflated in the last cycle but cannot explain why they worked back then. They ask for valuations of $20 million, $30 million, sometimes even $200 million, with only a utility token and a roadmap, claiming the token has a "clear use case" because it is used to pay fees or for governance voting.

The data is brutal. Among the 118 token issuances tracked in 2025, 84.7% fell below their issue price, with the median fully diluted valuation dropping by 71%. Some of the most hyped "native DeFi L1s" of this cycle saw their TVL drop by over 90% in the first year after launch, with tokens following a similar trend. AI-related token groups saw an average annual return of -50%, with several top performers of 2024 pulling back over 80% from their peaks.

The pattern is consistent. Initial traction comes from users seeking quick profits rather than genuinely liking your product. Tokens priced based on narratives, without revenue or user retention to support their valuations, bled in 2025. Massive emissions exposed that on-chain activity was primarily mercenary behavior.

What this quadrant needs to internalize is: the long-term value of a token comes from the team's ability to generate revenue and return capital to holders, not from artificial utility that forces users to spend it. Regulation still prevents anyone from publicly saying "the token is equity," but empirically, that is the only model that works. Everything else is, at best, a cyclical trade.

If you are here, the honest approach is not to issue another token. It is to return to the basics: who are your real users, what are they willing to pay for, and how can you capture a portion of that?

Crypto-Native, With Traction

This quadrant is full of teams that built something real many years ago, often in the last cycle, and have been quietly earning decent revenue from trading, lending, or exchange fees. The teams are small, cash flow covers salaries, and the product works.

Sounds good? But they also have challenges to overcome.

Most issued tokens early and are now stuck with a structural problem: revenue exists, but the token has no mechanical claim to it. Some of the largest products in the market handle monthly trading volumes of tens or even hundreds of millions of dollars, but for years the direct value captured by the token has been zero. No matter how good the revenue/profits are, the market does not truly trade the token at a consistent multiple; the market prices expected growth, not current economic conditions.

The buyback debate is the other half of the story for this quadrant. Some protocols that promised weekly fee-funded buybacks in early 2025 saw their prices rise over 40% in the following month. Others running automated, fee-funded buyback programs cumulatively bought back over $1 billion in tokens within seven months, with single-day buybacks nearing $4 million at their peak. DeFi buybacks totaled approximately $2 billion in 2024-2025.

Buybacks sound like the answer. Sometimes they are. But for teams in this quadrant without excess revenue, buying back tokens is just burning future runway to defend a price that may not hold. The harder and better question is, can you grow a second revenue line not tied to crypto volatility? Because if traditional finance-oriented competitors build better distribution into institutions while you are still surviving on altcoin traders, your moat will quickly turn into commodity-priced infrastructure.

Traditional Finance-Oriented, Without Traction

This group ballooned in 2024-2025. Custody tools, compliance middleware, tokenization rails, on-chain forex, institutional settlement—all genuinely useful. All expensive. All have enterprise sales cycles measured in quarters, not weeks.

The problem is not the product. It's the math. Founders raised $15 million to $30 million assuming institutions would come, but even onboarding a tier-1 bank client can take 12-18 months and requires compliance infrastructure that eats a year of burn before the first dollar of revenue lands.

The good news is that the exit environment for this quadrant is exceptionally healthy. Crypto M&A hit a record $8.6 billion in 2025, with over 140 VC-backed crypto companies acquired, a 59% jump year-over-year. Several of the largest deals saw existing giants paying hundreds of millions to billions of dollars for distribution, licenses, and enterprise relationships in derivatives, trading infrastructure, and payment rails.

If you are in this quadrant, the cool-headed play is: manage valuation and cash runway like your life depends on it, aim for a meaningful M&A outcome, because it is real. Don't price yourself out of the acquirer pool. Don't burn 24 months of runway chasing one enterprise logo. Build complementary partnerships with larger players who might ultimately want to acquire you.

Traditional Finance-Oriented, With Traction

The winners of the current regime.

Tokenized real-world assets grew from $5.5 billion at the start of 2025 to $18.6 billion by year-end, a 3.4x growth in twelve months. The largest tokenization platforms now handle billions in institutional liquidity, with market leaders holding around 20% share, supporting one of the world's largest tokenized treasury funds with nearly $3 billion AUM.

These companies aren't trying to convince anyone crypto is the future. Their institutional clients have already decided. The game now is straightforward enterprise sales: win more banks, more asset managers, more issuers; build alliance structures where an institution buying one of your products naturally buys three more from your partners; compress unit economics on the compliance and custody stack you've already built.

If the team is a pure service provider, this becomes a classic enterprise software war: sales velocity, net retention, integration depth.

The primary risk for this quadrant is not from crypto-native competition. It's from existing behemoths, large asset managers and global banks, eventually building their own rails, bypassing the startups that helped them adapt to the chain. The window is real, but not infinite.

The four quadrants appear different on the surface but are all navigating the same underlying shift: the market is maturing.

This doesn't mean narrative is dead. Institutions also chase hot themes, as anyone who has watched semiconductor and AI valuations over the past two years knows. But in a mature market, the half-life of pure narrative is shorter. It can still get you started, but it cannot keep you going.