A new report from Tether shows USDT saw growth in several metrics during the last quarter of 2025, including a new record in transfer volume.

Tether’s USDT Set A New Transfer Volume Record In Q4 2025

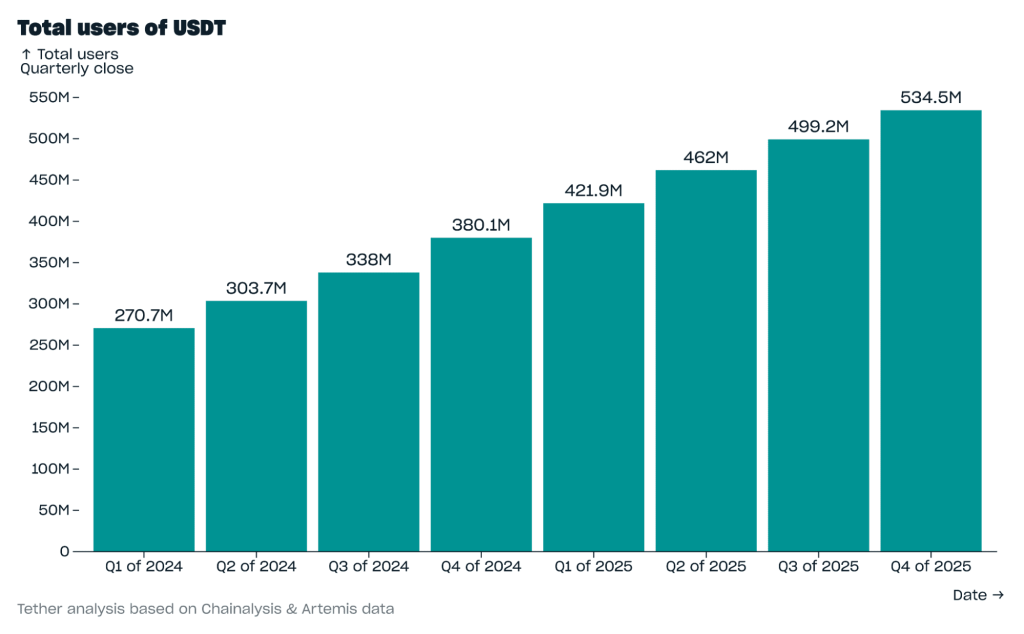

USDT issuer Tether has released its market report for Q4 2025 and it shows several new records for the largest stablecoin by market cap. First, the number of USDT users increased by 35.2 million during the period, taking the total to 534.5 million.

The quarterly growth in USDT users over the last couple of years | Source: Tether

In this count, Tether has included both the users who have received and used USDT for at least 24 hours on-chain, as well as the estimates of users that have received the stablecoin on centralized platforms like exchanges.

From the above chart, it’s visible that Q4 2025 was the eighth consecutive quarter in which Tether’s stablecoin saw growth of more than 30 million users. In terms of active users, the quarter set a new all-time high (ATH) with an average of 24.8 million users receiving USDT at least once inside a 30-day rolling window. “This accounts for 68.4% of all stablecoin monthly active users,” noted the report.

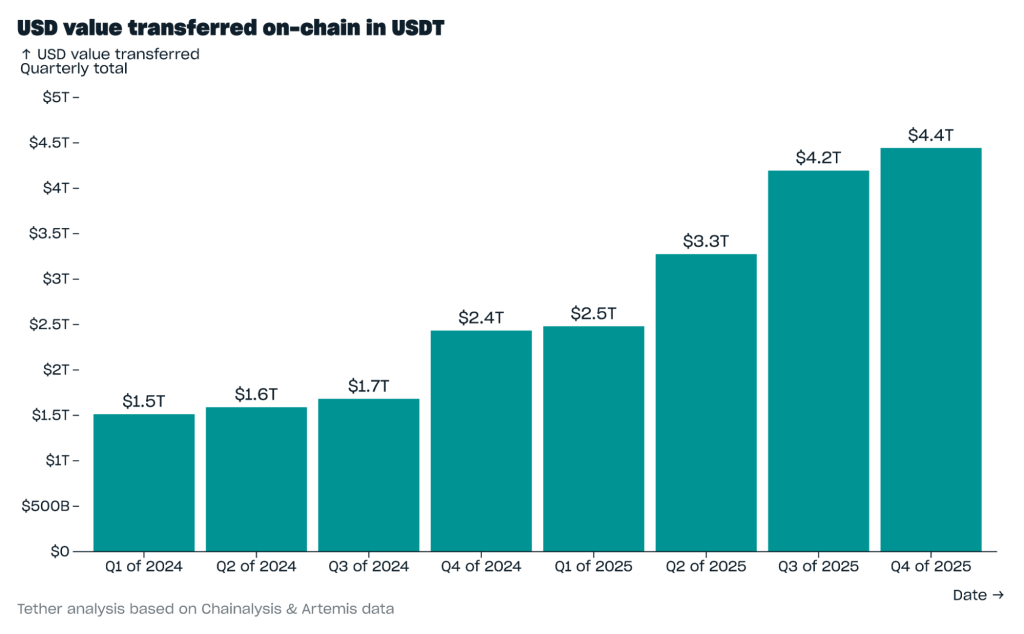

On-chain transfer volume also set a new ATH in this quarter, hitting a value of $4.4 trillion following a jump of $248.6 billion.

The stablecoin's transaction volume saw a notable rise over the past year | Source: Tether

As displayed in the chart, the USDT transfer volume stood at just $1.7 trillion in Q3 2024, so the sharp jump to $4.4 trillion since then indicates demand for using the stablecoin has seen a notable boost. “Of this $4.4T quarterly total, $2.8T (63.6%) was in transactions where USD₮ was the only asset transferred, and $1.6T (36.4%) was in transactions where multiple assets were transferred (typically in DeFi swaps),” said the report.

There has also been growth in transaction demand among the retail investors, as the number of transfers involving the stablecoin jumped by $313.1 million in Q4 to a new ATH of 2.2 billion. 88.2% of these transactions involved a sum less than $1,000.

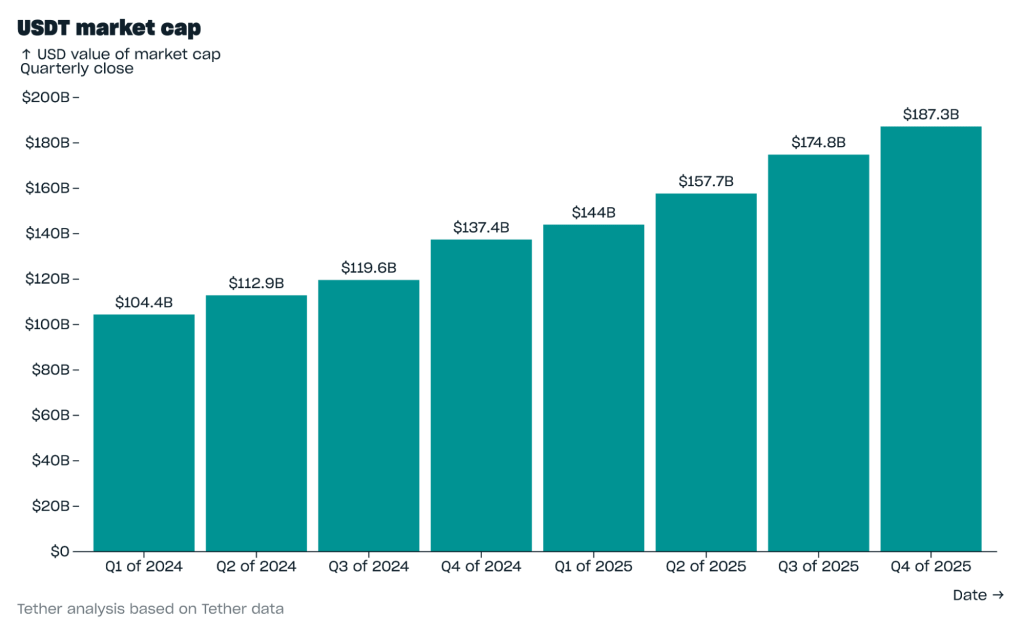

The capital invested in the stablecoin itself also saw an increase during the quarter, with the market cap hitting $187.3 billion after inflows of $12.4 billion.

Looks like the token's market cap has seen steady growth | Source: Tether

The growth in the USDT market cap occurred despite the fact that the wider cryptocurrency market saw a bearish transition in October. That said, the downturn still affected the token to some degree as before the market slowdown, its monthly market cap growth rate was sitting at 4.9%, which declined in the aftermath of the liquidation squeeze of October 10th.

Overall, between October 10th and today, USDT has been among the more resilient cryptocurrencies, being up 3.5% while the combined sector has lost more than a third of its market cap. In the same period, USDC, the second largest stablecoin, has seen a drop of 2.6%.

Bitcoin Price

At the time of writing, Bitcoin is trading around $65,800, down more than 9% over the last 24 hours.

The price of the coin seems to have been crashing | Source: BTCUSDT on TradingView