Original | Odaily Planet Daily (@OdailyChina)

Author | Asher (@Asher_0210)

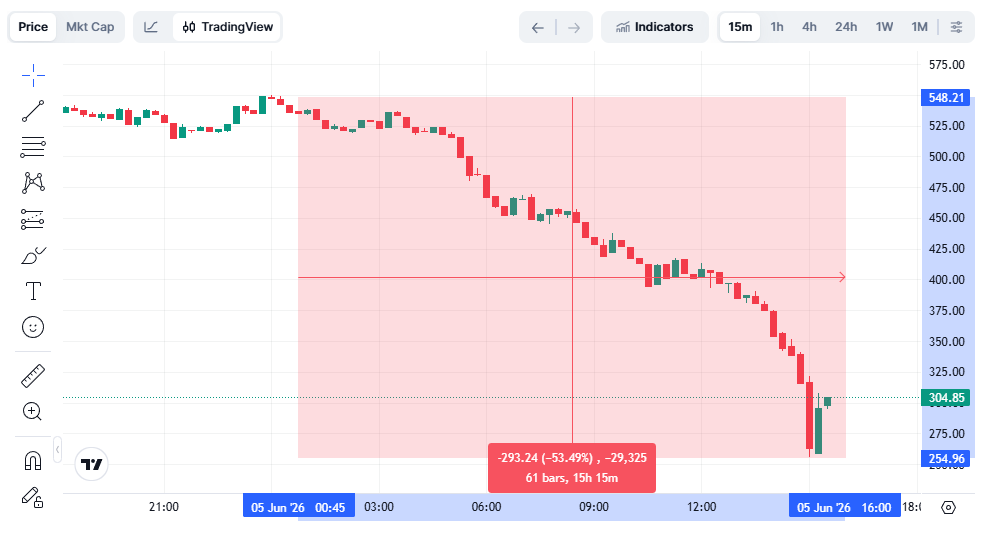

After the news broke, the Zcash token ZEC quickly nosedived, plummeting over 30% in a short time; by the afternoon, the sell-off didn't stop, panic continued to spread, and the price once fell to around $250, with the intraday loss widening to over 50%.

Security researcher Taylor Hornby discovered the issue on May 29th and has completed vulnerability verification in a local environment, generating test counterfeit ZEC, further validating that the vulnerability is an executable attack path. Currently, the two biggest controversies surrounding Zcash are: First, whether counterfeit ZEC has ever appeared in the privacy pool over the past four years; Second, how can officials prove that no counterfeit ZEC has flowed into the privacy pool, an extremely difficult task to disprove.

Where Did the "Unlimited Minting" ZEC Come From?

The security of Orchard (Zcash's privacy-protecting "shielded pool") relies on zero-knowledge proof circuits, with the core rule being asset conservation: the spend of each transaction must come from legitimate inputs, and ZEC cannot be created out of thin air. Users can hide balances and transaction amounts, but the system must verify the transaction's legitimacy.

Security researcher Taylor Hornby discovered that a constraint in the Orchard circuit was incomplete (under-constrained), allowing attackers to input data that should not have passed, yet verification could still return as successful. In other words, without needing administrator privileges or controlling nodes, and not being a backdoor, as long as the system mistakenly deems a transaction legitimate, originally non-existent ZEC could be recorded as legitimate assets within Orchard.

Shielded Labs called it "unlimited, undetectable counterfeit ZEC".

The Bug is Fixed, but Historical Issues Remain Unresolved

For ordinary security incidents, the biggest fear is large losses, but the most troublesome aspect of Zcash's current crisis is that the losses cannot be directly quantified.

If an attack occurred on the transparent chain, the market could at least see the attack address, fund flows, and affected assets. However, Orchard's transaction amounts, balances, and fund paths are inherently hidden. Once counterfeit ZEC might have appeared in the pool, it's difficult for outsiders to judge whether it's still lingering in Orchard or has gradually flowed out through normal transactions.

More critically, Orchard is not a completely isolated black box. Users can migrate assets between different fund pools, and both real ZEC and potential counterfeit ZEC could mix within the pool.

The Zcash ecosystem can emphasize that there is currently no evidence of the vulnerability being exploited and can explain that the probability of malicious exploitation is low. But for traders, "no anomalies have been found" and "it has been proven that nothing happened" are not the same thing.

This is the core reason for ZEC's expanding decline. Until the question of whether counterfeit ZEC ever appeared in Orchard is proven, ZEC's supply credibility will remain under a shadow.

Arthur Hayes Liquidates Position, Igniting Market Confidence Crisis

After the ZEC vulnerability was exposed, BitMEX co-founder Arthur Hayes's public liquidation further amplified market panic.

Arthur Hayes stated on platform X that he has sold his entire ZEC holdings. Hayes said he learned about the attack yesterday but did not realize its conflict with his narrative framework. ZEC's 30% drop prompted him to reconsider and decide to take full profits on that position. He added that while he believes the possibility of additional minting is extremely low, he cannot formally prove its impossibility at the cryptographic level; he will continuously reassess his judgment and, if his assumption is disproven, will repurchase, hoping to build a position at a lower price; privacy is priceless, and he wouldn't mind repurchasing at a higher price.

This was quite damaging for ZEC. Over the past period, Arthur Hayes has been one of the key narrative drivers for ZEC. His bullish view was based on the long-term logic of privacy assets regaining pricing power in the context of AI, government surveillance, and big tech expansion. Therefore, his liquidation wasn't just a major holder taking profits; it resembled a public downgrade of ZEC's current narrative.

When a top narrative supporter chooses to exit first, long positions originally supported by belief and expectations are more likely to turn into collective profit-taking and risk aversion.

Community Sentiment Spiral, ZEC Transforms from Price Correction to Trust Crisis

Perhaps influenced by Arthur Hayes's liquidation, community discussions about ZEC quickly shifted from "whether to buy the dip" to "whether it can still be trusted."

On one hand, the community repeatedly emphasized the severity of the vulnerability itself. Compared to short-term price drops, many users were more concerned that a vulnerability theoretically capable of creating unlimited counterfeit coins had lurked in Orchard for nearly four years. For them, the price drop was just the surface; what truly shook confidence was the question mark placed on Zcash's core security assumptions.

On the other hand, the process of AI-assisted vulnerability discovery further exacerbated distrust. Taylor Hornby, with the aid of AI tools, conducted a targeted review of the Orchard circuit, ultimately discovered the vulnerability, wrote an exploit program, and generated counterfeit ZEC in a local environment. Although AI did not perform the audit independently, what the community more easily remembered was the narrative that "a key vulnerability existing for years was assisted in being found by AI in a short time," which quickly gained traction.

This turned public criticism towards Zcash's development and audit systems. The community questioned why a vulnerability existing since 2022 could go undetected on the mainnet for years? If even the core privacy pool could have constraint omissions, how can users trust Zcash's promises on supply and privacy security again?

Therefore, this decline is no longer just profit-taking. Before Zcash provides more convincing proof, no one is really willing to hold ZEC long-term.