Author: Prathik Desai

Compiled by: Saoirse, Foresight News

Trying to sell me a product? Skip the lengthy feature pitch, first prove whether you use it yourselves. Amazon built its business on AWS, yet all the products sold on its platform run on the same set of servers open to its competitors. If a company isn't willing to use its own product, how can it convince customers to buy it?

Securitize's core business is providing asset tokenization infrastructure, committed to helping public companies, private equity funds, and asset management institutions bring various securities onto the blockchain. To prove the value of on-chain stocks to the market, the best demonstration is undoubtedly to tokenize its own shares first, and that's exactly what Securitize did.

On July 2, 2026, Securitize Co-founder and CEO Carlos Domingo rang the bell at the New York Stock Exchange, completing the company's public listing. That very morning, on the day of the listing, the company's shares were simultaneously launched in token form on the Solana and Avalanche public blockchains. This was not a wrapped derivative model, but direct registration of equity ownership on the blockchain, detached from traditional centralized registries. On the first day of trading, approximately $270 million worth of common stock was registered on-chain.

A company choosing to tokenize its shares concurrently with its IPO inevitably invites heightened regulatory scrutiny; most newly public companies deliberately avoid such risks, but Securitize actively chose to face the regulatory scrutiny head-on.

This leads to a thought-provoking question: If a public company can issue tokenized shares simultaneously with its listing, why can't private startups replicate this model at the Series A funding stage?

This article explores how tokenized equity will fundamentally reshape the entire suite of services that venture capital (VC) firms deliver to startups via a bundled Term Sheet.

What's in a Term Sheet?

Founders seeking venture capital (VC) funding want much more than just capital. Every time a VC signs a Term Sheet, it is essentially promising a bundled package of services.

- First, capital. The VC commits funds to fuel the company's growth from zero to one.

- Second, valuation pricing. All private companies need a valuation, and in the private market, this task is typically led by the lead investor.

- Third, curation/validation. Having a well-known firm on the cap table signals to the market that the venture is investment-worthy, helping attract follow-on investors, commercial clients, and top talent.

VCs also leverage their industry networks to connect companies with corporate clients, experienced technical talent, and key industry resources. In some cases, there's an implicit promise of follow-on investment: continuing to invest additional capital as the company grows. Finally, and crucially: the Term Sheet includes governance terms. As consideration for the investment deal, the VC typically gains a board seat, information rights, protective provisions, and the power to set transfer restrictions.

This entire bundle is the complete service package that a VC sells to a startup in a funding round.

This bundled model has remained stable for so long because private equity has long been closed to ordinary investors. Individual investors wanting to trade private shares or participate in price discovery were highly dependent on company cooperation.

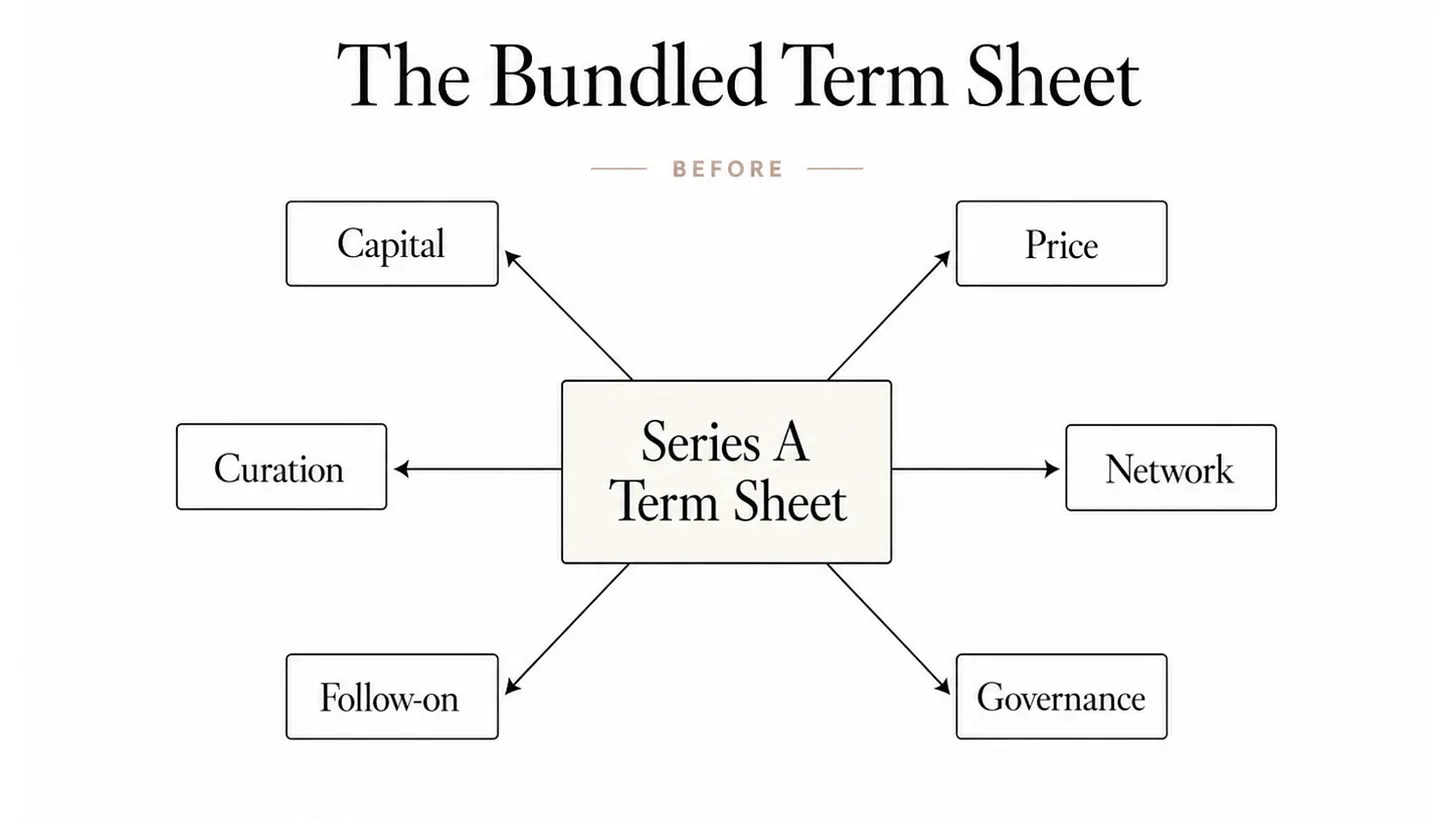

This diagram illustrates how a traditional Series A Term Sheet is a bundled model: one Term Sheet packages capital, pricing, validation, network access, follow-on commitment, and governance all together at once; founders cannot pick and choose separately.

Last month, I described how blockchain infrastructure can unbundle the functions of banks in IPO underwriting. Now, the same technology enabling stock tokenization further reveals that VCs no longer monopolize the pricing power for private companies.

However, a key constraint exists.

When Securitize tokenized its stock, it was a decade-old mature company with audited financials, discloseable cash flows, over $4 billion in tokenized assets on its platform—the market had sufficient information to perform a valuation. In contrast, a Series A startup is judged largely based on the founder's resume, personal reputation, and business vision. While the underlying asset (equity) is the same for both, the core basis for valuation is entirely different.

This highlights the core significance of validation in the Term Sheet. For a Series A venture, the VC's value isn't just having its name on the cap table; it's providing credibility for a company lacking public operational data. Late-stage pre-IPO companies like SpaceX and OpenAI find it easier to tokenize their equity because their operational profile is closer to a public company; secondary markets, tender offers, perpetual contracts, and brokerage research reports already provide price references long before the official listing.

Although implementing tokenization for early-stage company equity is more challenging due to the lack of data for fair pricing, this does not prevent the unbundling of the VC's bundled service package.

The Wave of Unbundling Arrives

Securitize is not the first company in the US to put its listed stock on a blockchain. Exodus did it on Algorand in 2021, and digital asset and data center company Galaxy Digital also issued on-chain equity. But Securitize achieved an industry breakthrough by being the first to issue native on-chain equity on the very day of its IPO.

The tokens traded on Solana and Avalanche have the exact same legal standing as the shares traded on the NYSE. Each token carries equivalent voting rights, dividend rights, and residual claim rights. They are not synthetic derivatives merely tracking price, nor are they beneficial interest certificates via an offshore Special Purpose Vehicle (SPV) holding shares. Securitize's tokenized common stock carries rights identical to its off-chain native SECZ shares.

Investors often confuse the ownership nature of various on-chain "stock tokens." Vaidik's article "Who Really Holds Your US Stocks? This Institution Nominally Holds 83% of the Market's Shares" sorts them into two main types: one is natively issued by the issuer (e.g., SECZ, Exodus), where the token itself represents the equity; the other is a custodial wrapper model, e.g., xStocks, Robinhood stock tokens, where an SPV holds the real shares, and investors only have a claim to proceeds. Only the first type of token carries full shareholder rights, and this is precisely the foundation upon which the entire VC business model rests.

Once equity can be continuously priced and freely transferred, the various services originally bundled in the Term Sheet no longer need to be sold as a package; each need can find a lower-cost, higher-efficiency independent solution.

For mature companies with a valuation basis, fundraising and valuation pricing can be gradually handed over to the market layer: prices are discovered by the market, and capital follows the price. Currently, the total value locked in tokenized equity on Ondo Global Markets has exceeded $1 billion; on the Hyperliquid platform, the pre-listing perpetual contract price for Cerebras deviated by only 1.3% from its Nasdaq opening price.

Project validation and network access still require an anchor investor, but the lead capital and brand credibility no longer must rely on the complete system of large firms like Sequoia or a16z. Elad Gil set up a roughly $1.5 billion solo fund, providing lead investment and brand validation with just himself and a rolling fund structure.

Specialized service providers address various ancillary needs: Fairmint and Pulley handle cap table management; Coinbase acquired LiquiFi in July 2025 to enter the token vesting space; Echo, acquired in October 2025, focuses on fundraising tools; Magna and Sablier handle streaming vesting. Founders in 2026 can assemble a full toolkit themselves, achieving backend capabilities they previously had to purchase as a bundle from VCs.

Governance becomes programmable. Fairmint's architecture supports continuous fundraising modes similar to SAFEs, automatically executing equity conversions according to preset rules; vesting schedules and unlock rules are enforced by smart contracts, no longer solely reliant on lawyers drafting documents.

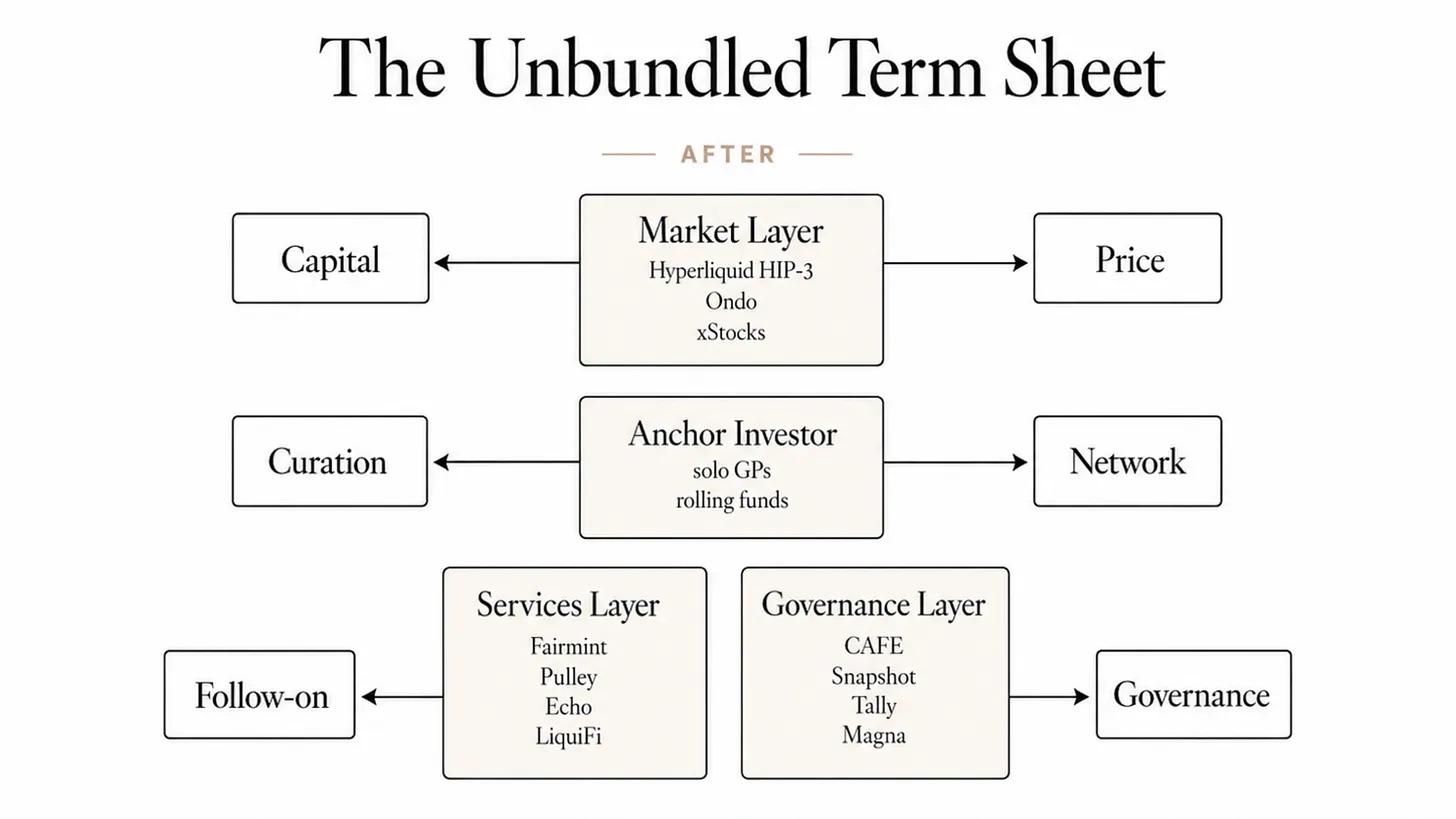

In the age of tokenized equity, the Term Sheet undergoes service unbundling: the six functions originally handled by a single Series A Term Sheet are split, with capital & valuation handed to the market layer, validation & network provided by anchor investors, and cap table administration & governance handled by specialized tech service providers; founders can purchase each service separately as needed.

Secondary liquidity channels continue to expand, giving company employees and early investors more exit options. Employees and angel investors in tokenized private companies no longer need to wait years for an IPO to sell part of their holdings.

Continuous liquidity is the profound change brought by tokenized equity trading. Liquidity fundamentally reshapes how founders and employees view equity. When shares can be traded at any time, the incentives and negotiations around vesting schedules and exit windows change. Previously, employees often had to wait four years for a tender offer opportunity; now they can connect with secondary markets anytime. But the new model also presents trade-offs.

Similar cases have already appeared in the crypto industry: Layer 2 governance tokens like Arbitrum's ARB and Optimism's OP were tradable immediately upon launch. When team tokens vested en masse, selling pressure occurred, causing token prices to decouple from actual network performance, forcing founders to spend excessive time monitoring markets, diverting focus from product development.

Of course, this analogy has limits: ARB and OP are governance tokens, not company equity; their prices reflect more on ecosystem activity than corporate profits. Yet the incentive misalignment they expose is highly similar. Regulatory guardrails like Reg D 506(c) accredited investor access, Rule 144 lock-up requirements, and multi-year lock-up agreements can mitigate concentrated selling but cannot eliminate the issue at its root. Tokenized equity opens a new exit channel for insiders, breaking the traditional mechanism of smoothing out realization pressure over time in private markets.

The follow-on investment commitment, often most valued by founders, remains the last piece in the VC service bundle for which there is no mature tokenized alternative.

The reason is that all current regulatory frameworks for implementation — including the SEC-approved DTCC pilot, Nasdaq's token trading system, and DTCC's related service launching in October — are all targeted at already-public companies like Russell 1000 constituents. Currently, there is no compliant channel supporting the public trading of tokenized equity from a Series A startup on these platforms.

Which Core Value Remains with VCs?

When the streaming era arrived, music distribution was completely commoditized, but record labels didn't disappear. Anyone can upload a song to Spotify; what couldn't be commoditized was the A&R (Artists and Repertoire) business: selecting creators worth investing in, building artist brands, and accessing industry resources not reachable by data alone. Record labels that adapted evolved into institutions making value judgments based on data. Their once-integrated business was unbundled to various service providers, leaving the labels with the scarce task of value discernment.

The venture capital industry will likely follow a similar evolutionary path. Tokenized equity will gradually take over all procedural tasks in the Term Sheet: ownership registration, price discovery, share transfer, scheduled vesting unlocks. Blockchains handle standardized processes far more efficiently than paper Term Sheets.

What will always remain scarce is the investor whose mere reputation can secure the next funding round, convince a large client to switch suppliers, or persuade senior talent to leave a big tech firm for a startup. Token technology cannot provide commercial validation for founders.

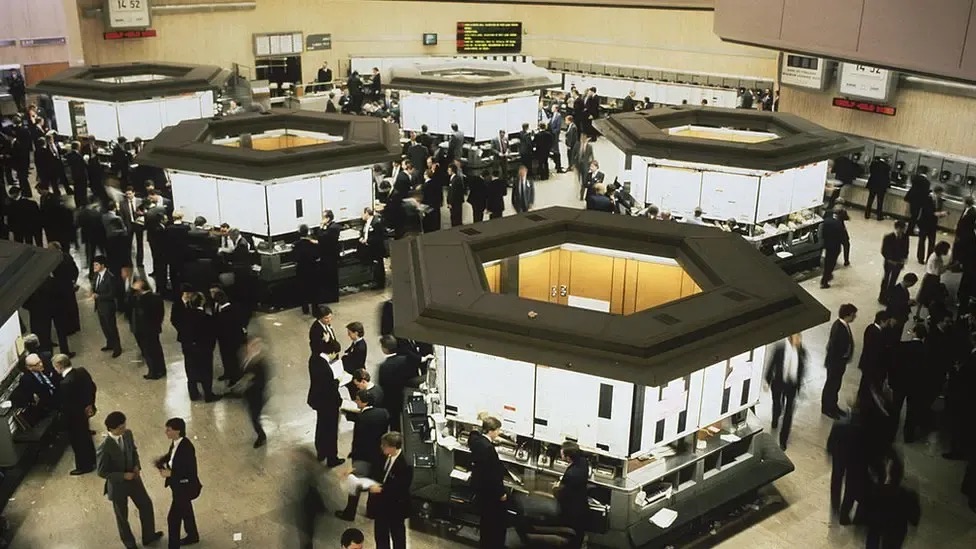

But any wave of service unbundling is eventually followed by a new round of integration, often led by new entrants. The 1986 London Big Bang unbundled broker and market maker roles, yet within a decade, universal banks had reintegrated various specialized functions.

After the London "Big Bang" reforms introduced electronic trading, the trading floor of the London Stock Exchange became obsolete. Source: Getty Images, BBC

For decades, founders proactively approached VCs because only there could they get capital, valuation, validation, and governance support all in one place. Tokenized equity is like a corridor with many separate doors: one for capital, one for pricing, one for governance needs. Founders still need all the services, but no longer must purchase them all from the same institution.

This also changes the underlying early-stage decision-making logic for entrepreneurs. Founders are no longer forced to agonize over "which fund to bring onto the cap table to solve all development problems at once." Instead, they gain the autonomy to choose: which functions to let market mechanisms handle, and which aspects to trust to human judgment.

The standardized processes in Term Sheets will be the first to be tokenized, as these are easiest for the market to take over. The value judgment component will be the last to be digitized, and perhaps may never be digitized; the market will always need humans to provide this service. A future Series A startup might be able to put its equity on-chain, but it will still need someone to make the judgment: is this equity worth bringing to the market?