By: Caitlin Ostroff, Katherine Long, and Neil Mehta, WSJ

Translated by: AididiaoJP, Foresight News

John Pedersen, 33, currently cannot work. The former Outback Steakhouse chef is recovering from a car accident and his savings are running low. The prediction market platform Kalshi seemed like a quick fix. He took out a variable-rate loan and started placing bets.

It started well. By betting on the daily snowfall in Detroit, where he lives, Pedersen turned about $2,000 into nearly $8,000, according to a Wall Street Journal review of his account records. He then put the money into sports trading, using AI-assisted strategies, and eventually reached $41,000.

Then he made his boldest bet yet: staking the entire $41,000 on a specific word being said by a celebrity on TV. He lost it all.

Pedersen isn't the only one who has left empty-handed from the 'bet-on-anything' markets, which cover sports, celebrities, news, and more.

Kalshi and its competitor Polymarket market themselves as tools that can change ordinary people's fortunes—implying everyone has a fair shot at a big win. "I almost couldn't pay my rent, but thanks to Kalshi's predictions, I made two years' worth of rent," a woman excitedly says in a Kalshi ad on TikTok.

But for most users, the reality is quite the opposite.

Instead, according to a Wall Street Journal analysis of platform data and interviews with traders, the average trader is losing money consistently, while a small group of experienced professionals—including trading firms with massive data resources—are eating up their funds.

The Journal found that on Polymarket, 67% of the profits go to just 0.1% of accounts. This means fewer than 2,000 accounts have netted nearly $500 million collectively. The Journal analyzed 1.6 million accounts trading on Polymarket since November 2022. The platform has at least 2.3 million total accounts.

Kalshi shows a similar pattern, with far more losers than winners. Spokesperson Elizabeth Diana said that based on the past month's data, for every profitable user, there are 2.9 losing users. She said this ratio could change as the platform grows. The company does not publish comprehensive user profit data nor disclose total user numbers.

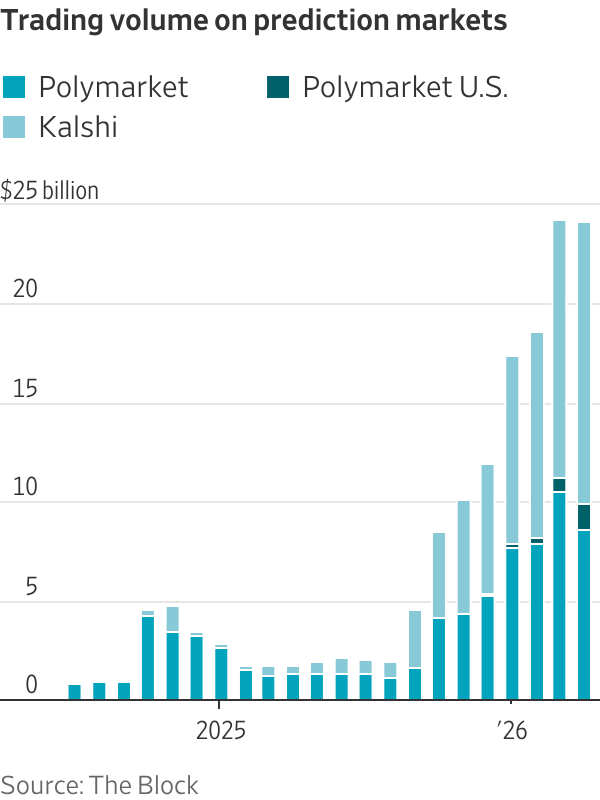

According to data analytics firm The Block, the two platforms' combined trading volume soared to $24.2 billion in April, up from $1.8 billion a year earlier.

Supporters say these markets are not gambling but harness the wisdom of crowds to accurately predict future events. Federal Reserve research has shown Kalshi to be an effective tool for predicting economic trends.

Traders are paying for big data feeds from third parties to gain an edge. Computers use data and algorithms to predict price movements and manage risk faster than any human could. Professionals also leverage scale to trade frequently and strategically—sometimes tens of thousands of times a day—profiting from tiny price movements, requiring a level of focus and discipline rare among casual users.

"The retail trader has no chance," says Michael Bos, a former professional poker player with a background in statistics. He places about 60 trades a minute on Kalshi and updates his buy and sell quotes 30 times a second.

Diana said a similar concentration of wealth is seen in many financial markets, and more users make money on Kalshi than in day trading or traditional sports betting. She said Kalshi has stopped running the "help me pay my rent" ads.

A Polymarket spokesperson declined to comment on the Journal's analysis.

Polymarket has a data partnership with Dow Jones, publisher of the Journal. This analysis used only publicly available data.

Take the case of Pedersen, the unemployed chef who lost everything. He fell into a category full of "marks": mention markets (bets on whether someone will say a specific word).

Professional traders say they avoid such bets because they are unpredictable; not even millions of dollars in data provides a reliable edge.

According to the Journal's analysis, mention market bets pay out far less often than their listed odds suggest. Retail bettors take on more risk than they realize, partly due to the "longshot bias" phenomenon—where bettors, excited by the prospect, overestimate the likelihood of improbable events.

Kalshi's mention markets have far higher monthly trading volume than Polymarket's and have exploded since mid-2025. These bets are popular with the young users the platforms court—including influencers who promote them in social media livestreams and other videos showing off wins.

John Pedersen outside a homeless shelter in Detroit, where he has been living since losing money on Kalshi investments. © Emily Rose Bennett for The Wall Street Journal

"Smarter Than You"

For all types of bets, the pitch from Polymarket and Kalshi is simple—users can monetize what they know and make money fast—a message that has gone global.

Yet the Journal's analysis found that over 70% of Polymarket users are losing money. A working paper last month by French and Canadian researchers reached a similar conclusion. They found profits in prediction markets flow almost entirely to sophisticated traders, while one-off and retail traders bear the losses.

The Journal's analysis of Polymarket trading data shows the average user loses between $1 and $100, while the worst-performing 10% of users lose an average of $4,000 each.

Some make emotional decisions—following gut feelings or betting based on information gleaned from public channels.

A self-described problem gambler from Connecticut lost $2,000 on Kalshi betting on the Super Bowl in a single day—all in the tense fourth quarter. A 31-year-old from Indiana called the trading "like crack," betting on sports on Kalshi nearly daily in the first months of this year and losing about $5,000.

In contrast, prediction markets are increasingly attracting companies with dozens of employees, spending millions on professional sports and financial data, and running trading algorithms. Their aim is to outperform the students, recreational gamblers, and other low-volume traders who make up the bulk of the platforms' users.

In traditional gambling, the house sets the odds, takes the bets, and pays the winners. In prediction markets, there is no "house"; users trade with each other. Platforms only collect trading fees, which vary based on contract price, market type, and other factors.

In a SoHo office, a college dropout stares at a computer screen watching millions of dollars flow from retail traders betting on the price of Bitcoin.

Samuel Wood-Soloff dropped out of Princeton this year after receiving a $500,000 check from Alliance Capital, a crypto startup accelerator backed by prominent Silicon Valley investors, including crypto entrepreneur Balaji Srinivasan. He took math classes at UC Berkeley in high school and took a gap year to trade cryptocurrencies before attending Princeton. Now, he and four friends have moved to New York to trade prediction markets full-time, betting on sports, politics, and future crypto prices.

"Our only competition is other market makers," he said in an interview, referring to other firms like his that continuously provide buy and sell quotes. He declined to disclose his firm's profits or losses but said he has deployed $500,000 to $1 million across Polymarket, Kalshi, and other smaller prediction markets.

Former poker pro Bos has made over $668,000 on Kalshi, mostly from sports bets, since he started trading seriously about three months ago. Beyond his trading speed, he is meticulous about pricing his buy and sell quotes.

"You'll find the easiest money is in sports," he says. "Sports attracts all the 'degenerate' young men, I guess." He clarified "degenerate" referred to gambling addicts.

He observes on Kalshi that a lot of retail traders simply bet "Yes" on what they hope will happen. "It's completely different from a crypto or stock exchange where people trade securities."

Jonathan Stall-Ryan, a University of Virginia student, runs a firm that is a top-five trader in crypto price markets on Kalshi. © Laura Thompson for WSJ

Stall-Ryan's firm pays for real-time data from third parties and uses algorithms to execute tens of thousands of trades daily. © Laura Thompson for WSJ

The founder of another firm with about a dozen employees—all college students like him—Jonathan Stall-Ryan, is a top-five trader by volume in crypto price bets on Kalshi. The firm spends more than $200,000 a year on real-time data feeds, AI coding agents, and servers, using algorithms to execute tens of thousands of live trades daily.

Stall-Ryan was at the University of Virginia with a fraternity brother when he saw him casually betting on Bitcoin prices on Kalshi. He said he thought to himself, "That guy is going to lose money."

Most of these professional traders act as market makers. Kalshi and Polymarket say they rebate part of the fees for market makers and sometimes even pay them to provide liquidity.

Quantitative trading firm Susquehanna International Group became Kalshi's first major institutional market maker in 2024. According to professional traders monitoring Kalshi's order book, the firm trades hundreds of millions of dollars weekly through Kalshi. Its accounts are private, so specific profits are unknown. Susquehanna declined to comment.

Another quant firm, Jump Trading, is active on both Polymarket and Kalshi. In mid-April, Citadel Securities President Jim Esposito said at a Semafor event the firm was "watching closely" the development of prediction markets. Some traders who buy high-risk options contracts are now flocking to prediction markets.

"All sports betting, all poker, all options trading is essentially betting against somebody who's dumber than you," Susquehanna co-founder Jeff Yass said on a 2020 sports betting podcast. He described his role in supporting the development of prediction markets in the same podcast as a "mission from God."

On one hand, he thinks Americans should be able to legally bet on sports even if it's banned in some states; on the other: "I expect to make a lot of money."

Stall-Ryan on the University of Virginia campus. His firm employs about a dozen college students. © Laura Thompson for WSJ

Looking for Easy Money

The platforms design contracts that pose "yes/no" questions about future events. Contracts are typically designed to pay out $1 if correct and zero if wrong. The contract price reflects traders' assessment of the event's probability. For example, if a contract for an event trades at 41 cents, the prediction market believes there is a 41% chance it will happen. If you win, a contract bought for 41 cents pays $1; if you're wrong, you lose your stake.

Contract prices fluctuate until settlement based on market forces between buyers and sellers. Traders profit from tiny price movements, much like Wall Street traders.

Many naive prediction market participants are repeating the mistakes of speculators looking for easy money in financial markets. Decades of research show day traders rarely make money. In recent years, many retail traders, spurred by social media, have lost their shirts on highly volatile meme stocks.

The U.S. operations of Kalshi and Polymarket (which recently launched to a small group of early users) are regulated by the Commodity Futures Trading Commission (CFTC) and say trading on their platforms resembles other regulated financial markets. The vast majority of Polymarket's activity is on its offshore platform, which technically blocks U.S. users but is easily bypassed with a VPN.

Critics say these markets are prone to issues like insider trading. Recent examples include alleged insider trading on U.S. military action in Venezuela, a Google announcement, and congressional races.

CFTC Chairman Michael Selig has defended prediction markets and asserted the federal agency's jurisdiction over them. The agency has cracked down on alleged insider trading and hinted at more government enforcement.

Polymarket said it has worked with the Justice Department to combat insider trading. Kalshi prohibits insider trading on its platform and has penalized several traders for violations in recent months.

Former Kalshi employee Adi Rajaprabhakaran last year called retail traders "fish" (gambler slang for easy-to-lose novices) on Substack. In an interview, while still broadly believing this to be true, he also argued that the presence of uninformed traders in prediction markets strongly incentivizes more sophisticated traders to enter, leading to more accurate predictions.

"Everyone who is betting thinks they are the more informed party," he said. "In the long run, the person who is more right will make more money. No one is being forced to do this."

The $41,000 Bet

Before encountering mention markets, Pedersen's experience on Kalshi had been going well. "I follow finance broadly," he said. "I'm always looking for ways to sharpen my acumen, if you will."

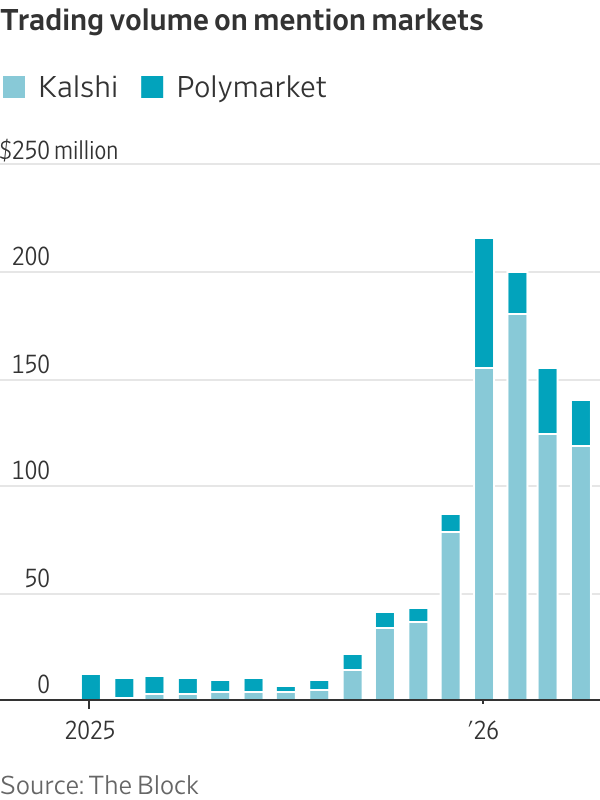

Trading volume in mention markets

The core question in a mention market bet is singular: Will a public figure say a certain word? This year, Kalshi users bet over $28 million on whether words like "cartel," "Somali," or "hockey" would be said during Trump's State of the Union address. According to The Block, Kalshi users bet nearly $181 million in mention markets in February alone.

The Journal's analysis of Kalshi data shows that mention markets pay out far less often than bettors might expect based on the listed odds.

Analyzing over 35,000 settled mention markets on Kalshi, the Journal found that on average, "Yes" trades priced with a 50% chance of winning actually paid out about 40% of the time. Since contract prices are supposed to match probabilities, these bettors are effectively overpaying.

The analysis found trading in these markets often exhibits a longshot bias, frequently losing money. On average, traders who bet "Yes" at the first price they see in a mention market—a common pattern for retail traders—would lose about 11% of their staked amount. That return is worse than most Las Vegas slot machines, according to research from the University of Nevada, Las Vegas.

Kalshi spokesperson Diana acknowledged a bias in expectations for mention markets but said they are not representative of the platform's overall pricing and are not the appropriate subject for such pricing analysis. She added that Kalshi's analysis shows mention markets are priced more accurately within four hours of an event.

Kalshi encourages mention market traders to livestream themselves trading during events, which two streamers said is to boost market engagement. Bank of America analysts wrote in an April report on prediction markets: "Mention market livestreams on social media often go viral and boost Kalshi's brand awareness."

In January, Pedersen staked his entire $41,000 windfall on rapper A$AP Rocky saying the word "rapper" on "The Tonight Show Starring Jimmy Fallon"—the star had recently played a rapper in a film. He had a chance to win over $168,000.

But the segment was cut from the NBC broadcast. Under Kalshi's market rules, only words said in the televised version count.

In a video he posted, Pedersen said this part of the rule was not obvious on the platform's website, and he didn't see it. (Kalshi later updated its interface to make market rules more prominent.)

Pedersen lost everything and had almost no other resources to fall back on. He now lives in a homeless shelter in downtown Detroit, though he says he recently received a job offer in mortgage sales.

He says once he gets back on his feet, his goal is to get into finance to support his music career. Would he return to prediction market trading? "Maybe," he said. "I'd rather spend my time on more regulated markets."