Original Author: Zhang Yaqi

Original Source: Wall Street Journal CN

Global stock markets have repeatedly hit new highs driven by the AI wave, but the fuel supporting this rally is becoming increasingly perilous—from the United States to South Korea, margin debt and leveraged ETF assets have both soared to historical extremes. The pro-cyclical nature of leverage itself is exponentially amplifying the tail risks of market volatility.

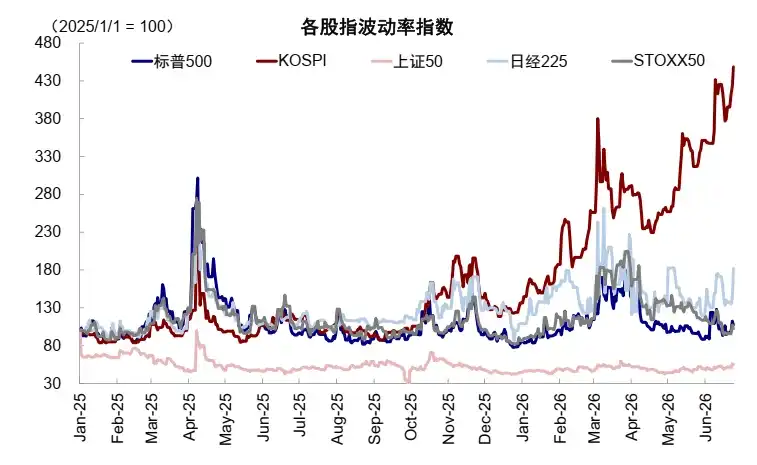

U.S. margin debt surged 54% year-on-year in May, reaching a record peak of $1.4 trillion; concurrently, the total asset size of leveraged ETFs nearly doubled in less than 70 days, exceeding $220 billion around June 3 (FactSet data). The risks of this leverage frenzy have first manifested in the South Korean market: the Korea Composite Stock Price Index (KOSPI) plunged 10% last week, triggering a trading halt, then rebounded sharply, only to trigger another halt shortly after, with violent fluctuations causing a co-movement weakness in U.S. AI-related stocks.

Alarms have since sounded on Wall Street. Barclays analyst Alexander Altmann warned clients this week that leveraged funds have accumulated purchases of approximately $300 billion in derivatives linked to individual stocks and indices since late March. If these positions need to be unwound in a short period, "the impact would be chilling," he described, characterizing it as "without doubt the largest source of non-fundamental risk in the market currently." Morgan Stanley also issued a warning on June 15, noting that marginal buyers in U.S. stocks rely on leveraged financing to an unprecedented degree, and such financing is becoming more expensive and scarce. Charles Schwab, one of the largest U.S. brokerages, tightened margin requirements this month and issued margin calls to clients exceeding the new thresholds.

All this points to the same logic: when a leverage-driven rally reaches its limit, the deleveraging backlash will magnify the decline by the same multiple.

U.S. Stock Leverage: Scale and Intensity at Historic Highs

The enthusiasm of U.S. investors for borrowing to buy stocks has currently reached unprecedented heights.

Financial Industry Regulatory Authority (Finra) data shows that U.S. margin debt in May increased 54% year-on-year, hitting a historical peak of $1.4 trillion. This surge runs parallel to the explosive expansion of the leveraged ETF market—products that typically track two or three times the daily percentage change of an underlying asset. According to FactSet data, between March 30 and June 3, the total assets of leveraged ETFs surged from about $115 billion to $220 billion.

The most sought-after products are concentrated in technology and semiconductor stock indices, as well as single-stock leveraged funds for Tesla, Nvidia, and more recently, SpaceX. Direxion's triple-leveraged ETF tracking a semiconductor index gained roughly 700% between late March and late June—yet on June 5 alone, it plummeted 31%, magnifying the benchmark index's decline by three times.

Investors ranging from hedge funds to retail traders on Robinhood have flocked in. Mark Hackett, chief market strategist at Nationwide Investment Management Group, expressed concern:

"I worry we are building a kind of hidden leverage that's not well understood. There are people with lottery-ticket mentality borrowing money to buy options on leveraged ETFs—that's already three or four layers of leverage."

Derivatives Mechanism: A Pro-Cyclical Amplifier

The danger of leveraged ETFs lies not only in their inherent profit-and-loss amplification mechanism but also in their potential to distort the price movements of the underlying assets they track—a phenomenon market participants call the "tail wagging the dog" effect.

Barclays estimates that to absorb the continuous influx of new capital, leveraged funds have accumulated purchases of about $300 billion in derivative contracts linked to individual stocks and indices since late March. After market makers take on these contracts, they need to hedge their own exposure by buying the corresponding spot stocks, further fueling the gains in tech and semiconductor stocks this year.

The problem is that this mechanism works in reverse as well and is self-reinforcing. Once the underlying stocks decline, leveraged fund assets shrink, forcing position reductions, which in turn depresses stock prices, triggering more redemptions and reductions, forming a negative spiral.

Dave Nadig, research director at ETF.com, issued a warning:

"Any market where there is a known, price-insensitive buyer or seller creates problems. I'm really worried that more and more money is flowing into this system of leveraged single-stock products, because the more money that goes in, the stronger this pro-cyclical trading effect becomes."

Warning from South Korea: Extreme Concentration Coupled with High Leverage

The scene that unfolded in the South Korean market this week is seen by market participants as a stress test case for reference.

According to a CICC research report, the KOSPI index has surged 87% year-to-date, leading global gains, primarily driven by memory chip giants like Samsung Electronics and SK Hynix. However, the combination of highly concentrated holdings and extreme leverage has sharply increased market fragility: on Tuesday, due to market concerns about memory chip expansion plans and the impact of news that South Korea was discussing taxing unrealized gains, KOSPI plunged 10% in a single day, triggering a trading halt; it then rebounded strongly over the next two trading days, returning above 9,000 points, only to trigger another halt on Friday.

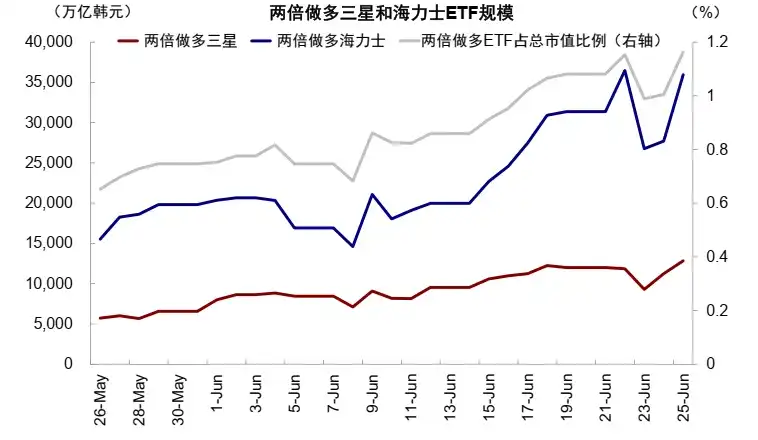

CICC estimates that current on-exchange leverage multiples in the South Korean market range from 2x to 5x, with broad leverage scale reaching 271 trillion won, an absolute level that has touched a historical high—theoretically, a decline of 16% to 36% in the underlying assets could trigger margin calls. According to The Wall Street Journal, trading related to leveraged funds tracking Samsung and SK Hynix recently accounted for up to 50% of the average daily trading volume of these two stocks, significantly disturbing their prices in both directions.

Lee Chan-jin, head of South Korea's Financial Supervisory Service, said at a press conference last week that he regretted not preventing the launch of leveraged single-stock funds: "These are high-risk products, and about 92% of holders are retail investors. Despite consumer warnings, trading fervor has not cooled."

Soaring Financing Costs: Borrowing to Buy Stocks Is Getting More Expensive

As previously reported by Wall Street Journal CN, Morgan Stanley's analysis reveals pressure accumulation from another angle.

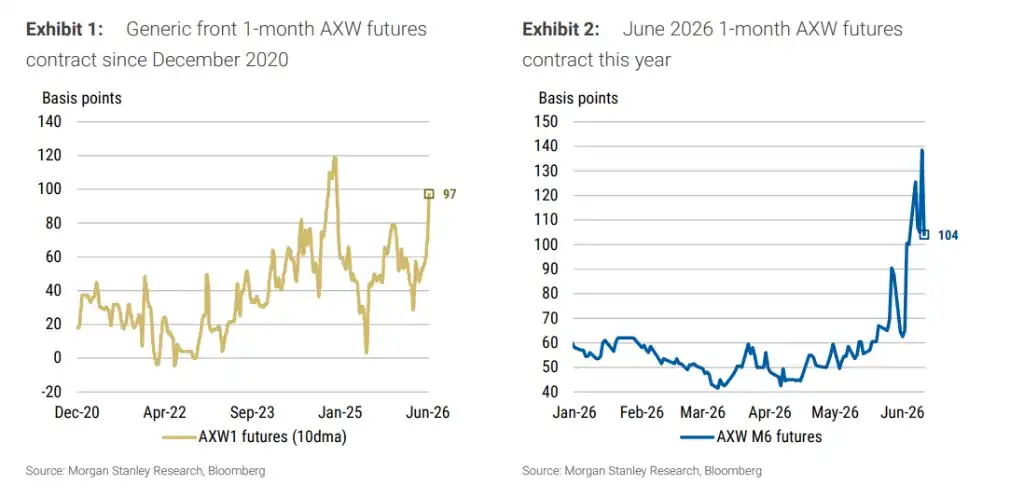

The core indicator measuring stock financing costs—the AXW futures (tracking the spread between the implied financing rate of S&P 500 total return futures and the benchmark rate SOFR)—for a one-month contract expiring in June spiked to +140 basis points last week. Even after the S&P 500 retreated from its historical high, the indicator remained at extremely high levels, marking the highest reading since December 2020 (excluding special year-end periods).

Meanwhile, data from the Federal Reserve Bank of New York shows that for the week ending June 3, 2026, the equity asset exposure held by U.S. primary dealers through securities financing methods like repo reached $223 billion, a record high. Morgan Stanley's constructed "equity financing reliance" indicator—dividing primary dealer stock repo scale by the S&P 500's free-float market capitalization—has soared nearly 50% over the past year, approaching the historical peak seen in mid-March this year. This means that for every dollar of market capitalization, an increasingly dense amount of borrowed funds has accumulated behind it.

This financing demand is highly concentrated in a few sectors. Morgan Stanley's sector breadth data shows that over the past three months, only the Information Technology sector among the 11 GICS sectors outperformed the S&P 500, gaining 24.2% with a 13.3% excess return; over the past year, on about 70% of trading days, the number of sectors outperforming the broader market did not exceed five. This indicates that the overall market's rise is actually supported by leveraged funds in a very few sectors. Once these funds begin to retreat, the impact on the overall market will be simultaneously amplified.

Once Deleveraging Begins, the Shock Will Be Multiplied

Morgan Stanley warns that the current situation constitutes a potential nonlinear risk: High financing costs force leveraged buyers to stop adding positions; the disappearance of marginal buyers causes the market to lose upward momentum; subsequent price corrections then trigger deleveraging, with selling pressure further amplified by leverage, ultimately leading to declines exceeding expectations. Historical data shows that阶段性 highs in AXW futures often coincide高度吻合 with阶段性 tops in the S&P 500.

More alarmingly, Morgan Stanley's financial conditions index shows that from the outbreak of the Iran conflict to June 11, financial conditions have tightened by an amount equivalent to a 31-basis-point rate hike, primarily driven by rising 10-year Treasury yields and a stronger dollar. However, because stock indices are still rising, most investors remain unaware of this tightening—the stock market rally itself contributed about -21 basis points of easing to financial conditions, masking to some extent the pressure from other factors.

Morgan Stanley's baseline forecast is that the Fed will cut rates by 25 basis points each in March and June 2027, with the final policy rate target range between 3.00% and 3.25%. However, the bank warns that once deleveraging triggers a stock market decline, investors will be forced to reassess financial conditions and subsequently reprice the Fed's policy path. The previously assigned weighting to tail risks of rate hikes will be the first to unravel.

Alexander Altmann wrote in a client note: "The technical forces that previously amplified upward momentum through leverage expansion may now begin to cut in the opposite direction."