Author: Nicky, Foresight News

Original Title: The Most Rapidly Expanding Stablecoin Recently Is Actually a Trump Family Pawn

In the current relatively stable stablecoin market landscape, WLFI's USD1 stablecoin is attempting to break through by leveraging Trump family resources and aggressive ecosystem strategies.

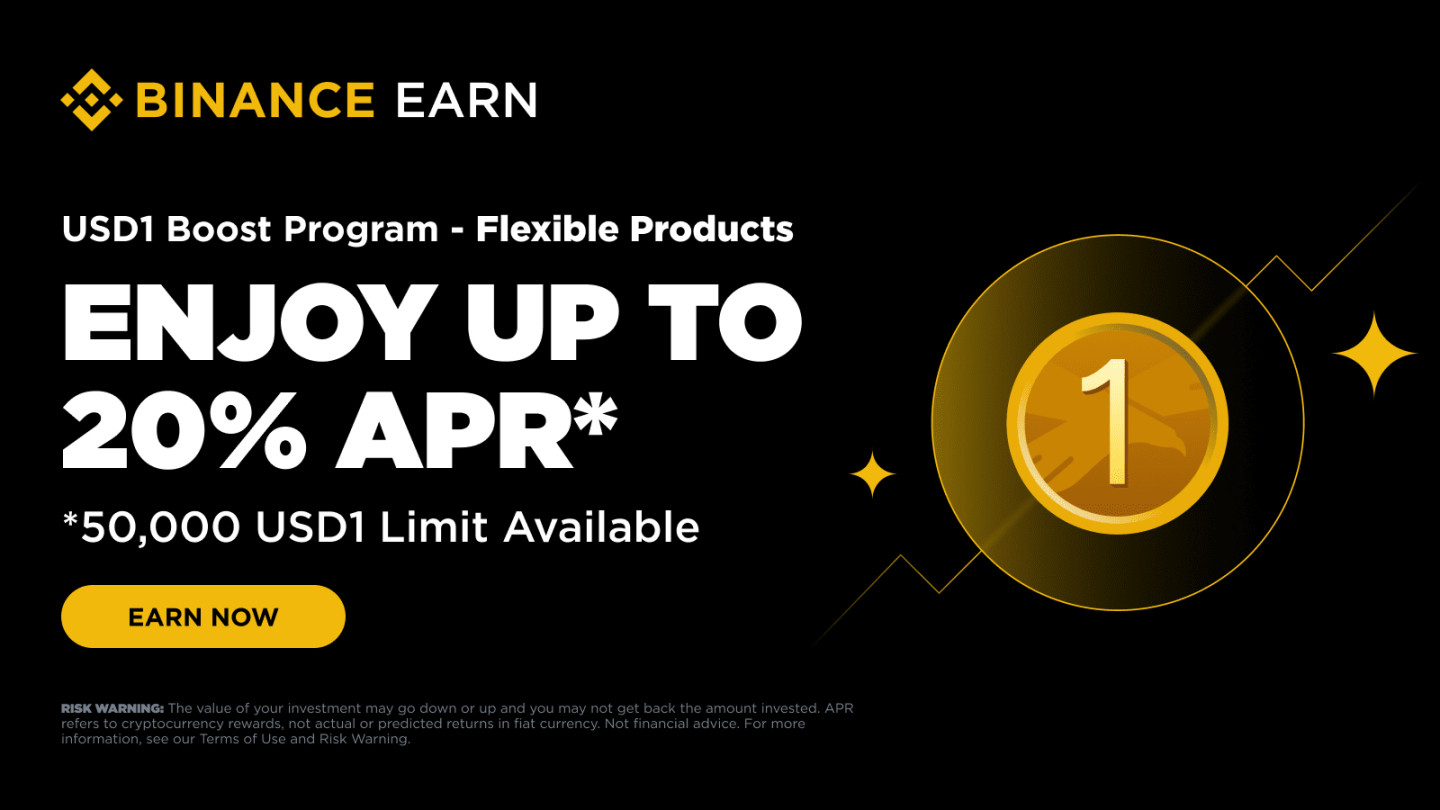

Recently, WLFI used treasury funds to incentivize adoption and partnered with Binance to launch a high-yield savings product with an annualized return of 20%, driving USD1's circulation to exceed 3 billion, with a single-day peak growth of over 7.6%.

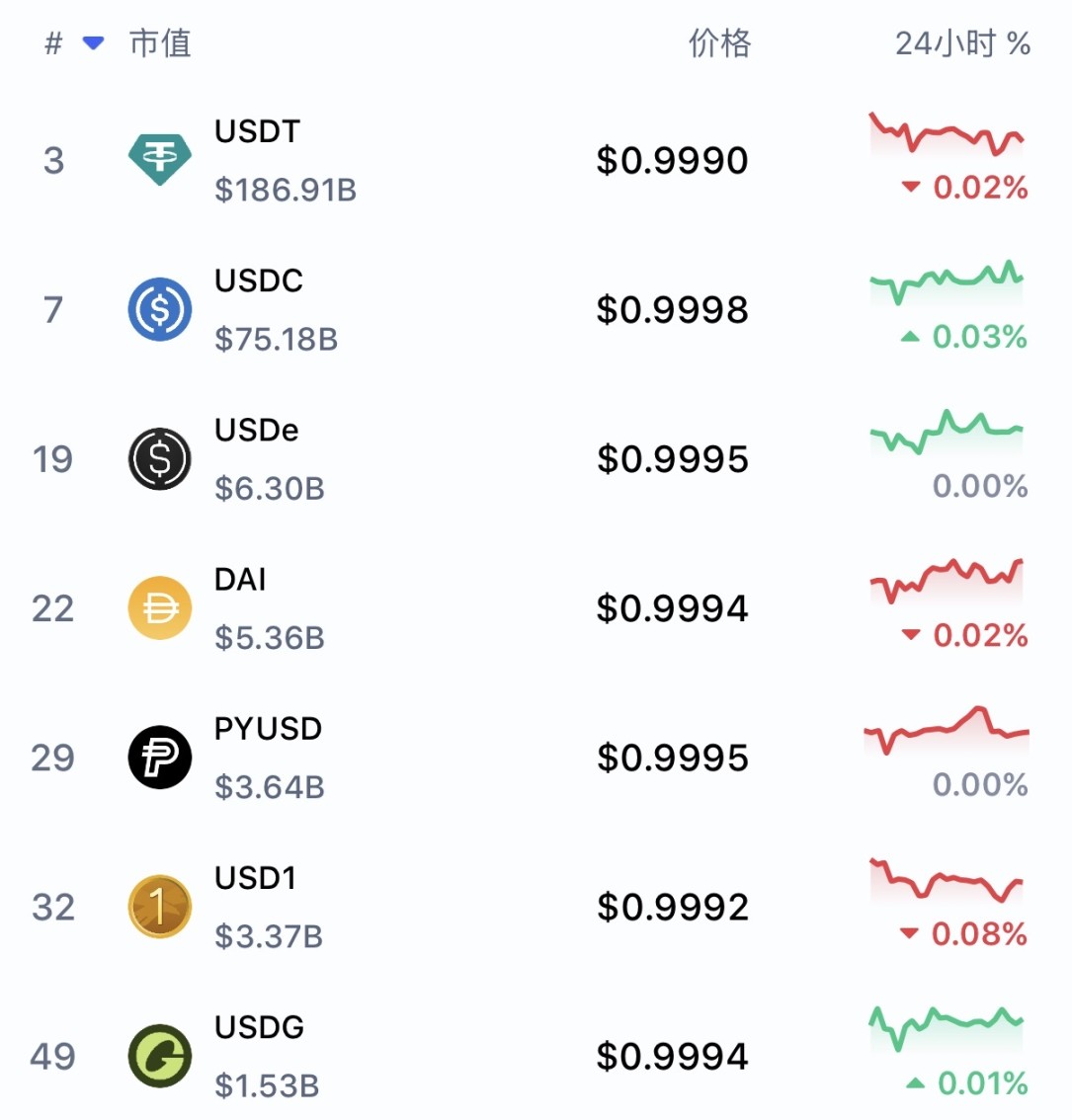

According to CoinMarketCap data, as of now, USD1's market capitalization is $3.37 billion, ranking sixth among stablecoins by market cap, approximately 1.8% of USDT's total market cap and 4.48% of USDC's total market cap.

On centralized exchanges, USD1 has gained relatively comprehensive trading support, being listed on exchanges such as Binance, Coinbase, and Upbit. Taking Binance as an example, USD1 currently has 14 trading pairs, covering assets like BTC, ETH, SOL, BNB, as well as XRP and ASTER.

Looking at the trading data from the past three days, the trading volume for the BTC/USD1 pair is approximately $5.13 billion, while the ETH/USD1 pair is about $38.9 million. For comparison, the BTC/USDT volume during the same period was around $5 billion, and ETH/USDT reached $3.59 billion; BTC/USDC volume was about $1.44 billion, and ETH/USDC was approximately $1.06 billion.

This comparison reflects a relatively clear reality: although USD1 is usable on exchanges, its liquidity scale for spot trading of mainstream assets still lags significantly behind USDT and is orders of magnitude behind USDC. At least at this stage, USD1 appears more like a stablecoin introduced to the market rather than a foundational settlement asset with established natural trading preference.

The recent rapid growth in USD1's issuance is closely related to incentive measures. On December 24, 2025, Binance launched a fixed annualized savings activity for USD1 with a maximum annualized yield of 20%. Before the activity began, USD1's circulation was approximately 2.7 billion tokens, which then quickly climbed and surpassed 3 billion tokens.

On January 5, 2026, WLFI officially announced that a governance proposal regarding 'using a portion of the unlocked treasury funds to incentivize USD1 adoption' had passed, with 77.75% approval votes. This proposal marks WLFI's intention to continue expanding USD1's use cases through more direct resource investment.

During this period, the market also experienced brief fluctuations related to liquidity structure. On December 24, 2025, a relatively large market order briefly drove down the BTC/USD1 quote, causing the price to rapidly spike down (or 'wick') to $24,111.22 near $87,000, with a daily amplitude of 73%.

On December 26, according to informed sources, due to Binance's savings activity attracting a large number of users to exchange USDT for USD1, USD1 once traded at a premium of about 0.39%. Some funds subsequently sourced USD1 through lending markets and gradually sold it on the spot market to meet demand. Because the BTC/USD1 trading pair had relatively thin initial liquidity, it caused a rapid wicking situation. CZ explained that the pair was not included in any index, thus it did not trigger liquidations, and the related volatility reflected more the fact that liquidity for the new trading pair had not yet been fully established.

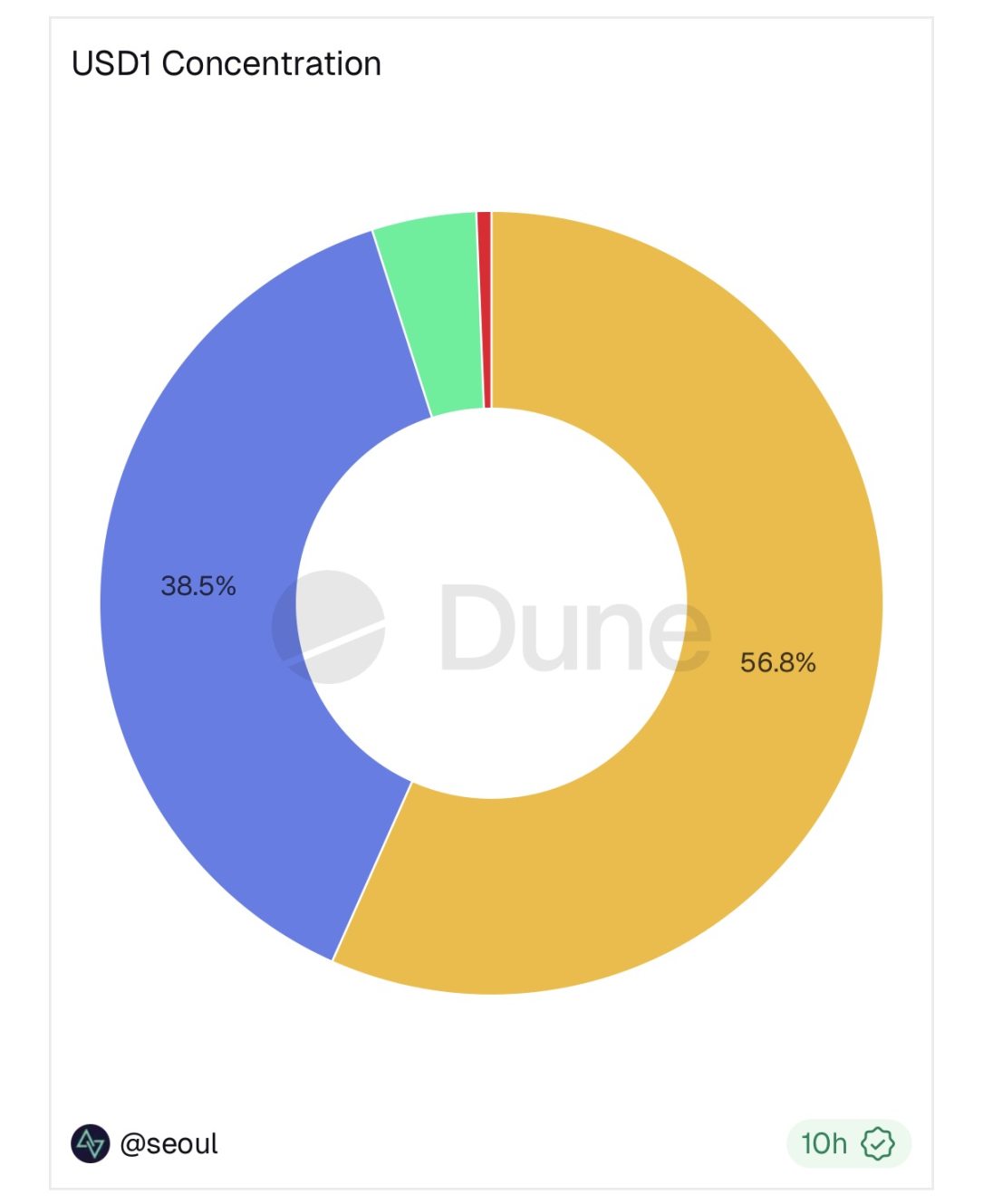

As of January 8, 2026, USD1's market capitalization is approximately $3.37 billion. From an on-chain distribution perspective, its issuance is primarily concentrated on BSC and Ethereum mainnet, at approximately $1.91 billion and $1.3 billion respectively, together accounting for the vast majority. In contrast, the scale of USD1 on the Solana network is about $143 million, a significantly lower proportion. Although WLFI continues to emphasize support for the Solana Meme ecosystem in its narrative and partnership directions, the actual on-chain volume indicates that USD1 currently still relies mainly on the liquidity structure of traditional EVM networks.

Compared to centralized exchanges, WLFI is also trying to promote the use of USD1 through on-chain scenarios. In September 2025, WLFI announced partnerships with Solana's Meme launch platform BONK.fun and the decentralized exchange Raydium to introduce USD1 as a trading pair into the related ecosystem.

On January 6, Raydium released data showing that USD1's trading volume on the Solana network in the past 24 hours was approximately $295 million.

Additionally, WLFI disclosed purchases of Meme tokens like B and 1 to support community development. Such collaborations provide USD1 with scenarios closer to native on-chain use, but the related demand still largely depends on community activity and阶段性 market sentiment, and its sustainability remains to be seen.

Furthermore, on January 8, WLFI disclosed that its affiliated entity, WLTC Holdings LLC, has applied to the U.S. Office of the Comptroller of the Currency (OCC) to establish the World Liberty Trust Company, National Association (WLTC). This institution is positioned as a national trust bank specifically serving the issuance, custody, and related financial activities of the USD1 stablecoin.

According to WLFI's explanation, the core goal of establishing WLTC is to integrate the issuance, redemption, custody, and exchange functions between USD1 and the U.S. dollar within a single, highly regulated entity. WLFI stated that USD1's circulation scale exceeded $3.3 billion within one year of launch and has been used by some institutions for cross-border payments, settlement, and treasury management scenarios.

If the application is approved, WLTC plans to offer three core services to institutional clients under the federal regulatory framework: minting and redeeming USD1, providing on/off ramps between U.S. dollars and USD1, and custody and conversion services for USD1 and other stablecoins. These services are initially planned to be offered with no fees.

WLFI also emphasized that the proposed trust bank will comply with regulatory requirements including anti-money laundering, sanctions screening, and cybersecurity, and will adopt institutional arrangements such as customer asset segregation, independent reserve management, and regular audits. The institution will operate under a regulatory structure compliant with the GENIUS Act.

Regarding existing partnerships, BitGo will continue to be an important partner for USD1 after WLTC officially begins operations, supporting its subsequent development.

World Liberty Financial was established in 2024 as a project focused on decentralized finance. Public information shows that the project has close ties to the Trump family in terms of structural design and market promotion, with related members playing roles in project promotion and ecosystem dissemination. USD1 is a U.S. dollar-pegged stablecoin launched by WLFI in March 2025, aiming to provide a settlement asset on-chain that can be exchanged 1:1 with the U.S. dollar for use in cross-border payments, DeFi activities, and liquidity needs in digital asset markets.

According to information disclosed on WLFI's official website, each USD1 token is backed by an equivalent reserve of U.S. dollar assets, primarily consisting of U.S. dollar cash, short-term U.S. Treasury bills, and other cash equivalents. The related assets are custodied by BitGo Trust Company and its affiliated entities, with BitGo also handling the issuance and redemption functions for USD1. Eligible BitGo clients can directly redeem USD1 1:1 for U.S. dollars, while other holders need to complete redemption through trading platforms supporting USD1 or regulated custodians.

Similar to other centrally issued, compliance-oriented stablecoins, USD1's official disclosure also clearly lists multiple risks. Its core constraints mainly focus on several aspects: USD1 is not legal tender and does not enjoy deposit insurance; direct redemption is only available to eligible BitGo clients; although the reserve assets are primarily high-liquidity assets, they may still face liquidity pressure in extreme situations;同时, changes in regulatory policies, address freezing mechanisms, and risks associated with third-party platforms may all affect the use and circulation of USD1.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush