Author: Gu Yu, ChainCatcher

Just a few days into 2026, the most dismal public offering of a well-known project in the crypto industry in recent years may have already occurred: nearly 30 hours after the Infinex token public sale launched, the subscription amount was only $460,000, less than 10% of the target.

It's important to note that the Infinex project team had already considered the bleak market conditions and made significant concessions in valuation, fundraising targets, and terms. The valuation for this public offering was drastically reduced from the $300 million announced last November to $100 million, and the planned fundraising amount was cut from $15 million to $5 million.

Even with such drastic adjustments, Infinex's public offering still met with a cold reception from the market, which came as a surprise to many observers. After all, Infinex, as a star project, had previously raised over $60 million, and its founding team and investor background are very impressive. Infinex's situation is a true reflection of the current downturn in the crypto market.

What is the Infinex Project?

Founded by DeFi OG and Synthetix founder Kain Warwick, Infinex became independent from Synthetix in 2023. Initially positioned as a decentralized perpetual contract protocol, it has gradually evolved into a comprehensive crypto application that allows users to seamlessly switch between different DeFi protocols and chains on a unified interface. Its current focus is on perpetual contracts based on Hyperliquid, cross-chain bridging and trading, multi-chain asset management, yield earning, and other functions.

Another main feature is its use of a new security architecture centered on on-chain smart accounts and keys, which replaces traditional seed phrases and email modes, making login more convenient and faster. It also supports using biometric technology (touch or face ID) for on-chain transaction signing.

Overall, Infinex aims to be user-experience oriented, emphasizing lowering user barriers, integrating multi-chain liquidity, and attempting to solve the long-standing issues of complexity and asset fragmentation in DeFi at the product level.

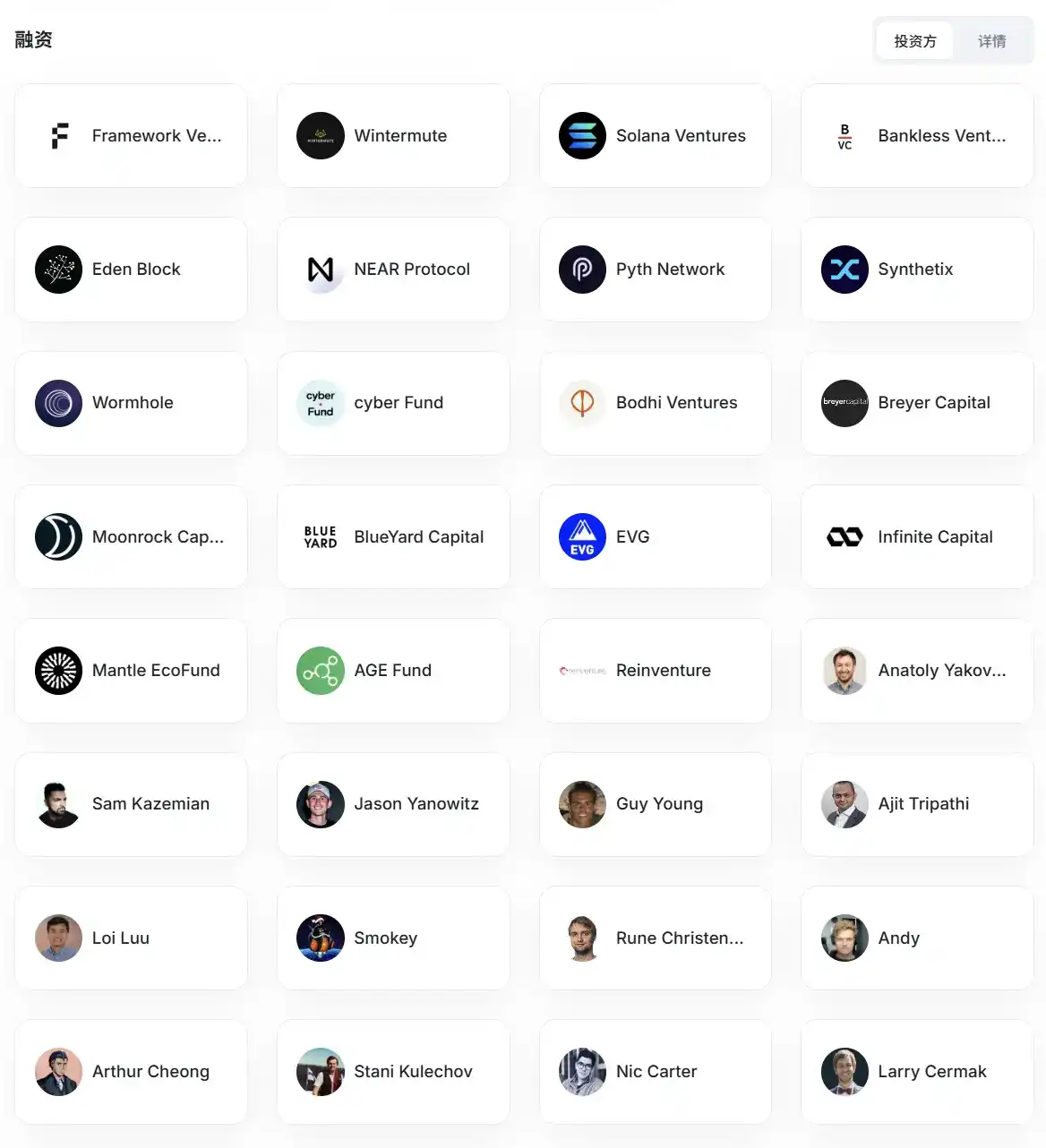

In October 2024, Infinex recently raised $65.3 million in sponsorship revenue by selling "Patron NFTs," which were sold in four rounds to retail traders, venture capital firms like Solana Ventures and Breyer Capital, and well-known individuals such as Solana founder Anatoly Yakovenko and Aave founder Stani Kulechov, totaling 41,252 NFTs.

Infinex recently revealed in an article that the implied valuation for this NFT financing round was $400 million, and participants have priority allocation rights in the latest public sale round.

Infinex Investor Lineup Source: RootData

Why Did the Public Sale Flop?

From $65.3 million to $460,000, Infinex's public sale has experienced a stark contrast in treatment. While the bleak market is certainly a factor, the primary issue lies in the project team's strategic missteps.

According to the public sale rules, Infinex limited each address to a maximum investment of $2,500. This setting was intended to attract more participants and reduce the impact of whale addresses on token concentration. Although the intention was positive, market feedback shows that the team did not consider that the number of active on-chain users is far lower than expected in the recent sluggish market. Only 285 addresses participated in the public sale after it launched, with only 134 addresses reaching the $2,500上限.

Infinex's latest tweet response expressed a similar sentiment: "We tried to balance existing NFT patrons, new participants, and fair distribution, but the result was that almost no one was willing to participate in this sale."

All INX tokens purchased in this public sale will be locked for 1 year, which is unusually long compared to other public sales. Although buyers can choose to redeem the tokens early, the purchase valuation must be correspondingly increased to $300 million.

Furthermore, the significant valuation下调 may have also played a negative role. Although Infinex's intention in lowering the valuation was to show goodwill to the market, such a drastic adjustment objectively intensified the wait-and-see sentiment among some investors. For some participants, the "plunge-like correction" in valuation反而 reinforced their judgment of a downward trend in the overall industry expectations, rather than constituting a reason to enter.

In response to the糟糕的公募状况, Infinex announced on January 5th the removal of the per-address maximum limit and a change from random allocation to a "max-min fair distribution," also known as "waterfall allocation." Everyone's allocation will increase equally until the上限 is reached or sold out.Infinex founder Kain Warwick also tweeted that he would fund the project's operations himself if necessary.

However, even after the rule adjustments, the market still did not respond positively. As of noon on January 6th, on-chain data showed that the cumulative investment in this public sale was $1.34 million from 508 transactions, still $3.66 million short of the $5 million target. This suggests that the problem may not just be "unfriendly rule design" but rather a systematic decline in investors' interest in participating in such public sales.

The Deep Structural Contradictions of the Public Sale Model

To some extent, Infinex's public sale failure is particularly striking because it occurred at a time when "ICOs seem to be warming up."

Since the second half of 2025, as Bitcoin prices stabilized and some sectors experienced阶段性反弹, discussions about "primary market recovery" in the crypto market have gradually increased. Projects like Monad, Pump.Fun, Plasma, Falcon Finance, and others have重新 chosen token public sales for fundraising. The ICO public sale model, which had been明显边缘化 in the past two years, began to reappear in the industry's视野, with fundraising platforms like Buidlpad and echo also rising rapidly.

But rather than a return of the ICO热潮, this is more of a passive choice.

In the current environment, traditional venture capital investment frequency has significantly decreased, valuation systems have become more conservative, and fundraising cycles have been noticeably lengthened. For many projects that have not yet formed stable revenue but need continuous development investment, token public sales have become one of the few still "feasible" fundraising paths. It does not rely entirely on institutional endorsement nor require accepting extremely compressed private placement terms, theoretically allowing direct access to market liquidity.

It is against this background that more and more projects are turning to public sales. However, Infinex's experience clearly shows: a project's fundraising motivation does not equate to the market's willingness to provide capital.

More critically, this current wave of "ICO resurgence" is exposing the deep structural contradictions of the token public sale model.

On one hand, projects attempt to demonstrate restraint and rationality to the market by lowering valuations, extending lock-up periods, and emphasizing long-termism; on the other hand, investors are expressing冷淡 towards this narrative with their actions. In an environment of insufficient liquidity and limited secondary market capacity, long-term lock-ups are not seen as a value consensus but rather as a one-sided risk transfer.

In past cycles, the core appeal of public sales came from two premises: the expectation of quick circulation and market sentiment premium. Currently, both premises have significantly weakened. Token issuance is increasingly resembling a transaction of "cashing in the future early," but the market is in no hurry to price these futures.

Infinex's public sale results precisely reveal this misalignment. As more projects choose to raise funds through public sales, the market has not correspondingly expanded its risk-bearing capacity for public sale assets but has instead become more selective. The result is that even with solid project backgrounds and significantly reduced valuations, public sales can still encounter collective观望.

In the coming period, well-known projects like Zama (January 12th) and MegaETH will相继 launch their public sales. With Infinex serving as a negative example, this will be an excellent test to检验 market confidence and the effectiveness of the public sale mechanism.

In a cycle of contracting liquidity, declining risk appetite, and increasingly rational investors, any form of token issuance will face stricter scrutiny. For the entire industry, this is both pressure and an unavoidable reality check.