The ongoing West Asia crisis is still creating ripple effects across global markets. And Japan is becoming a clear case study.

Data from Trading Economics shows Japan’s 10-year bond yield climbing to 2.42%, the highest level in nearly three decades.

Rising yields point to persistent inflation pressure, leaving the Bank of Japan with little room to cut rates. Instead, markets are slowly starting to price in the possibility of further tightening.

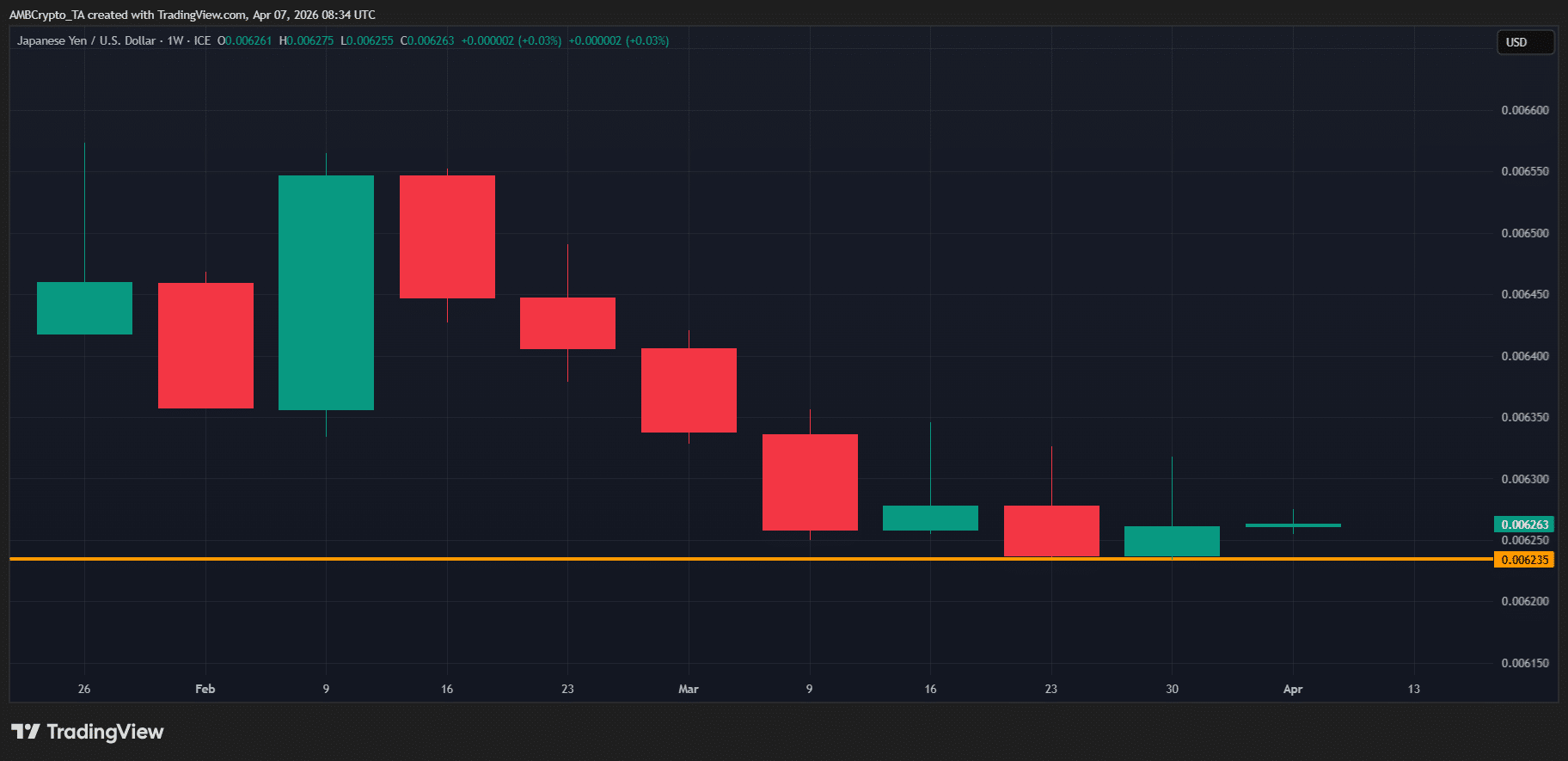

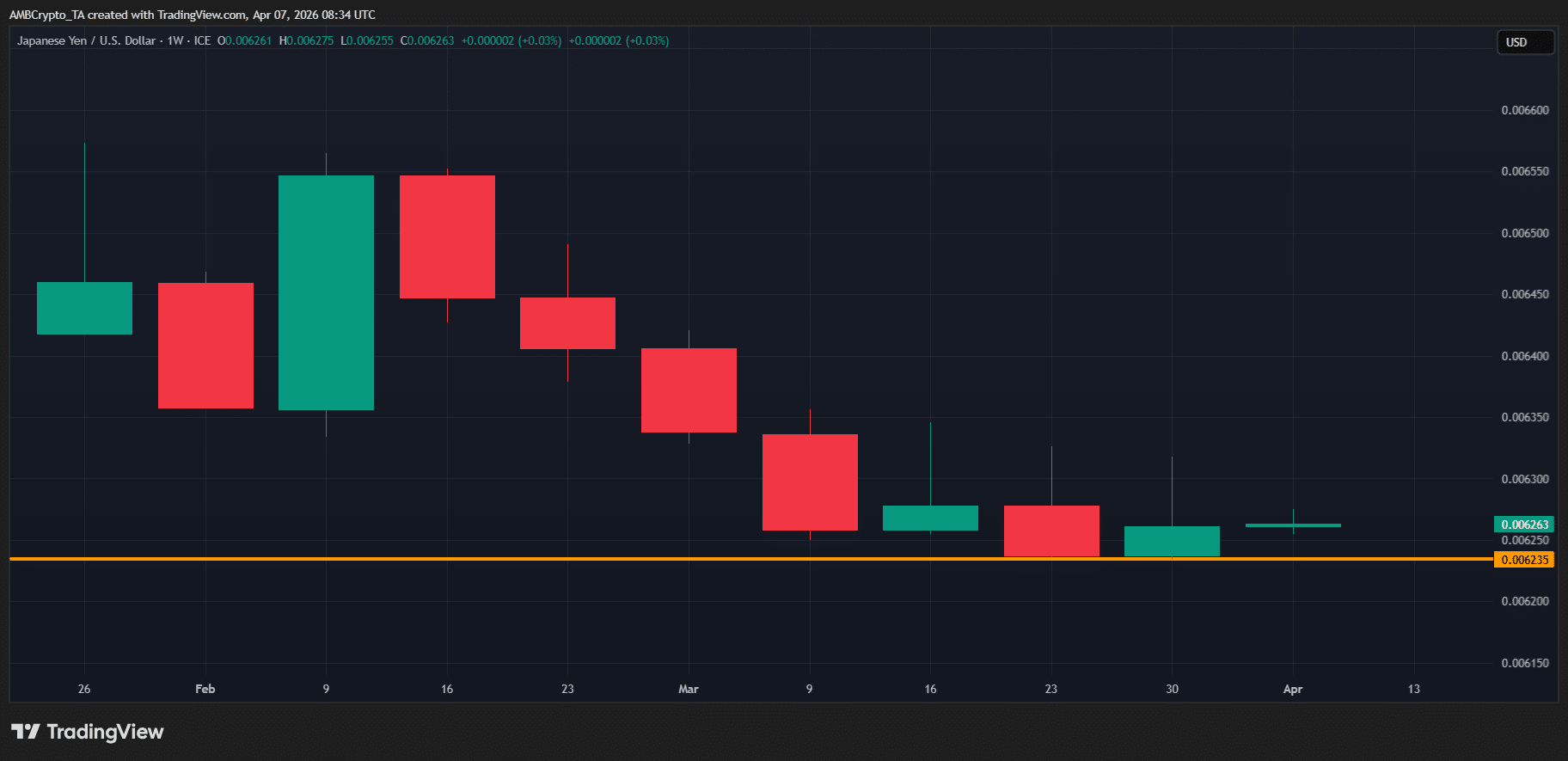

Notably, the currency market is already reacting. Throughout most of March, the JPY/USD pair moved into consolidation, and a similar structure is now forming in April, potentially signaling a local bottom.

For crypto markets, this is a macro signal worth paying attention to.

From a technical standpoint, rising bond yields usually point to capital rotating toward traditional safe-haven assets as investors prepare for tighter monetary conditions and the possibility of further rate hikes.

At the same time, the choppy behavior in the JPY/USD pair reflects the aftereffect of this adjustment phase.

In simple terms, the yen appears to be transitioning from sustained weakness into a stabilization phase. However, the bigger takeaway for crypto is what this means for the U.S. Dollar Index (DXY).

Historically, periods of dollar weakness have triggered capital rotation into risk assets, as yields from traditional safe havens become less competitive compared to the faster upside potential seen in equities and crypto.

Naturally, that raises a key question: Could a weaker dollar give crypto the macro tailwind it needs to break through the current FUD?

Analysts point to an overvalued dollar as crypto’s catalyst

U.S. Treasury yields are cooling off, and the dollar is starting to reflect it.

According to Trading Economics, the 10-year U.S. Treasury yield has dropped nearly 3% from its late-March peak of 4.43%, the highest level since July 2025.

This pullback highlights how ongoing geopolitical tensions have weighed on inflation and put the Fed in a tricky spot. The cooldown, however, now points to a shift in market expectations, with investors starting to price in a softer monetary stance.

Notably, the impact is showing up in markets. The DXY is down 0.35% this week after topping 100, while the total crypto market cap has rallied 3.5% since kicking off April’s run.

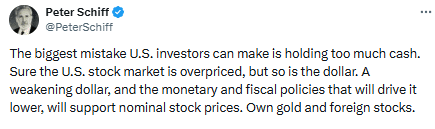

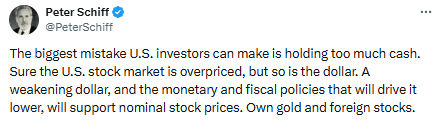

Taken together, this reinforces Peter Schiff’s point: An overvalued dollar can act as a catalyst for capital rotation into risk assets, including crypto.

In this context, Japan’s yield jumping to a multi-year high starts to carry real weight. Economically, rising Japanese yields are starting to shift global capital flows, as investors rotate into the yen and Japanese bonds, reshaping liquidity patterns.

When combined with a softening dollar, this setup becomes even more significant, creating conditions that could support inflows into risk assets like crypto.

For investors, this is a key macro signal to watch closely, highlighting where capital might flow next.

Final Summary

- Japan’s multi-year high yields are reshaping capital flows, creating favorable conditions for crypto.

- An overvalued dollar, as Peter Schiff highlights, can act as a key catalyst driving crypto inflows.