Editor's Note: As Michael Saylor continues to amplify his company's exposure to Bitcoin through tools like STRC, a seemingly efficient financial structure is simultaneously accumulating dividend pressure and potential risks. In the short term, it drives capital inflows and price increases; but once the market turns, this mechanism reliant on continuous financing could quickly backfire on the company itself. This article explores this structure, attempting to outline its operational boundaries and potential chain reactions under extreme scenarios.

Below is the original text:

Through STRC, Saylor has created a "Frankenstein's monster."

Victor Frankenstein created this monster out of arrogance—he was confident he could play God and challenge death. But after the monster successively destroyed his family and friends, it ultimately dragged him into ruin as well.

Through STRC, Saylor has designed an "idealized" BTC-linked instrument, allowing retail investors to capture Bitcoin's excess returns in a manner similar to a "risk-free rate." It is this financial engineering capability that enables him to claim unprecedented Sharpe ratios and an 11.5% return with just 1 basis point of volatility—but ultimately, this mechanism could also crush MSTR.

Note: The following analysis is based on one premise—BTC trades sideways or declines. If BTC can achieve the 20–25%+ compound growth rate assumed in Strategy's internal model, then many of these assumptions would no longer hold (though not all would be invalidated).

In just the past two weeks, STRC has attracted nearly $3.5 billion in inflows, with total issuance reaching $8.5 billion. Combined with other preferred instruments from Strategy, the outstanding amount is currently about $13.5 billion (excluding convertible bonds here). These financing proceeds have supported the corresponding scale of BTC purchases and were likely a major driver behind last week's price surge to $78,000; but at the same time, they also bring an annual dividend obligation of approximately $400 million.

Previously, Saylor maintained a dividend reserve of about $2.25 billion. Before the April issuance round, this reserve could cover about 25 months of dividends. But the new issuances in just the last two weeks have already compressed the coverage period to 18 months. To restore it to 25 months, he would need to raise about $500 million through ATM (at-the-market) offerings.

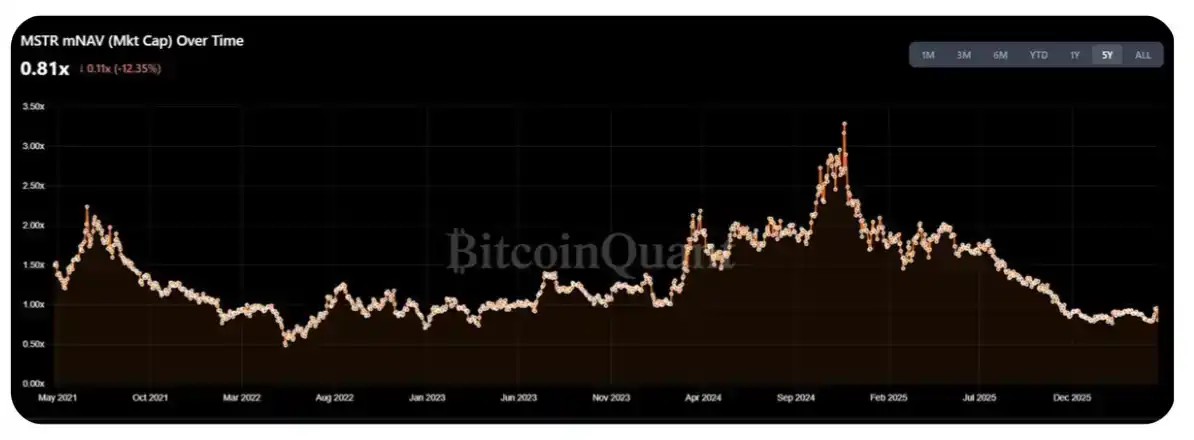

Currently, MSTR's mNAV has fallen back to 1.25–1.30 times the annual high range, which has also prompted the crypto community (CT) to call for large-scale BTC purchases again this week. However, the issue is that I believe about 50–70% of this week's new issuances will be used to replenish the dividend reserve, rather than directly for buying BTC.

More importantly, it is worth considering STRC's performance in "extreme scenarios." MSTR's current market cap is approximately $55–60 billion. The practical question is: How much more STRC can Saylor issue before the dividend burden puts substantial pressure on mNAV?

A simple estimation method: the annual issuance scale could be controlled at 1–2% of MSTR's average daily volume (ADV). Based on the current daily trading volume of about $2–3 billion and 252 trading days per year, this roughly corresponds to an issuance space of $5–15 billion—equivalent to 3–10 times the current annual dividend/coupon payments.

However, I tend to believe this range represents the "upper limit," not the常态 level. In fact, for shareholders holding only common stock, the structural cost of this trade is already becoming apparent: STRC's success is actually suppressing MSTR's mNAV—and in the震荡区间 since 2023, this metric was closer to 1.5 times (though one could argue the current environment is more like mid-early 2022).

On the surface, for common stockholders, continuing to support these "yields" that do not translate into their own upside gains seems irrational—under continuous issuance, the BTC holdings per share have not substantially increased (though this is largely due to Strategy's already massive size).

That said, DAT shareholders are a rather "special" group, and I can imagine they can withstand such pressure, at least for the next year, without necessarily adopting this view.

Additionally, the above analysis implies a key premise: MSTR can maintain an mNAV above 1 times for the foreseeable future. If it falls below 1 times, then compared to directly issuing stock, selling BTC would result in less dilution for shareholders. This would open the floodgates of supply, pushing the market into a phase of "DAT reflexivity dominating in a downturn"—a point I discussed last year (see original post).

To briefly summarize this logical chain:

STRC continues to expand;

As the scale grows, Saylor needs to pay越来越多的 dividends;

MSTR buyers gradually realize that the stock they are buying is actually financing dividends, not用于增持 BTC;

Buyers find this is not the交易结构 they initially expected and start exiting;

Once new buying dries up, mNAV falls below 1 times;

mNAV < 1 times → Saylor is forced to sell BTC instead of issuing more stock;

The market enters a panic state.

In my view, the correct way to judge STRC's maximum supply scale is to find a "tipping point": where the dividend burden from new issuances begins to exceed the marginal benefit of per-share BTC growth. A rough estimate suggests this tipping point corresponds to an annual dividend支出 of $3–4 billion, equivalent to issuing about $10–20 billion more STRC. At the current pace, it could be reached within 6 months.

Of course, Saylor still has room to maneuver. The dividend reserve does help stabilize prices and market confidence, but if the震荡 or downtrend continues, holders are essentially playing a game of "musical chairs." When the dividend reserve is down to 6 to 9 months, the rational choice might become: exiting early in the 90–95 price range, rather than bearing the downside risk of Saylor suspending dividends (another option he has).

Although STRC dividends are "cumulative," in extreme cases, I believe Saylor is more likely to choose "com sacrificing preferred stock credit" rather than being forced to大规模 sell BTC. Essentially, he faces this arithmetic problem: "If I fulfill preferred stock obligations and give up future issuance space, how much more BTC can I buy" - "the amount of BTC I have to sell to maintain preferred stock" = result

If the result is positive, choose to sell BTC; otherwise, "sacrifice" preferred stockholders

The main argument against this judgment is: once it really reaches the stage where this calculation is needed, the market has likely already turned, and MSTR's mNAV has most likely fallen below 1 times.

Thank you for reading, even if the beginning was somewhat "sensational." Also welcome any different views or criticisms. (Acknowledgments to @TraderBot888, the first person to discuss this idea with me back in the day.)