Original Author:shtanga0x&securezer0

Compiled by | Odaily Planet Daily (@OdailyChina)

Translator | Wenser (@wenser2010)

Editor's Note: Recently, posts about Polymarket's LP incentives for the NCAA "March Madness" have almost flooded the timeline on platform X. At the same time, official Polymarket members hinted at a major announcement next Monday, with community speculation pointing towards funding or a token launch.

After the U.S. SEC and CFTC cleared the obstacle for airdrops on crypto platforms using the Howey test, POLY has become the "last hope for airdrop farming" in the eyes of many, and LP market making might become one of the key metrics for the airdrop.

In light of this, Odaily Planet Daily will use the opposing views of two analysts on LP market making incentives to provide Polymarket users with a more comprehensive perspective. The following is the compiled content, with some information edited.

Positive View: The 4 Major Categories Behind Polymarket's LP Incentive Program

Recently, Polymarket's incentive mechanism underwent a low-key upgrade, shifting its focus to Liquidity Providers (LPs). For the past few years, the platform has maintained a "zero trading fee" strategy, but since the beginning of this year, it has quietly introduced fees for specific prediction markets and launched two major market maker reward programs.

On the surface, charging trading fees seems unfavorable for trading users, but in reality, it addresses the core structural pain point of prediction markets—the liquidity problem.

The new fee structure aims to fund incentive programs, rewarding users who provide limit orders and maintain order book depth. Therefore, both Polymarket and its users benefit from: narrower spreads, richer order books, and a better trading experience—especially in high-frequency crypto markets.

Its rollout path is also very clear, showing a trend from single to multiple:

- January 2026: 15-minute Crypto markets

- February 2026: Expanded to 5-minute Crypto markets + NCAAB college basketball + Serie A football

- March 6, 2026: Expanded to all Crypto markets (covering 1H, 4H, daily, weekly events, etc.)

Based on the above information, this article will detail how the new fee and reward system works—and why fees paid + rewards earned could become a potential anti-sybil indicator in the POLY airdrop. This is not a simple monetization operation; it's Polymarket showing through action that what it truly wants is liquidity, not volume-bot farming.

Part I. Complete Analysis of the New Taker Fee Mechanism

The vast majority of Polymarket markets remain completely free. Deposits, withdrawals, and trading (for most event markets) still have zero platform fees.

Trading fees currently only apply to the taker side (taker orders) and cover three types of markets:

- All Crypto up/down markets (15min, 5min, 1H, 4H, daily, weekly, etc.)

- NCAAB (US College Basketball League)

- Serie A (Italian Football League)

The key point is that taker fees only take effect for markets created after the fee activation date; existing prediction events created previously are not affected.

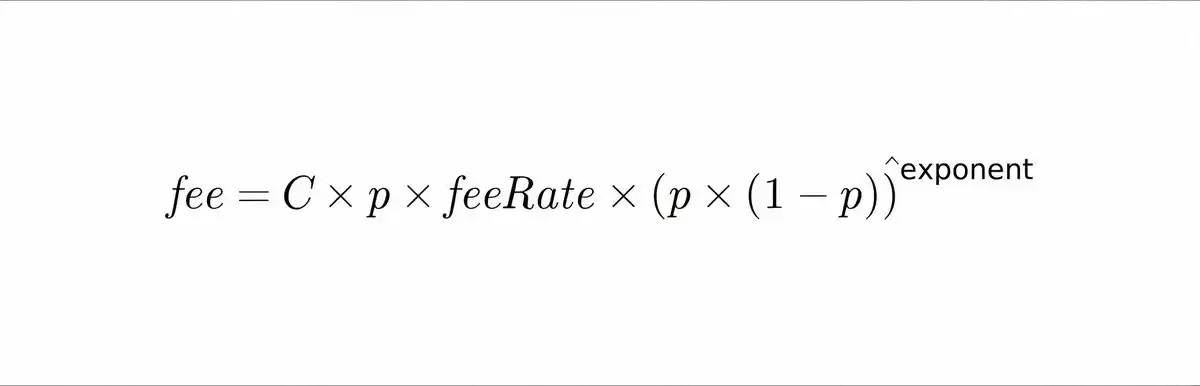

The fee formula is uniform (where C = number of shares traded, p = share price/market probability, fees rounded to 4 decimal places, minimum fee is 0.0001 USDC):

The effective fee rate follows a symmetric probability curve:

- Fees are highest when the probability is near 50% (highest outcome uncertainty);

- Fees approach 0 when the probability is near 0 or 1 (higher outcome certainty).

For example, for a $100 trade in a Crypto market:

- p=0.50 → trading fee ≈ $0.44;

- p=0.10 or 0.90 → trading fee ≈ $0.02.

The probability curve for sports events is similar, but the midpoint fee (around 50% probability) is slightly higher. The fee direction is specifically:

- Buy: Fee deducted from the share quantity;

- Sell: Fee deducted from the USDC funds;

- Market making incentives are paid in USDC.

It is worth mentioning that the Polymarket platform does not keep the entire fee pool; a fixed percentage of the fees (20% for Crypto markets, 25% for sports prediction events) is directly returned to LPs. (Note: Polymarket's US compliant platform uses a simple fixed fee of 0.01%. This analysis only discusses the global CLOB platform, which introduced the new fee system in 2026.)

Part II. Market Maker Incentive Program (Limit Order Execution Rewards)

Incentives in this section only cover markets where taker fees are collected. This means only limit orders that are executed (taken) by traders are eligible for corresponding rewards; simply placing an order without execution does not count.

The reward amount uses the same calculation method as the taker fee. Each participant's reward is proportional to their trading volume, and the total prize pool consists of a portion of the collected fees (20% for Crypto markets, 25% for sports prediction events).

Competition occurs only within specific prediction events; LP orders only compete with other LPs in the same liquidity pool for that event.

Daily incentives are sent directly in USDC to the corresponding wallet address.

Part III. Liquidity Incentives (Resting Order Incentives)

The second incentive system is provided by the Polymarket platform and applies to all prediction events (including those without fees).

The core difference is: Order execution is NOT required; you can earn money just by placing orders on the order book to provide liquidity.

Each prediction event defines several parameters that determine eligibility:

- Maximum incentive spread (e.g., ±4 cents)

- Minimum order size

- Daily total reward pool

The platform samples the order book every minute, recording 10,080 snapshots per week.

The reward calculation formula is highly detailed:

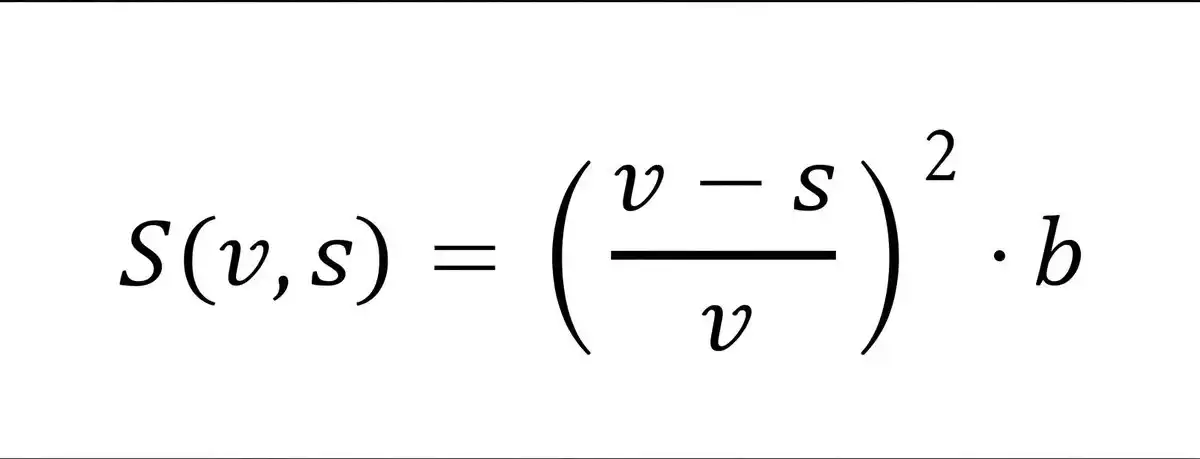

1. Distance Score (Quadratic Equation)

Where,

V - Maximum incentive spread

s - Distance from the midpoint

Orders closer to the midpoint score exponentially higher.

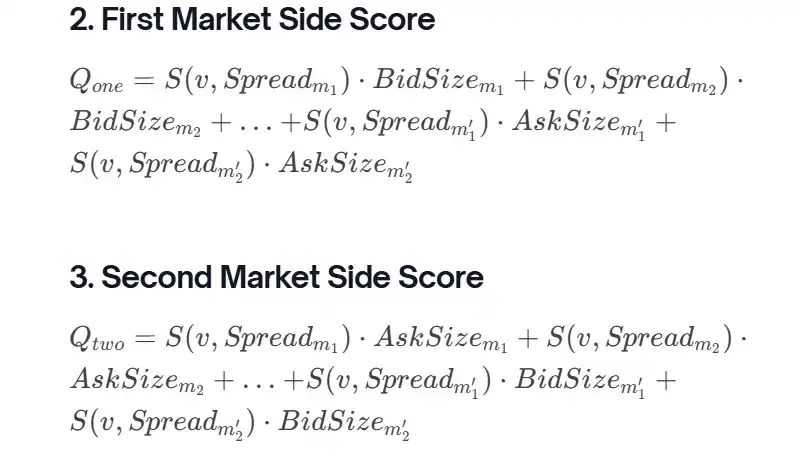

2. Two-Sided Score (YES/NO Complementary Structure)

Bid and ask orders are scored separately, considering the complementary structure of Yes/No markets.

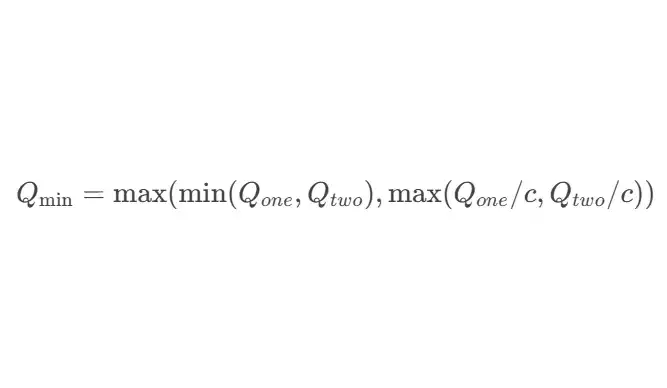

3. Q-value Minimization Adjustment

Providing liquidity on both sides of the order book scores higher points for the prediction event.

One-sided quoting is penalized unless the market probability is near 0 or 1.

4. Final Score

All LP scores are normalized and aggregated over time to determine each participant's proportional share of the market's reward pool.

Rewards are distributed in USDC at UTC midnight, with a minimum payout of $1.

Active reward prediction events and personal earnings can be viewed in real-time at polymarket.com/rewards. The incentive spread range is highlighted in blue on the order book interface. Users can also check the Polymarket official documentation.

Currently, one-sided orders can still earn points (but at a significant discount), while two-sided quoting is prioritized for incentive points. Rewards are calculated separately for each individual prediction event. There is no cross-event calculation. Effectively, the system rewards traders who maintain tight spreads and balanced liquidity near the market midpoint, enhancing the trading experience for all users.

Part IV. Sponsored LP Incentives

The third mechanism allows anyone to directly add LP incentives to specific markets using USDC, attracting LPs to provide market making. Sponsors can add or withdraw funds at any time; unused funds are automatically returned.

The rules of this mechanism are completely consistent with the Liquidity Incentive Program—just place orders, no execution required.

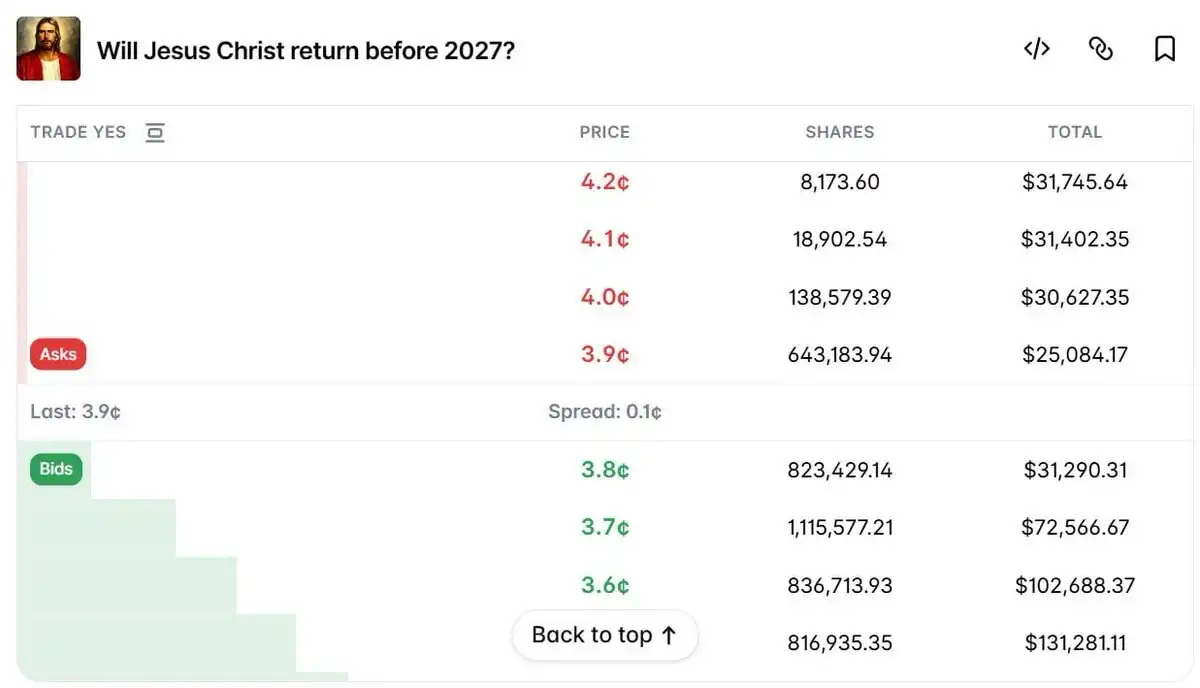

A typical case is the prediction event "Will Jesus Christ return by 2027?". A platform user invested $70,000 as an LP incentive in February and now receives about $57 per day in liquidity incentives, making this event one of the deepest markets on the platform. This mechanism allows the community itself to deeply activate market liquidity for any prediction event without waiting for official Polymarket action.

Part V. The Strongest Anti-Sybil Indicator for the POLY Airdrop

At first glance, Polymarket seems to just need more traders.

However, if most users rely solely on market orders, the platform will quickly face liquidity problems.

Polymarket does not rely on centralized market makers, so if limit orders are insufficient, the order book becomes sparse.

In this situation, it is difficult to avoid high slippage and sudden fee increases when buying, selling, or executing large orders.

Polymarket doesn't need volume-bots; it needs LPs who provide real value.

Previously, everyone only focused on trading volume, thinking high volume was the key to getting the airdrop. However, the new fee structure and reward program suggest a different incentive model—what matters is not just volume, but participation in fee-generating prediction events that need liquidity. In other words, the platform rewards targeted LP activity, not just passive limit orders.

The reward distribution formula effectively reveals the type of liquidity Polymarket values most. The scoring system evaluates:

- Proximity of the order to the midpoint

- Order size

- Balance between bid and ask prices

Therefore, rewards become a direct measure of a trader's value to the platform's liquidity. If a trader consistently earns rewards, it means their orders are actively improving market liquidity and execution quality. Here are examples of potential incentives for market participants:

- Will Arctic sea ice reach its maximum extent this winter?—Existed for 3 months, volume less than $20k, liquidity reward only $9;

- Will Bitcoin reach $75,000 in March?—Existed for two weeks, volume reached $3 million, liquidity reward $142;

- Bitcoin Up/Down - 15 minutes — Covers hundreds of prediction events, daily trading volume millions of dollars, average daily fees ~$10k, liquidity reward $2000.

More important than specific prediction events is the truth revealed by the data—taker fees and earned liquidity rewards are harder to manipulate artificially compared to simple volume metrics. Systematically earning market making incentives requires capital, risk management, and constant presence, which significantly削弱 (weakens) the advantage of airdrop farmers and instead benefits genuine market participants.

Conclusion: Taker Fees and LP Incentives May Become Key Metrics for POLY Airdrop

Future POLY token distribution may depend not only on trading volume but also on taker fees paid and LP rewards earned. These metrics are transparent, measurable, and highly aligned with platform needs. In this model, rewards are not tied to farming volume but to contributions that truly optimize the platform's trading experience: liquidity, stability, and efficient price discovery.

In other words, the best performing LPs are the most valuable users. The most hardcore Polymarket players were never the ones with the highest trading volume, but the LPs who provide the deepest order book liquidity.

Also attached is a Polymarket LP market making guide: 《Now is the Best Time to Interact with Polymarket (Exclusive Tutorial)》

Of course, there are always different views in the market. Some believe that Polymarket's LP incentive program appears to be "spending money to buy liquidity" but is actually profiting from it, setting a trap for LP users. Let's hear the opposing view.

Opposing View: Is Polymarket's LP Incentive a Platform Scam? Are LPs Actually a "Pay-to-Lose" Trap?

Regarding Polymarket's recently launched LP incentive program, arbitrage trader and Polymarket/Kalshi bot player securezer0 directly called the much-hyped "Polymarket Rewards Farming" within the circle a massive psychological warfare operation, pointing out that it is a collective hype campaign paid for directly by the platform or heavily incentivized KOLs.

The Truth for LPs: Another Form of "Paying to Lose Money"?

Multiple LPs stated bluntly: The current LP mechanism on Polymarket is essentially "spending money to incur losses".

Where is the problem? The leaderboard directly incorporates LP rewards into the P&L data display but remains silent on a key concept—LP wear and tear (impermanent loss).

When your position gets filled on one side, it often cannot be sold at a reasonable price, or cannot be sold at all before the event resolves. This part of the capital loss is systematically hidden by the platform. The real ROI data is much lower than the book value. For most LP participants, the profit is actually negative. They just believe the POLY airdrop will cover the losses—this is not an arbitrage incentive program; it's a trade based on platform faith.

Why Are Professional Market Makers Reluctant to Enter?

Professional market makers generally avoid Polymarket LP market making for one core reason: Insider trading risk is real.

Both Polymarket and Kalshi had to offer equity in exchange for liquidity to get professional market makers to the table—this in itself speaks volumes.

Effective LP operation is an extremely complex automated risk control system. The myth of "low barrier to entry, high returns" for LPs only holds true if Polymarket continues to heavily subsidize liquidity rewards—a path that is fundamentally unsustainable in the long run.

The Platform's Real Dilemma: Needing to "Create" Millions of Dollars Out of Thin Air Daily

Insufficient liquidity is the primary driver behind Polymarket gradually turning on the fee switch.

To maintain liquidity rewards for various prediction events and keep more USDC liquidity on the platform, Polymarket needs to consume millions of dollars daily to maintain trading depth. If a better solution cannot be found, the platform has no choice but to charge fees on every buy and sell, using this revenue to support investors and market makers.

Once fees are fully implemented, ordinary users will be in an extremely awkward position—because traditional sports betting platforms might actually be more cost-effective, for the following reasons:

- Odds are comparable after factoring in fees;

- Traditional platforms offer cashback and monetary incentives;

- Rules are clear and regulated;

- Insider traders face account bans and even prison risks.

3 Viable Solutions: Fixed Fees on Profit, POLY Liquidity Pools, Extended Product Fees

Instead of seeking a quick fix that worsens the situation, it's better to address the root cause: Target the vampires, not the users. Charge fees on the arbitrage bots that extract USDC from real users. After all, these bots are the source of polluted liquidity. Specifically, the methods are:

Charge a fixed 1% fee only on profits, i.e., only on the net gain (sell price minus cost basis), not touching the principal, thus not harming the user trading experience.

Build a native liquidity pool with POLY tokens. Provide liquidity programmatically at the protocol level for various prediction events, deeply binding token economics with liquidity provision.

Charge on extended products, not the core product. Parlays, derivatives, leverage—these are natural fee scenarios; touching these won't damage the fundamental user experience.

Currently, the moat of Polymarket's platform business still needs strengthening. Zero fees and better odds are its most important value anchors区别于 (differentiating it from) traditional betting platforms. Abandoning these two points for short-term revenue is tantamount to self-sabotage.