Author: Zen, PANews

Telegram has recently been in the spotlight again due to financial information circulating among investors: revenue is rising, but net profit is turning downward. The key variable here is not a slowdown in user growth, but the decline in TON's price, which has transmitted volatility from the asset side into the income statement.

The sale of over $450 million worth of TON tokens has led the outside world to re-examine its interest relationship and boundaries with the TON ecosystem.

Due to Low TON Prices, Telegram Sees Surging Revenue but Still Reports Net Loss

According to an FT report, in the first half of 2025, Telegram achieved a significant leap in revenue. Unaudited financial reports show that the company's revenue reached $870 million in the first half of the year, a year-on-year increase of 65%, significantly exceeding the $525 million in the first half of 2024; it achieved nearly $400 million in operating profit.

In terms of revenue structure, Telegram's advertising revenue grew by 5% to $125 million; premium subscription revenue surged by 88% to $223 million, nearly double the same period last year. Compared to these two items, the key factor in Telegram's revenue growth mainly comes from the exclusive agreement signed with the TON blockchain—TON became the exclusive blockchain infrastructure for Telegram's mini-app ecosystem and brought Telegram nearly $300 million in related revenue.

Therefore, overall, Telegram continued its strong growth momentum from the mini-game boom ignited in 2024 in the first half of last year—in 2024, Telegram achieved its first annual profit, with profits as high as $540 million, and annual revenue reached $1.4 billion, far exceeding the $343 million in 2023.

Of the $1.4 billion revenue in 2024, about half came from its so-called "partnerships and ecosystem," roughly $250 million from advertising, and $292 million from its premium subscription service. Clearly, Telegram's growth is partly due to the surge in the number of paying users, but even more so due to the收益 brought by its cryptocurrency-related collaborations.

However, the high volatility of cryptocurrencies has also brought risks to Telegram. Even though it achieved nearly $400 million in operating profit in the first half of 2025, Telegram still reported a net loss of $222 million. Informed sources stated that this was because the company had to revalue its held Ton token assets. Due to the持续低迷 of altcoins in 2025, the price of Ton tokens持续下跌 throughout 2025, falling by over 73% at its lowest point.

Selling $450 Million: Cashing Out or Upholding Decentralization理念

Accustomed to the long-term低迷 of altcoin prices and the floating losses of many DAT-listed companies, retail investors were not too surprised by Telegram's losses due to the depreciation of virtual assets. What surprised and displeased the community more was the FT report stating that Telegram had sold off a large amount, with its TON token sales exceeding $450 million. This figure exceeds 10% of the token's current circulating market value.

Thus, the持续走低 of TON's price, combined with Telegram's disposal of its huge token holdings, has sparked质疑 and controversy among some TON community members and investors regarding its "selling tokens to cash out" and背刺 Ton investors.

According to the public explanation by Manuel Stotz, Chairman of the Board of TON treasury company TONStrategy (Nasdaq: TONX), all TON tokens sold by Telegram are subject to a four-year vesting period. This means these tokens cannot be circulated on the secondary market in the short term and will not cause immediate selling pressure.

Furthermore, Stotz stated that the main buyers Telegram connected with were long-term investment entities like the TONX company led by Stotz himself. Their purchase of these tokens is for long-term holding and staking. TONX, led by Stotz, as a US-listed专项 investment company for the TON ecosystem, primarily acquired Telegram's筹码 for long-term strategic purposes, not for speculative flipping.

Stotz also emphasized that Telegram's net holdings of Ton tokens did not decrease significantly after the transaction and may have even increased. This is because Telegram exchanged part of its existing holdings for vested token distributions and can持续获得 new TON income from业务 like advertising revenue sharing.综合计算, its holdings remain high.

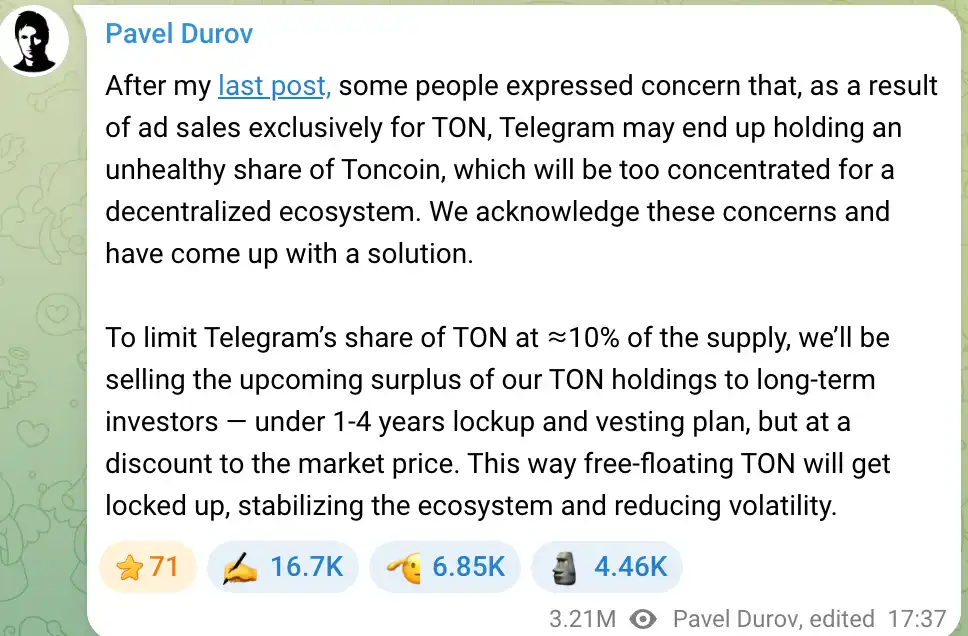

Telegram's long-term business model of acquiring TON tokens had previously raised concerns among some community members—the company holding too high a proportion of tokens is not conducive to TON's decentralization. Telegram founder Pavel Durov took this concern very seriously and stated as early as 2024 that the team would control Telegram's TON holdings to no more than 10%. If holdings exceed this standard, the excess will be sold to long-term investors to achieve wider token distribution, while also raising development funds for Telegram.

Durov emphasized that these sales would be conducted at a slight discount to the market price and would be subject to lock-up and vesting periods to avoid short-term selling pressure and ensure the stability of the TON ecosystem. This plan aims to prevent TON from being concentrated in Telegram's hands, which could raise concerns about price manipulation, and to维护 the project's decentralization宗旨. Therefore, Telegram's token selling行为 is more like a part of asset structure adjustment and liquidity management, rather than simply cashing out at high prices for arbitrage.

It is worth noting that while the持续走低 of TON's price in 2025 certainly brought impairment pressure on Telegram's financial reports, in the long run, Telegram's deep binding with TON has also created a situation of shared prosperity and loss.

Telegram has gained new revenue sources and product highlights through deep participation in the TON ecosystem, but it must also bear the financial impact of crypto market volatility. This "double-edged sword" effect is also a factor that investors must consider when evaluating its value as Telegram contemplates an IPO.

Telegram's IPO Prospects

With improving financial performance and business diversification, Telegram's上市前景 has become a focus of market attention. The company has raised over $1 billion since 2021 through multiple rounds of bond issuance; in 2025, it issued another $1.7 billion in convertible bonds, attracting participation from internationally renowned institutions like BlackRock and Abu Dhabi's Mubadala.

These financing measures not only provide Telegram with capital but are also seen as preparations for an IPO. However, Telegram's path to listing is not smooth; its debt arrangements, regulatory environment, and founder factors will all influence the IPO process.

Telegram currently has two main bonds outstanding: one is a bond with a coupon of 7% maturing in March 2026, and the other is a convertible bond with a coupon of 9% maturing in 2030. In the second $1.7 billion bond, approximately $955 million was used to replace old bonds, and $745 million was new capital for the company.

The special feature of the convertible bond is that it has an IPO conversion clause: if the company goes public before 2030, investors can redeem/convert the bonds at approximately 80% of the IPO price, equivalent to a 20% discount. In other words, these investors are betting that Telegram can successfully IPO and achieve a considerable valuation premium.

Currently, through the 2025 debt restructuring, Telegram has提前 redeemed or repaid the vast majority of the bonds maturing in 2026. Durov publicly stated that the old debt from 2021 has been largely settled and does not constitute a current risk. Addressing the impact of the frozen $500 million Russian bonds on Telegram, he responded that Telegram does not rely on Russian capital, and there were no Russian investors in the recently issued $1.7 billion bond.

Therefore, Telegram's main debt now is the convertible bond maturing in 2030, leaving a relatively宽裕的上市窗口. However, many investors still expect Telegram to seek an上市 around 2026-2027,实现债转股 and open up new financing channels. If this window is missed, the company may face long-term debt interest pressure in the future and may lose a good opportunity to transition to equity financing.

When investors measure Telegram's上市价值, they also focus on its profit prospects and抽成模式. Telegram currently has about 1 billion monthly active users and an estimated 450 million daily active users. This huge user base gives it commercial imagination space. Although its growth has been迅猛 in recent years, Telegram still needs to prove that its business model can achieve sustainable profitability.

The good news is that Telegram currently has absolute control over its own ecosystem. Durov recently emphasized that he remains the company's sole shareholder, and creditors are not involved in corporate governance.

Therefore, Telegram has the potential to sacrifice some short-term profits for long-term user stickiness and ecological prosperity without being constrained by short-sighted shareholders. This "delayed gratification" strategy is in line with Durov's consistent product philosophy and will also be the core of the growth story told to investors during the IPO path.

However, it must be emphasized that an IPO does not depend solely on financial and debt structure. FT pointed out that Telegram's potential上市计划 is currently still affected by judicial proceedings in France against Durov, and the related uncertainty makes it difficult to clarify the上市时间表. Telegram has also acknowledged in its communication with investors that this investigation may pose an obstacle.

Recommended Reading:

RootData 2025 Web3 Industry Annual Report

Xiao Hong: From Small-Town Youth to Manus CEO, The Long-Termism of a Bitcoin Believer

Binance's Power Shift: The Dilemma of a 300 Million User Empire

Has the Project Buyback红利 Really Come to an End?