The full report is freely available in PDF format.

Welcome to Strategy Watch #3

Strategy Watch was built to address a clear demand for high-signal, impartial analysis of fund-level performance and allocation trends in digital assets.

Our objective is straightforward — to make Strategy Watch a must-read monthly publication for the digital asset investment community.

Funds and allocators that contribute data and insights help shape a more complete and valuable view of the landscape. If you have insights, data, or allocation updates worth sharing, we welcome your contribution.

Present your latest initiatives and updates to a curated audience of institutional allocators.

Inside the Latest Strategy Watch

The report is structured across six core sections, each focused on a distinct dimension of institutional activity in digital assets:

01 Institutional Flow Monitor | Early stabilization as BTC/ETH outflows improve and ETF demand recovers, but conviction in spot markets remains under pressure.

02 Fund and SMA Performance | Market-neutral strategies delivered consistent gains; directional performance remains highly dispersed.

03 Strategy Deep Dive: Quant Trend Following | What’s driving quant trend performance in a difficult environment for directional strategies? Hear directly from a fund manager.

04 On-chain Vault Performance | Are ETH curators underperforming ETH staking yield?

05 Manager Monitor | Find out how more than 300 managers are expecting the crypto market to perform over the next three months.

06 Allocation Updates | A $6B pension fund increases crypto exposure as new funds and institutional strategies continue to launch.

The Premier Digital Assets Allocator Platform. Learn more

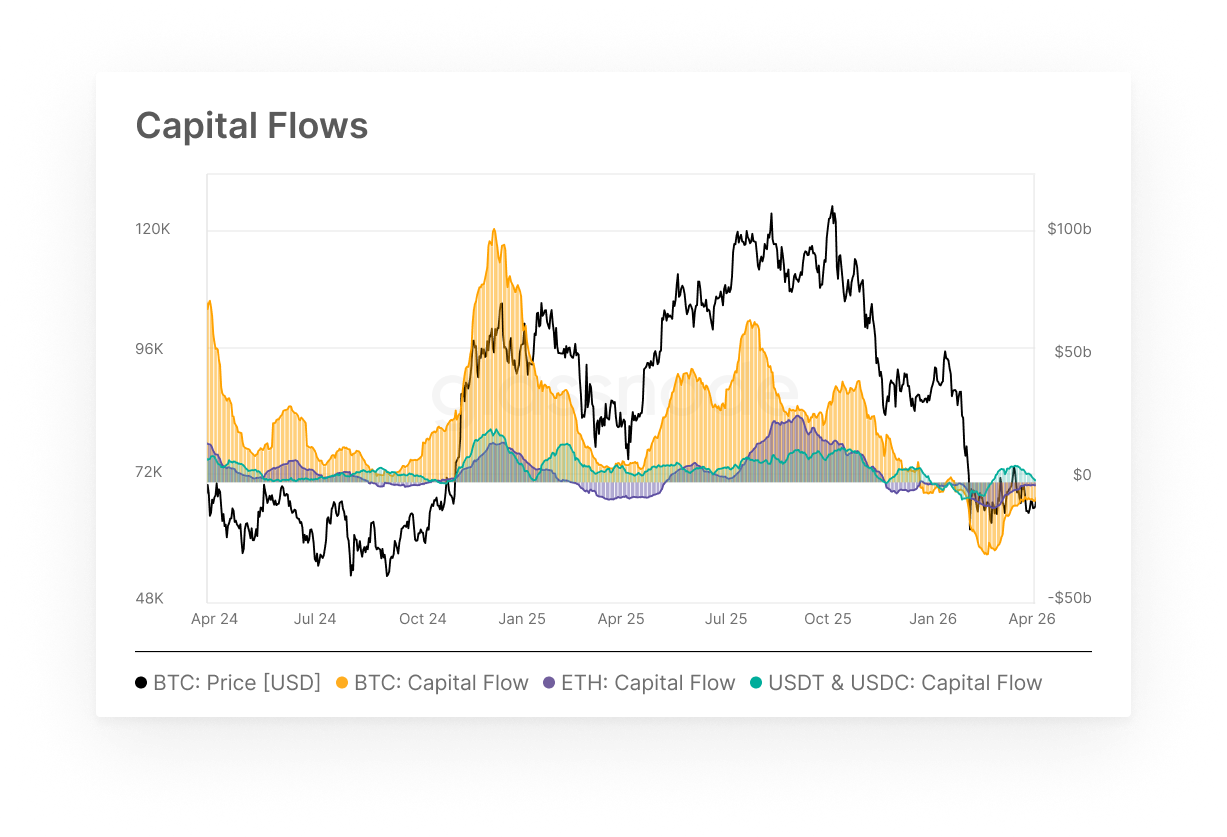

Institutional Flow Monitor

- BTC and ETH capital flows remained negative through March but continued to recover from February lows, while stablecoin inflows moderated alongside the broader stabilization.

Bitcoin and Ethereum continued to register net outflows through March, with capital flows closing the month at -$7.0B and -$1.6B respectively, a notable improvement from the -$9.6B and -$3.2B readings seen in mid-February. Stablecoin inflows also moderated to +$2.6B by month-end, easing from the +$6.2B peak earlier in March. The overall picture is one of gradual stabilization rather than recovery, with the acute phase of institutional de-risking losing momentum but conviction in spot assets remaining under pressure.

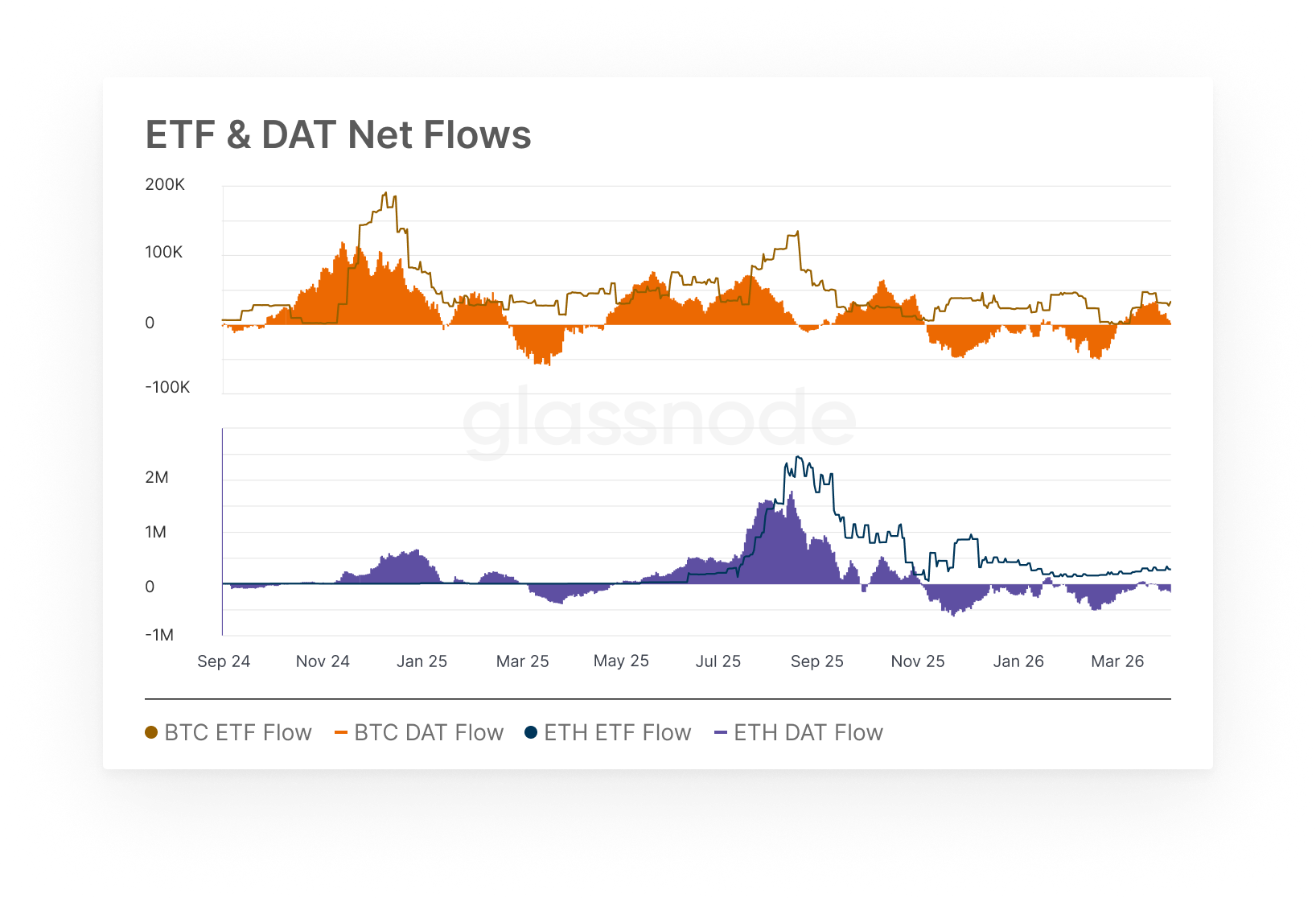

ETF & DAT Net Flows

- BTC ETF and DAT flows swung decisively positive through March, with ETH channels following at a more measured pace before both eased into month-end.

Bitcoin ETF and DAT flows finally turned positive through March, reaching intra-month highs of +30.6k BTC and +46.8k BTC respectively mid-month before settling back to +17.6k BTC and +30.9k BTC by month-end. Ethereum flows mirrored the directional shift with less intensity, as ETF flows reached +46.6k ETH and DAT flows peaked at +295.9k ETH before easing to +261.9k ETH at close. The mid-month surge followed by minor pullback, suggests demand remains sensitive to wider market conditions, rather than a true sustained structural shift in institutional positioning.

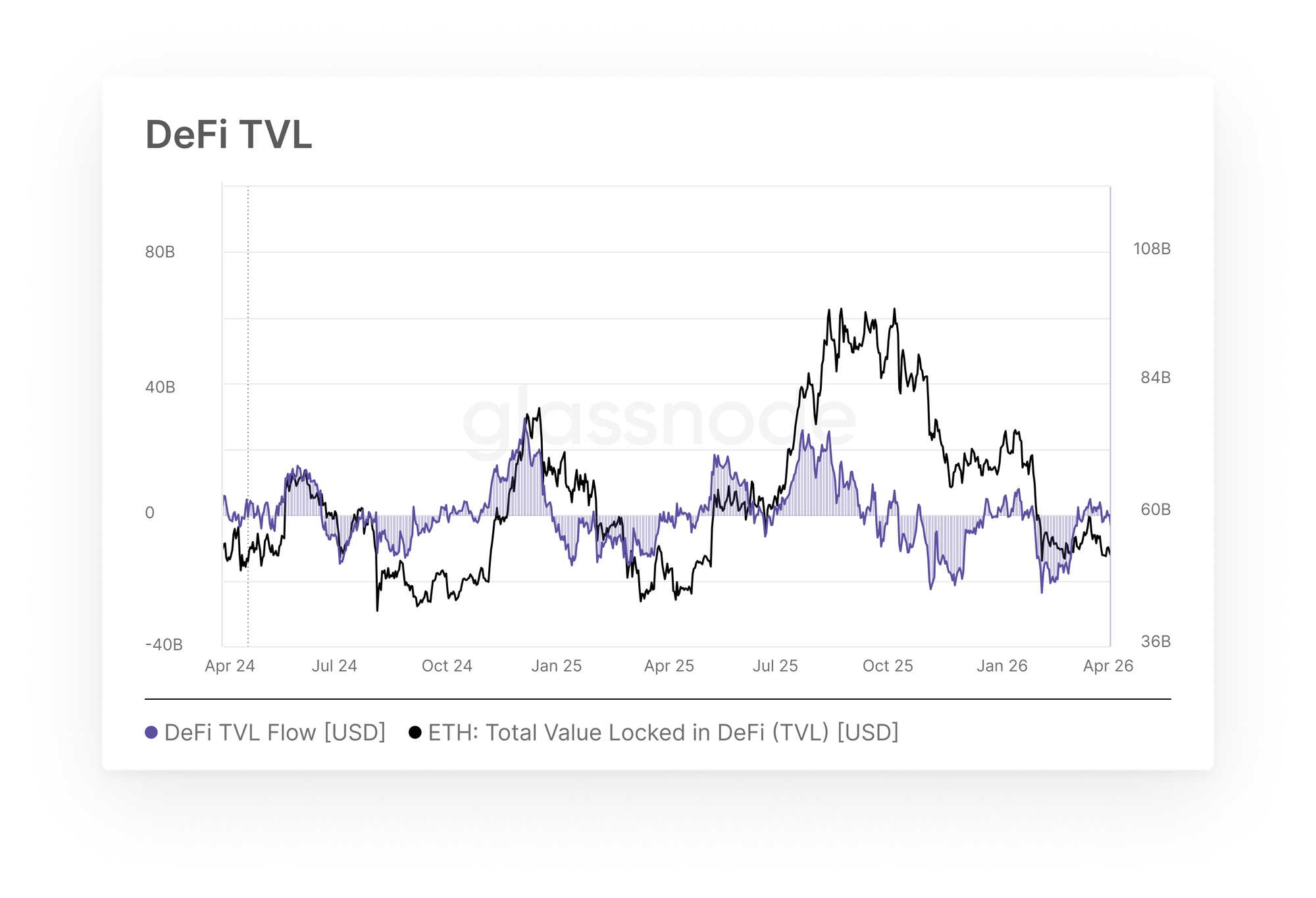

DeFi TVL & Stablecoin Cap

- DeFi TVL flows on Ethereum staged a significant recovery through March, reversing from peak February outflows to near-neutral territory by month-end.

After registering peak monthly outflows of $17.8B at end of February, Ethereum DeFi TVL flows recovered sharply through March, turning positive in mid-month and closing the period near neutral at -$0.75B. The pace of recovery was notable, with flows moving from double-digit outflows in early March to briefly positive readings around $4.9B by mid-month before settling back. While the trend shift is meaningful, a single month of stabilization is insufficient to declare a reversal of the broader contraction that has persisted since August 2025, and sustained inflows would be required to confirm a genuine return of allocator conviction in on-chain yield strategies.

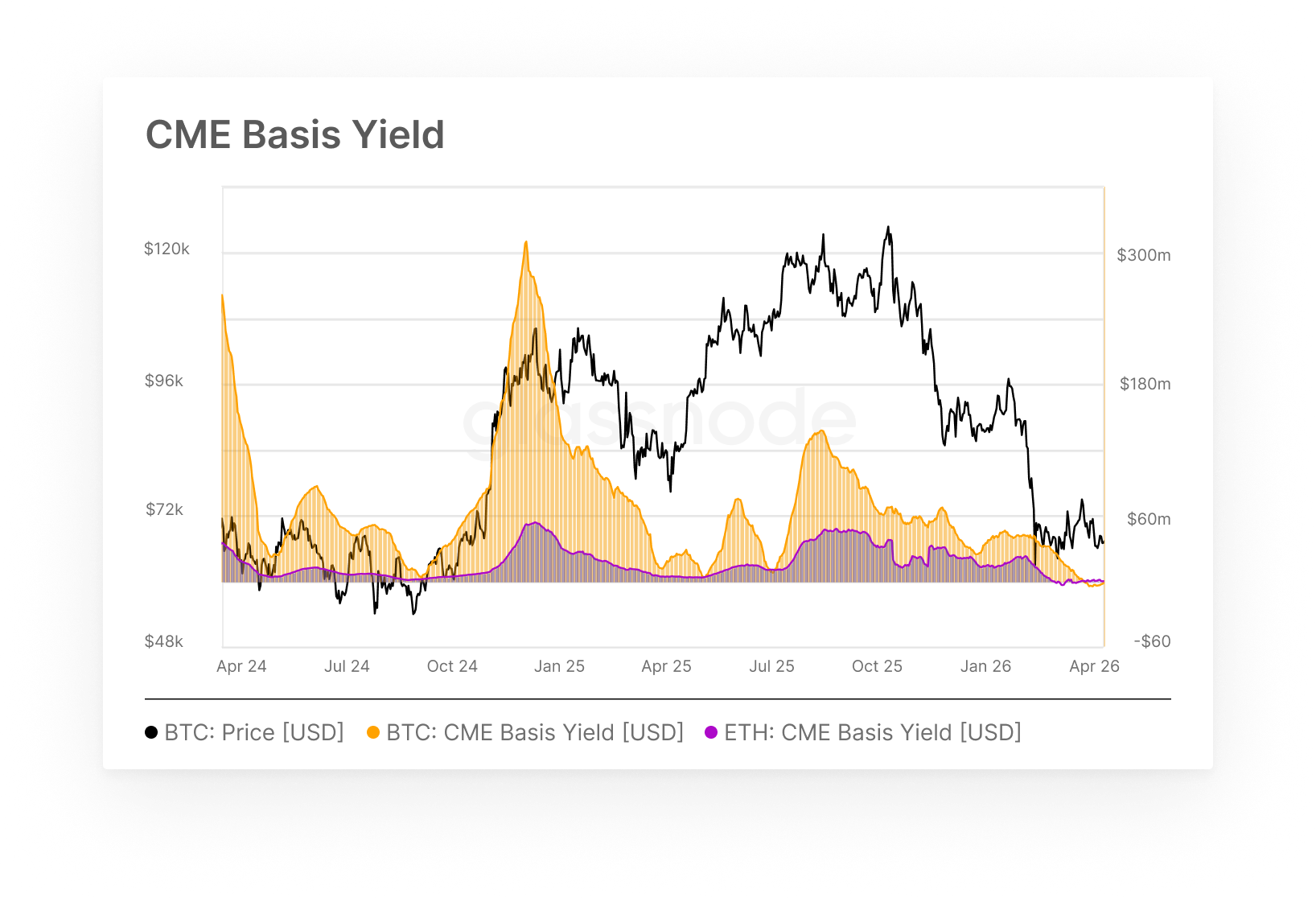

CME Basis Yield

- BTC CME basis yield turned negative through March, erasing the carry trade entirely, while ETH basis yield remained subdued but showed tentative signs of recovery by month-end.

Here we measure return available to institutions running cash-and-carry trades. After compressing through February to $17.3M/month, BTC basis yield crossed into negative territory mid-March and closed the month at -$3.9M, reflecting a full inversion of the carry premium. This signals futures are trading at a discount to spot, removing the economic rationale for market-neutral strategies entirely. ETH basis yield, already negative at end of February, oscillated in a narrow range before recovering modestly to +0.9M by month-end. Taken together, the carry environment for both assets remains structurally challenged, with meaningful recovery contingent on a sustained rebuilding of futures premium above spot.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions. Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.