Original Author: Sanqing, Foresight News

On April 13th, Eli Ben-Sasson, CEO of the ZK-Rollup infrastructure company StarkWare (behind Starknet), announced at an all-hands meeting that the company would undergo layoffs and restructure into two separate business units, focusing on revenue generation and Starknet development. The company initially launched the StarkEx scaling engine and introduced Starknet as an Ethereum Layer 2 Validity Rollup to the mainnet in late 2021. It developed its own Cairo programming language, Sierra intermediate representation layer, and a post-quantum proof system, establishing itself as a technical benchmark in the ZK Rollup field. In 2022, it completed multiple funding rounds, totaling approximately $260 million, with its valuation once reaching as high as $8 billion, making it one of the highest-valued ZK projects in the crypto industry at the time.

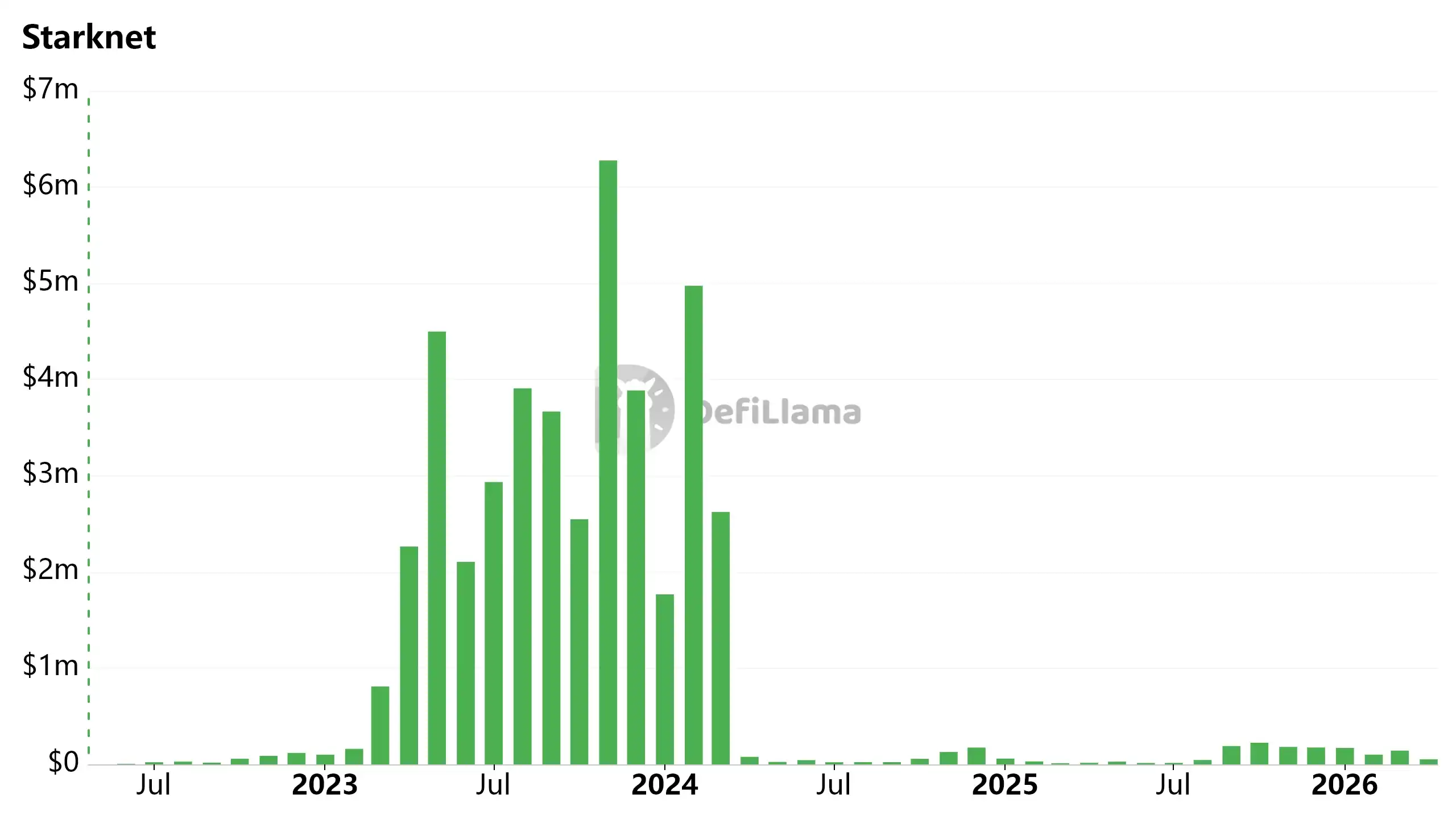

According to DefiLlama data, the Starknet network's on-chain monthly revenue peaked at nearly $6.3 million in November 2023. However, since April 2024, its monthly revenue has been only tens to hundreds of thousands of dollars, a drop of over 95%.

Starknet Chain Fees (Monthly)

Retreating from 'Infrastructure' to 'Independent Applications'

Facing a shift in identity from a 'platform infrastructure company' to a 'product-oriented technology company', Ben-Sasson admitted that the past StarkWare was "too big, too inefficient," and stated that it must now return to a startup mode, using small teams for rapid iteration to find Product-Market Fit (PMF).

Image Source: Eli Ben-Sasson's Tweet

In this industry-wide contraction, StarkWare is not an isolated case. OP Labs (the core development team behind Optimism) laid off about 20 people in March (approximately 20% of its staff), aiming to focus on core priorities, accelerate decision-making, and reduce coordination costs; Polygon Labs conducted an organizational integration after an acquisition in January, laying off about 60 people across multiple teams, although the company stated that net headcount remained unchanged.

Additionally, the exchange Crypto.com laid off 12% of its staff, the L1 Algorand Foundation laid off 25%, and several other companies or projects, including the crypto research firm Messari, underwent a new round of human resource adjustments.

After the restructuring, Chief Financial Officer Ran Grinshtein will oversee backend functions such as finance and human resources, while the frontend business will be split into two units, each with its own independent BD, engineering, and GTM (Go-To-Market) teams.

- Starknet Development Department: Led by Product Lead Tom Brand, continuing the underlying work on the core protocol.

- Applications Department: Led by Chief Product Officer Avihu Levy, tasked with the crucial responsibility of direct revenue generation, dedicated to building products that "can only be realized with the StarkWare technology stack and have minimal external dependencies."

Although the official specific product lines have not been announced, considering Levy's recent paper on achieving quantum-secure transactions (QSB) without modifying the Bitcoin protocol, and Starknet's launch of Zcash-like privacy features, quantum security and Bitcoin-related products are highly likely to be among its first trial directions.

The Impact of EIP-4844 and the Polarization of L2s

Starknet's predicament essentially reflects the collective growing pains of the entire L2 sector following the protocol upgrade.

In March 2024, Ethereum introduced EIP-4844, which significantly reduced Blob data costs, directly destroying the business model L2s relied on—"profiting from the Gas price difference between L1 and L2."

Subsequently, Ethereum continued to expand Blob supply through multiple upgrades. The Pectra upgrade in May 2025 increased the target from 3 per block to 6 per block (maximum 9); after the Fusaka upgrade in late 2025, it was further increased to a target of 14 per block and a maximum of 21 per block.

Ethereum still intends to continue gradually scaling Blob capacity through more BPO mechanisms and technologies like PeerDAS in the future, which will keep the data availability costs for L2s at an extremely low level in the long term.

When data availability costs are significantly reduced, the moat of network value is no longer cheapness, but rather its own user density and capital沉淀能力 (capital sedimentation ability).

Despite suffering the same EIP-4844 impact, the performance of the L2 market is highly polarized.

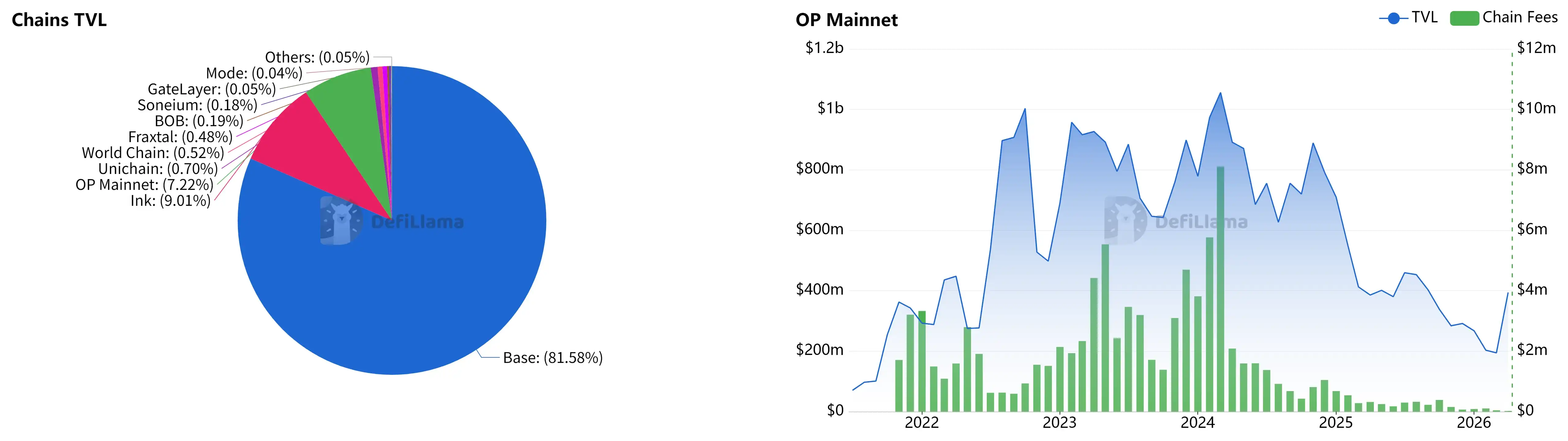

According to DefiLlama data, Base, leveraging Coinbase's strong user引流 (user diversion) and fiat on-ramp channels, garnered $75.4 million in revenue in 2025 (62% of total L2 revenue) and processed over 60% of the total network transaction volume; Arbitrum, relying on the composable financial stack formed by leading protocols like GMX and Pendle, maintained its TVL stably at the $2 billion level.

Optimism once relied on the OP Stack and Superchain ecosystem, but currently, the Superchain's TVL is highly dependent on Base (over 80%), with OP Mainnet itself accounting for only a single-digit percentage. Its TVL and on-chain fee revenue also declined significantly in 2025-2026. Making matters worse, Base announced in February 2026 that it would break away from OP Stack and transition to its own unified technology stack, further weakening Optimism's hub status in the L2 ecosystem.

Left: Superchain Chain TVL Pie Chart | Right: OP Mainnet TVL and Chain Fees (Monthly)

Starknet's situation is even more severe. Its TVL is currently only about $241 million, less than one-twentieth of Base's; its native token STRK has plummeted from the airdrop high in February 2024 to $0.033, with a total market capitalization of approximately $187 million—even lower than the company's historical total funding of $260 million.

Starknet TVL, STRK Price, and STRK Market Cap

Distribution Capability Determines Who Stays at the Table

"Infrastructure alone doesn't win the race." This statement by Ben-Sasson is a reflection on StarkWare's past eight-year strategy of "build the network and wait for users to come."

StarkWare's investment in cryptographic engineering far exceeded its peers; its from-scratch construction of the Cairo language and quantum-resistant STARK system is extremely hardcore. However, in reality, its technical purism in refusing to be EVM-compatible created a very high migration barrier for developers, which is a factor limiting ecosystem prosperity.

The core driver of L2 growth has long ceased to be technical differentiation, but rather distribution capability and strategic alliances. Currently, Base and Arbitrum together lock in nearly 75% of the total L2 value.

21Shares predicts that the L2赛道 (L2 track) will consolidate into "a slimmer, more resilient set of networks" by the end of the year. In this winner-takes-all淘汰赛 (elimination contest), retreating to self-developed applications is one of the few remaining differentiated paths for StarkWare.

Technical储备 (technical reserves) are just the entry ticket, not the finish line. What StarkWare now needs to prove to the market is no longer what cutting-edge technology it can "invent," but what products it can actually "sell."