TL;DR

· ZeroHedge believes that the opening of SPCX options could trigger a gamma squeeze, potentially pushing the stock price to $400 in an extreme scenario.

· Currently, only a volatility channel has been confirmed; $400 should not be considered a market consensus.

· Related tickers: SPCX, NVDA, MSFT, AAPL, SQQQ, SOXS.

ZeroHedge posted on social media suggesting that the opening of SPCX options could trigger a gamma squeeze, potentially driving SpaceX's stock price to $400. It is an influential and aggressive financial media outlet and trading account in the U.S. stock market, known for long-term expertise in discussing macro liquidity, positioning structures, and extreme trading scenarios together. This time, it has directly linked the listing of SPCX options, gamma squeeze, and a $400 stock price.

SPCX surged over 25% on its first trading day, with a valuation exceeding $2 trillion. Overnight and after-hours quotes briefly approached $230, but this is not the official closing price and cannot directly indicate long-term capital's willingness to accept this valuation. For the average reader, the more important point is not how many shares were issued in the IPO, but rather the limited supply of tradeable shares in the early stages of listing, highly concentrated retail buying interest, and the imminent opening of options trading.

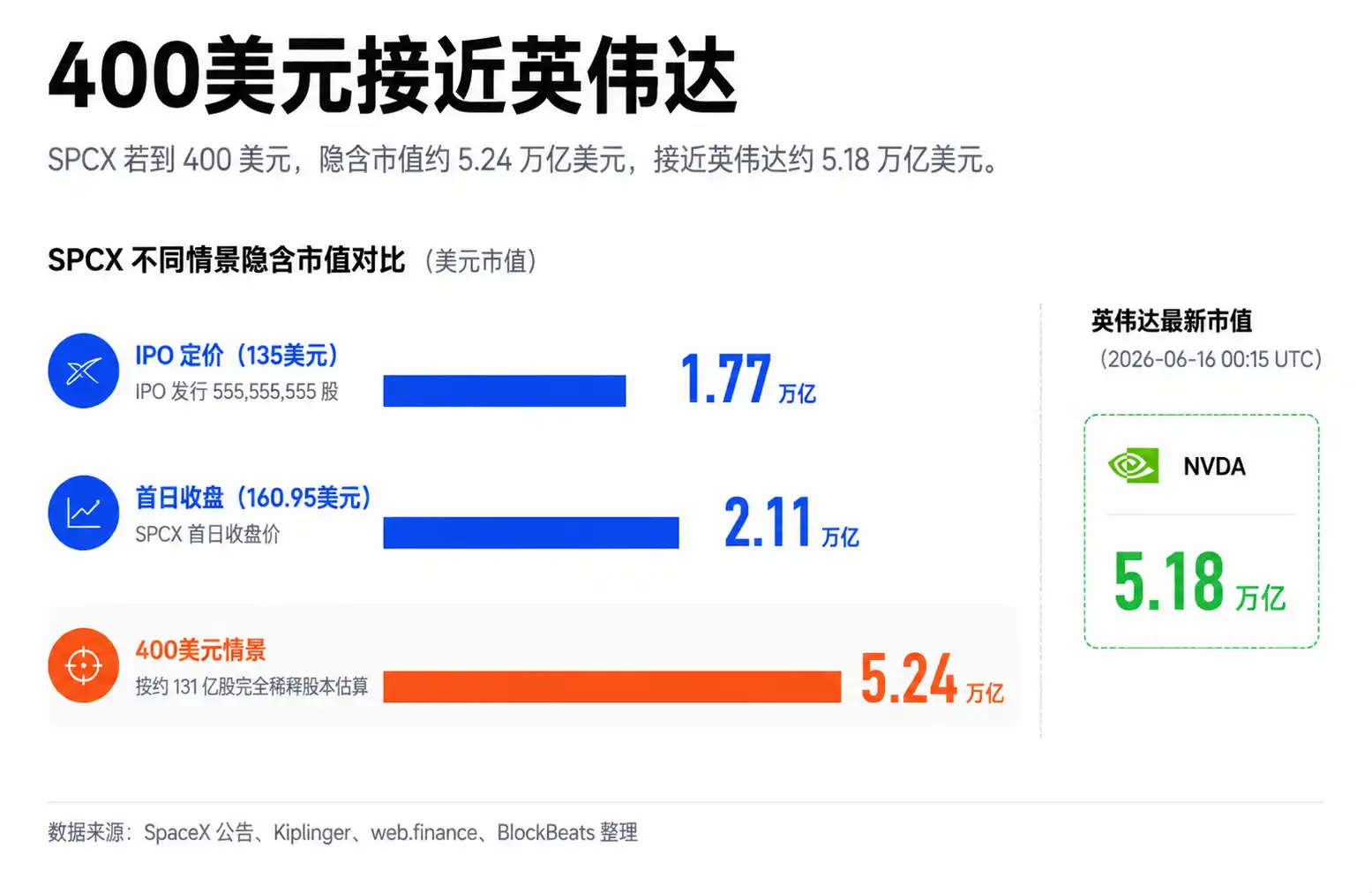

This is where the $400 claim becomes truly worth discussing: the number itself is exaggerated, but it points to a market structure that warrants caution. ZeroHedge believes that the combination of SPCX's low free float, retail buying interest, and options listing could trigger an effective gamma squeeze. Based on an estimated fully diluted share count of approximately 13.1 billion shares, $400 would correspond to a market capitalization of about $5.2 trillion, placing SpaceX very close to, or even briefly surpassing, Nvidia.

Why Can SPCX Fluctuate Like a Small-Cap Stock?

The uniqueness of SPCX lies not in the company's size, but in the limited number of shares available for trading early on.

Low free float refers to a limited proportion of shares available for free trading in the market. Even if a company's total market cap is large, if only a small portion of shares enters the secondary market initially, short-term prices become more sensitive to buying pressure. The pool is large, but the amount of water that can actually be scooped out for trading is small.

This also distinguishes SPCX from Apple, Microsoft, and Nvidia. Mature large-cap stocks have vast free floats, institutional holdings, index funds, market makers, and arbitrage capital. Moving such a stock's market cap by hundreds of billions of dollars in a day requires significant capital and broader consensus.

SPCX is in the early stages of its listing. SpaceX's official announcement confirmed the IPO share count and over-allotment arrangements, but relative to the company's overall valuation, the initial public float proportion remains low. Low free float combined with the Musk narrative could make the stock price behave more like a new issue under concentrated capital pressure in the short term, rather than a mature mega-cap stock.

This also explains why after-hours prices are closely watched by the market. After-hours trading has poorer liquidity and thinner order books. Once capital chases the same stock, price elasticity is amplified. After-hours quotes briefly approaching $230 can indicate tight share supply at that moment, but cannot directly prove long-term capital has accepted that valuation.

The first layer of ZeroHedge's $400 scenario is based on this: If a trillion-dollar company's short-term trading behavior resembles that of a low-float small-cap stock, it may experience price jumps rarely seen in normal large-cap stocks.

Options Open Adds Leverage to Volatility

Options are important because they transform retail directional bets into passive hedging demands for market makers.

According to Reuters, SPCX options are expected to start trading as early as Tuesday, with Cboe anticipating activation on Tuesday. The report cites market participants expecting heavy and volatile early trading, with expensive premiums.

For the average investor, this means SPCX no longer has only one way to play: buying the stock. After options listing, the market will see many cheaper, higher-leverage, and riskier call options.

The easiest to ignite sentiment are out-of-the-money call options, which are call contracts with strike prices above the current price. They are relatively cheap and more like lottery tickets. If the stock price rallies fast enough, returns could be high. If it doesn't reach the strike, the options can quickly expire worthless. Retail investors in hot stocks typically prefer such contracts because they allow betting on larger gains with smaller capital.

The core mechanism of a gamma squeeze occurs here.

When a large number of investors buy call options, the party selling the options is usually market makers. To manage risk, market makers often need to buy some underlying shares to hedge. As the stock price rises and options move closer to being profitable, market makers may need to buy more shares. This creates a positive feedback loop: retail buys calls, market makers buy stock, rising stock price forces market makers to increase hedges, and the rally attracts more buying.

Applied to SPCX, this mechanism is highly imaginative. It simultaneously possesses low free float, a hot narrative, retail attention, the options listing window, and the sharp price volatility already seen in the early listing period. ZeroHedge believes that if demand for out-of-the-money calls becomes sufficiently concentrated, market maker hedging purchases could push the stock price to $400 in a short period.

Boundaries must also be drawn. $400 is the extreme upside scenario presented by ZeroHedge, not a baseline judgment that current evidence alone can independently derive. The imminent opening of options only indicates a new leverage channel has appeared. To prove a gamma squeeze is forming, we would need to see actual option volume in the first days after listing, open interest in out-of-the-money calls, strike price distribution, implied volatility, and market makers' net gamma exposure.

What can be said now is that the machine has the conditions to start. What cannot be said is that the machine has definitely started.

Vanda Data Supports Crowded Trade, But Does Not Equal Widespread Euphoria

If one only looks at SPCX's price action, it's easy to think retail has fully returned to risk assets. However, Vanda's fund flow data provides another, narrower explanation.

According to ZeroHedge citing Vanda Track data, SPCX ranked first in net retail buying for the second consecutive trading day, with approximately $93.8 million in net daily purchases, accounting for about 73% of the total single-stock retail net buying in U.S. stocks that day. This data point could not be cross-verified in independent public channels this time and is better viewed as a reference for observing retail crowding, rather than a multi-source confirmed market fact.

Even so, this metric still supports part of ZeroHedge's argument: SPCX has indeed seen rare capital concentration. For a low-float stock, concentrated buying alone is enough to significantly impact the price. If options trading further amplifies this directional bet, volatility could continue to expand.

But this data also provides constraints. While there was some moderate inflow into semiconductor stocks during the same period, it did not show a state of indiscriminate, market-wide risk appetite expansion. Inverse or leveraged bearish ETFs like SQQQ and SOXS still saw buying, indicating retail is not rushing en masse into all risk assets but focusing attention on the single narrative of SPCX.

This distinction is important.

If it were broad-based risk appetite expansion, SPCX's rise could be understood as part of overall market sentiment. If it's crowding in a single asset, the faster it rises, the more fragile the positioning structure becomes. The more concentrated the capital, the stronger the short-term upward momentum, but once expectations falter, option premiums decline, or after-hours liquidity worsens, the reverse volatility could also be more severe.

This is also the most easily misunderstood aspect in comparing SPCX's market cap to Nvidia's. Nvidia's valuation stems from continuous validation of AI chip revenue, data center demand, profit margins, and long-term growth expectations. SPCX's current short-term trading is more driven by early-listing liquidity structure, the Musk narrative, and options leverage expectations. Both can command high valuations, but the supporting mechanisms differ.

$400 Awaits Validation from the Options Chain

The most important variable for SPCX moving forward is not whether more people on social media are shouting $400, but what the real options market actually looks like.

For ZeroHedge's extreme scenario to remain plausible, we first need to see sufficiently concentrated volume and open interest in out-of-the-money call options. Simply having options listed with active trading is not enough. The key is whether buying interest is concentrated in call contracts with strikes above the current price, and whether these contracts force market makers to continuously buy shares to hedge.

Implied volatility must also be considered together. When options first list, premiums may be very expensive. For buyers, even if the stock continues to rise, if implied volatility drops quickly, option gains could be erased. For market structure, high premiums can inhibit subsequent chase-buying and may lead early buyers to take profits.

Real underlying share volume and support are equally important. Low free float can amplify gains, but can also amplify losses. The high after-hours price proves tight liquidity but cannot prove long-term capital is willing to continuously absorb supply. If option buying is not as strong as imagined, or if early-stage profit-taking is concentrated, SPCX could also experience a reverse feedback loop.

Finally comes the fundamental anchor. SpaceX's long-term story is not weak; Starlink, launch services, space infrastructure, and potential communication synergies are all reasons the market is willing to assign a high valuation. However, moving from around $3 trillion to over $5 trillion in the short term looks more like an extrapolation of trading structure rather than a completed re-rating validated by financial data.

In the coming days, what investors really need to monitor is the strike price distribution on the options chain, open interest in out-of-the-money calls, changes in implied volatility, and whether the underlying stock still sees genuine volume and support at elevated prices. Only when all these data points point in the same direction will ZeroHedge's $400 scenario transition from an extreme extrapolation to a risk the market must price in.