Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web 3_golem)

SpaceX has once again made history: on July 7th (Tuesday), SpaceX was officially included in the Nasdaq 100 Index, becoming the fastest publicly listed company ever to be added to the Nasdaq 100, with a corresponding weight of about 1.3% in the index. However, this historic achievement was not reflected in SpaceX's stock price performance. According to Gate US stock data, SPCX closed down over 6.8% on Tuesday at $149.47, hitting its lowest closing price since its listing. How will SPCX perform in the future? What judgments have Wall Street institutions made?

Index Inclusion Good News Exhausted, Only Bad News Remains, Holding $150 is Already an Achievement

Prior to SpaceX's inclusion in the Nasdaq 100 Index, JPMorgan estimated it would trigger at least about $4.3 billion in passive fund inflows, and over $800 billion in assets tracking the Nasdaq 100 Index would subsequently continue to passively allocate to SpaceX.

Although this is a significant positive, since SpaceX's IPO day, "entering the Nasdaq Index" has been constantly speculated, and market expectations had already been digested. When the expectation was realized on July 7th, market sentiment was no longer able to push the stock price higher. On the other hand, the massive buying pressure behind the Nasdaq Index did not hit the market on the day SpaceX was included; in reality, most passive fund buying had been completed ahead of July 7th.

Furthermore, historical data also shows that index inclusion does not necessarily constitute a sustained upward signal and has, in some cases, become a short-term peak.

Strategy is a typical example. On December 23, 2024, Strategy was included in the Nasdaq 100, but on that day, MSTR actually opened high and closed low, falling about 7.3% to close at $332.23. Subsequently, Strategy entered a sustained downtrend, with its stock price dropping to $255.43 in February 2025. The passive buying pressure from the Nasdaq index did not become effective support for Strategy's stock price.

And after the positive news of SpaceX's index inclusion is exhausted, the well-known negative of the share unlocking wave in August will be magnified indefinitely. SpaceX's prospectus clearly states that two days after the Q2 2026 earnings report, eligible internal shareholders can sell up to 20% of their locked-up shares. If the stock price rises 30% above the IPO price by then and meets that standard for 5 days, an additional 10% can be unlocked. 22V Research strategist Jeff Jacobson estimates that insiders may sell up to 44% of SpaceX's shares before early September.

Similar to how the positive expectations of index inclusion were digested by the market in advance, the panic brought by SpaceX's share unlocking is also bound to be reflected in the price ahead of time. This is an important factor suppressing SpaceX's stock price from a market sentiment perspective both recently and in the future. BitMine Chairman Tom Lee also specifically mentioned SpaceX's upcoming share unlock in an interview, believing that one should not chase the high on SpaceX in the short term, and that using the pullback brought by the unlock to build positions is the appropriate choice.

But this past Tuesday's US market close, SpaceX was not alone in falling. According to Gate US stock data, the three major US stock indices all closed lower: the Dow fell 0.25%, the S&P 500 fell 0.45%, and the Nasdaq fell 1.16%. AI concept stocks also fell broadly: Astera Labs fell 11.52%, Ambarella fell 9.92%, Teradyne fell 9.59%, AeroVironment fell 8.09%.

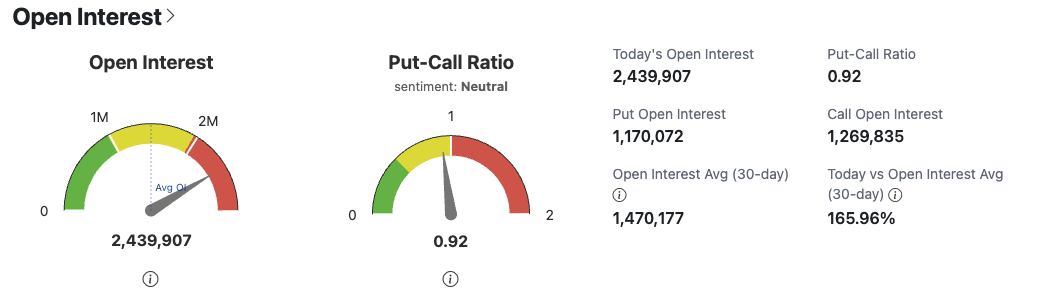

By comparison, in the context of a broad market decline and exhausted positive news leaving only negatives, SPCX still holding near $150 without breaking the IPO price is already an achievement. Meanwhile, according to OptionCharts data, the current Put-Call Ratio for SPCX is 0.92, indicating market sentiment remains neutral, not significantly bearish.

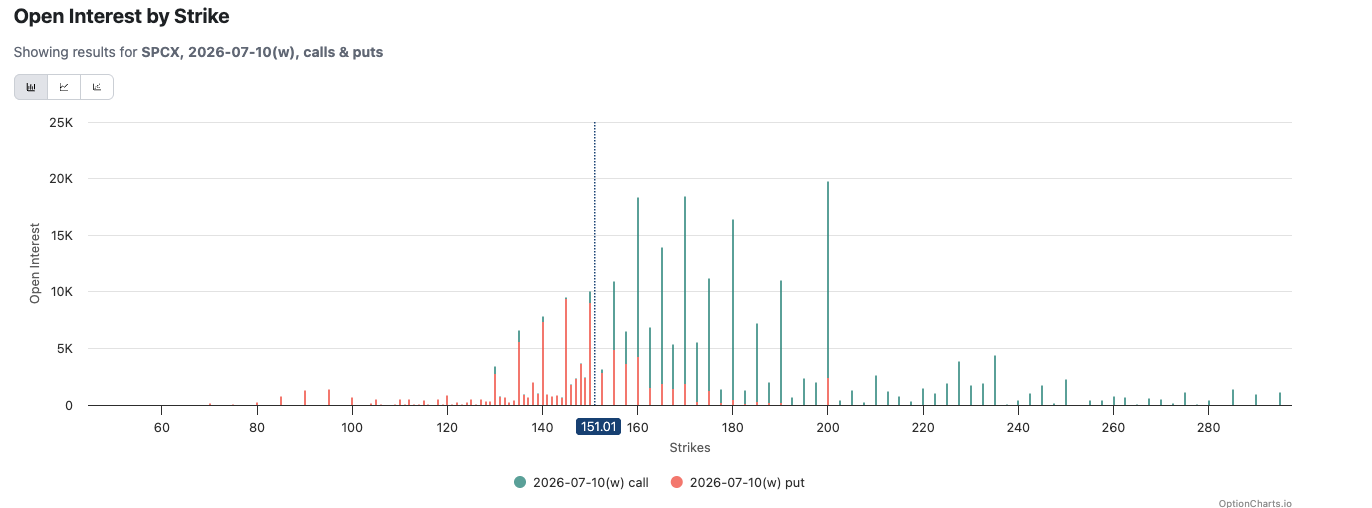

Furthermore, a large number of call options expiring on July 10th are stacked at $160 and above for SPCX, making the $150-$155 range the main battleground for bulls and bears.

Institutions Collectively Give Buy Ratings, Does SPCX Have Potential Upside?

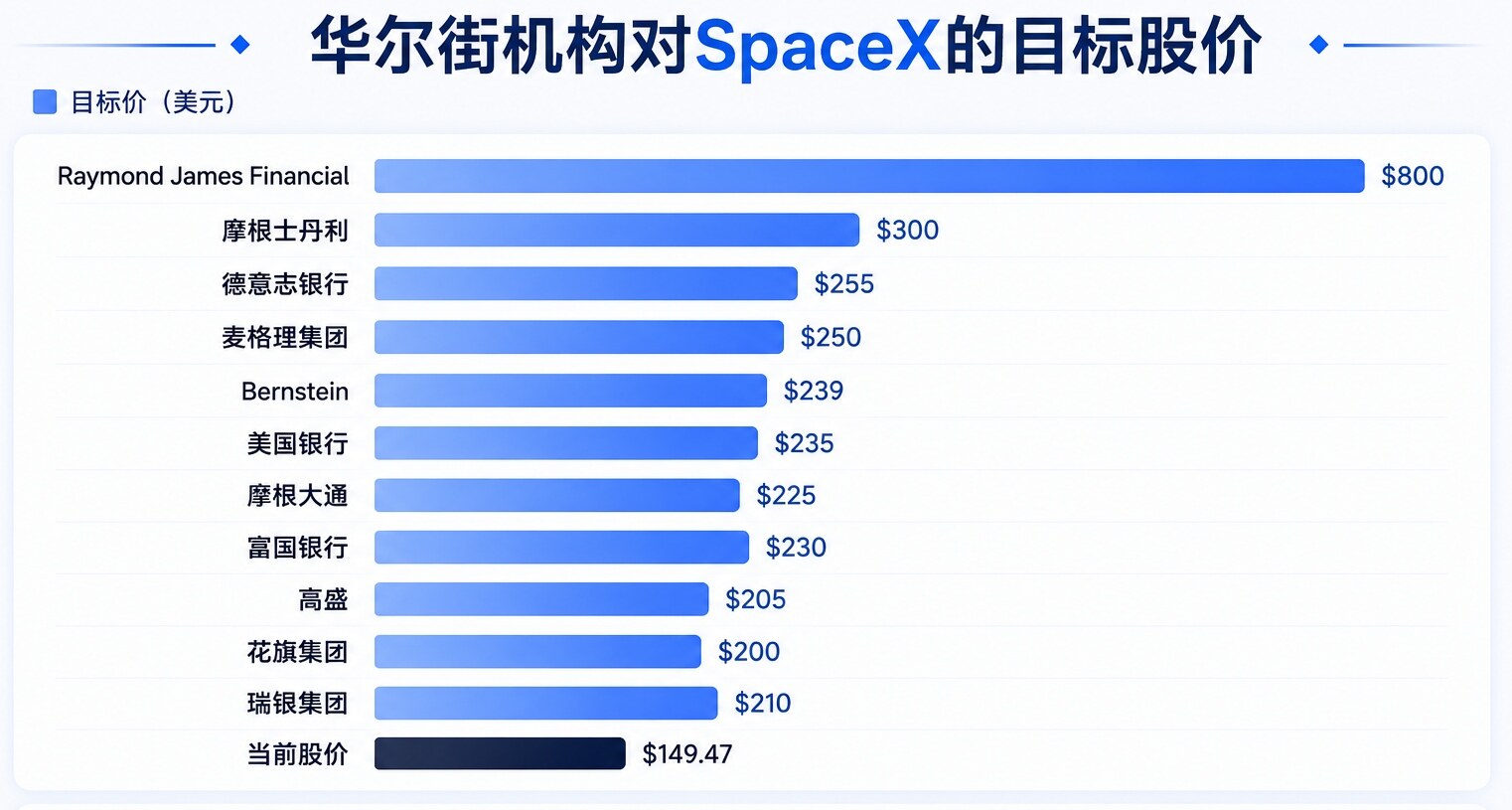

Obviously, neither time nor market sentiment is on the side of the bulls anymore. Over the past month, SPCX has tested the $150 support level multiple times, but previously, $150 support was on the offensive side; now it is purely on the defensive. However, bizarrely, after the end of the IPO quiet period, Wall Street institutional analysts have collectively given SPCX a Buy rating.

As IPO underwriters, both Goldman Sachs and Morgan Stanley gave SpaceX a Buy rating. Goldman Sachs analyst Eric Sheridan set a target price of $205, while Morgan Stanley analyst Adam Jonas gave a target price of $300. Additionally, Bank of America initiated coverage on SpaceX with a Buy rating and a target price of $235; Citigroup set a target price of $200 for SpaceX; Bernstein gave SpaceX an Outperform rating with a target price of $239; Macquarie Group set a target price of $250; Deutsche Bank set a target price of $255; JPMorgan set a target price of $225; UBS Group set a target price of $210; Wells Fargo set a target price of $230.

Raymond James Financial gave the most optimistic forecast, with analyst Brian Gesuale setting a target price for SPC as high as $800, believing SpaceX will become "one of the most iconic industrial infrastructure companies of the 21st century."

However, these institutional ratings primarily focus on SpaceX's long-term value, such as its positioning in rocket launches, Starlink, and AI space data centers. In the short term, especially before the August share unlocking wave arrives, what can SpaceX rely on to support its stock price from falling below $150 and heading straight for the $135 IPO price? The foreseeable potential positives are as follows:

First, relying on Trump's promotion. On July 7th, SpaceX President and COO Gwynne Shotwell and her husband announced participation in the Invest America plan, donating part of their SpaceX shares to over 2 million American children's "Trump Accounts," with an estimated donation of about 2 million SpaceX shares worth approximately $325 million. Trump had previously publicly urged Musk to donate SpaceX shares to the "Trump Account." Trump is a businessman who understands value exchange. After SpaceX stock enters the "Trump Account," he might promote SpaceX just as he promoted Micron and Dell.

Second, SpaceX's Starship flight test scheduled for July 14th. SpaceX's Starship's 13th flight test (Flight 13) is currently targeted for launch on July 14, 2026 (Tuesday), with a backup date of July 15th. The US Federal Aviation Administration (FAA) has issued an operational advisory confirming NET (No Earlier Than) July 14th. Rocket launches have always sparked public interest. As a world-leading aerospace company, each of SpaceX's launches garners global attention. If Flight 13 is completed successfully, SpaceX's aerospace narrative might once again briefly ignite "fan" enthusiasm, thereby boosting the stock price. Although the community and tracking sites generally consider July 14th as the primary launch target, it could be delayed by days or weeks due to technical readiness, weather, or other factors.

But ultimately, what investors most anticipate might be for Musk himself to do something to "rescue the market."