TL;DR

The South Korean stock market just experienced its sharpest drop this year.

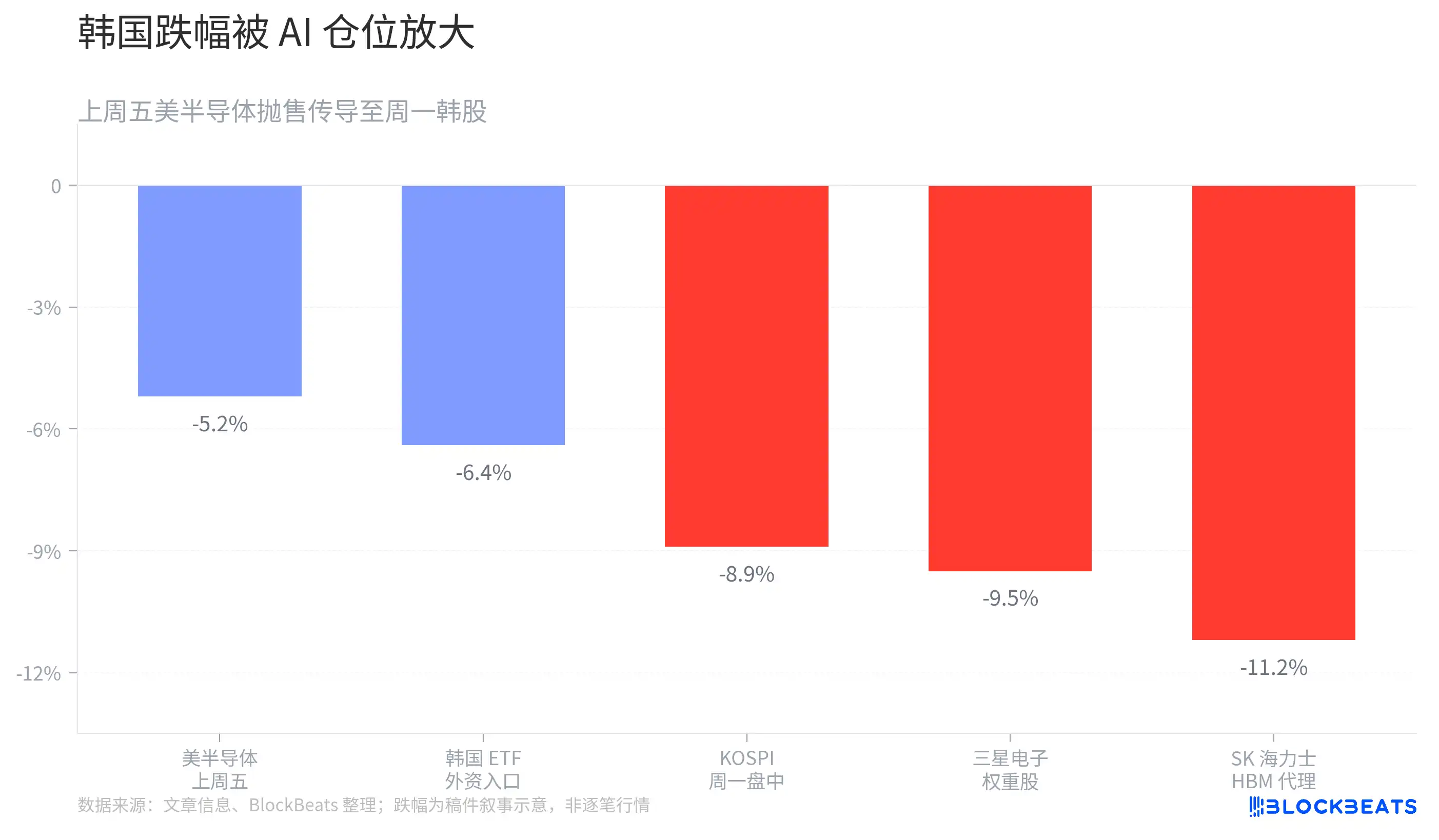

After opening on Monday, the KOSPI fell nearly 9% intraday, triggering a circuit breaker. Both Samsung Electronics and SK Hynix plunged heavily, and the market began discussing whether the AI bull market has reached an inflection point.

But while the market panicked and sold off, another event was unfolding in Seoul.

Jensen Huang began his visit to South Korea over the weekend, not only meeting with SK Group Chairman Chey Tae-won but also announcing a new multi-year cooperation agreement between NVIDIA and SK Hynix to jointly develop next-generation memory products for AI data centers. Simultaneously, he held intensive meetings with South Korean tech giants like Samsung Electronics, LG, and NAVER, reiterating that AI infrastructure construction is still in its early stages.

Thus, a rather contrasting picture emerged in the market.

On one side, South Korea's AI leaders faced concentrated selling pressure; on the other, the most core customer in the AI supply chain was moving to strengthen its ties with Korean suppliers.

If AI demand was truly collapsing, Jensen Huang wouldn't have needed to fly to Seoul specifically to reinforce cooperation.

This is also why a new debate is emerging in the market today.

Is the Korean market preemptively signaling the peak of the AI cycle, or is it experiencing a typical high-leverage deleveraging event?

South Korea Becomes One of the Most Sensitive Markets for Global AI Trading

Although this decline occurred in South Korea, the trigger did not originate there.

Last Friday, the U.S. semiconductor sector faced a sharp sell-off. The Philadelphia Semiconductor Index recorded one of its worst single-day declines in recent years, with AI infrastructure-related companies like Broadcom and Micron also correcting. Subsequently, the market began to reassess the risk exposure of high-valuation tech stocks.

South Korea became the most directly affected market.

Over the past year, the core driver of the South Korean stock market's rise has not been its domestic economy, but rather AI data center construction, HBM demand growth, and the expansion of the NVIDIA supply chain.

Samsung Electronics and SK Hynix together account for an extremely high weighting in the Korean market. When global funds want to bet on AI infrastructure, South Korea is one of the most convenient entry points; and when funds begin to reduce their AI exposure, South Korea naturally becomes one of the easiest markets to sell.

As a result, the decline in the Korean market far exceeded that in the U.S. market itself.

In a sense, South Korea is no longer just a national index, but more like a large AI memory ETF.

Jensen Huang's Visit to South Korea Presents a Stark Contrast to Market Panic

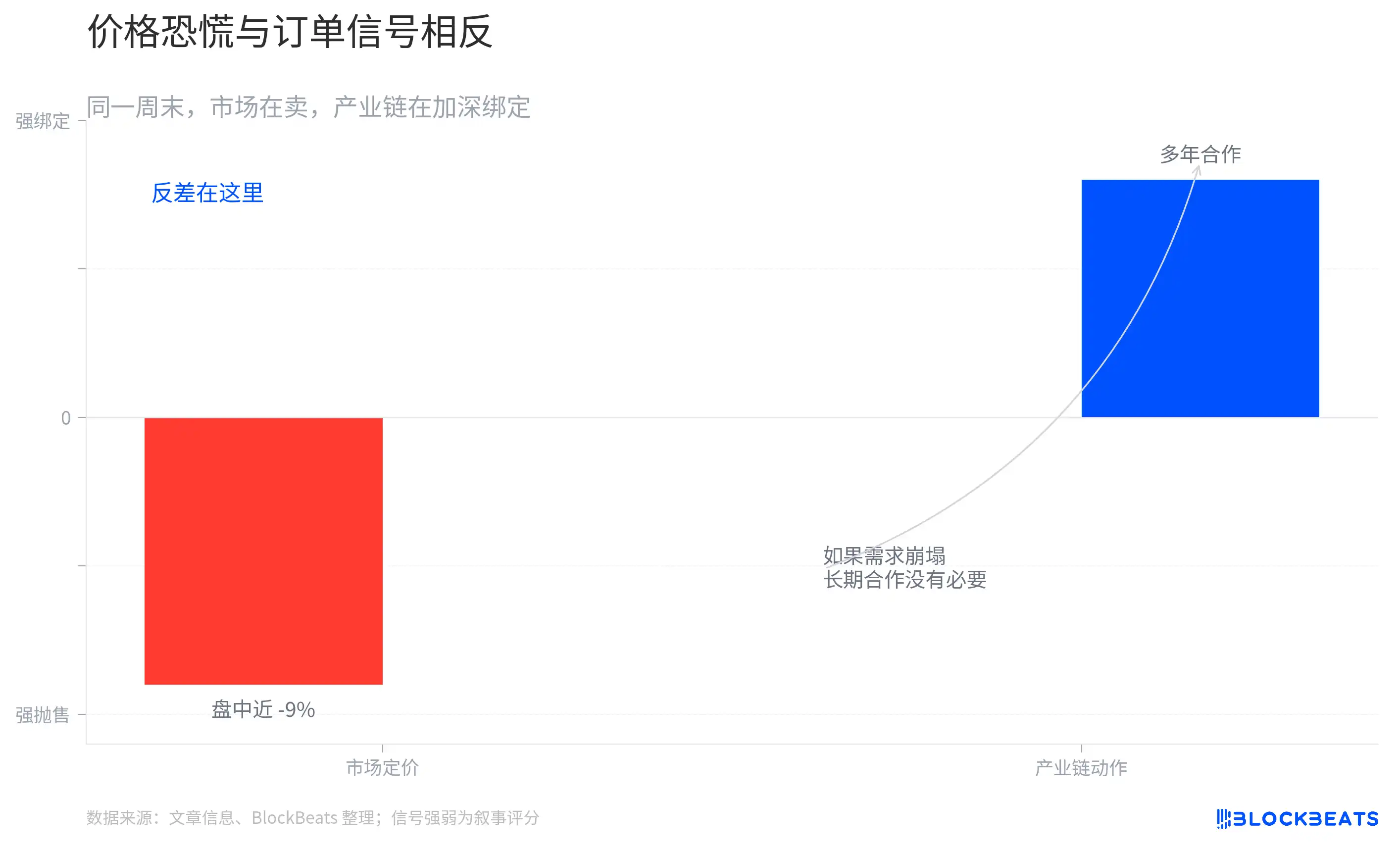

If market panic stems from valuations, then the biggest positive news over the weekend came from the supply chain itself.

The core objective of Jensen Huang's visit to South Korea was very clear: to further strengthen the cooperative relationship between NVIDIA and the Korean AI supply chain. The most notable development was the announcement of a new multi-year cooperation agreement between NVIDIA and SK Hynix. Over the past two years, HBM has become one of the most critical components in AI servers, and SK Hynix is one of the biggest beneficiaries of this trend.

This is also why the market highly anticipated this cooperation.

In recent months, as the scale of AI infrastructure construction continues to expand, the market began to worry about whether HBM demand growth would gradually peak. However, Jensen Huang's visit to South Korea at this time actually sends the opposite signal. If NVIDIA believed that AI data center construction was nearing its end, it wouldn't need to reinforce long-term cooperative relationships with suppliers at this point.

From a supply chain perspective, there is no evidence yet of a sudden disappearance of AI demand.

The most interesting part of the past two days lies right here. The capital market is using stock prices to express concerns about AI sector valuations, while the core enterprises in the supply chain are still discussing expansion and cooperation plans for the coming years. A significant temperature gap remains between the price signaled by the market and the signal released by the industry.

The AI Bull Market Begins Entering the Profit Pool Reassessment Stage

This is also the core of the current major divergence.

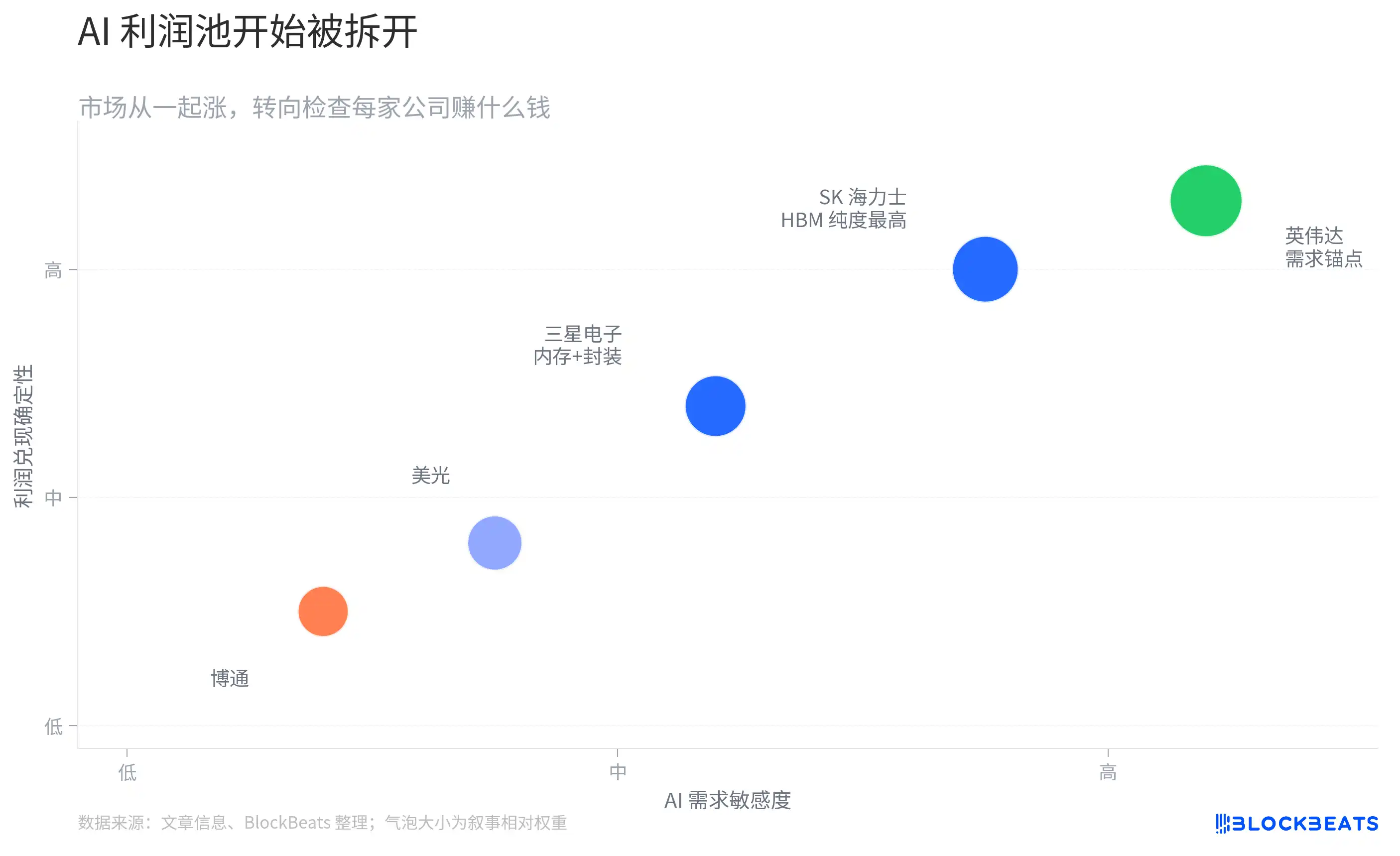

Over the past year, the market traded a very simple logic: AI demand growth. Therefore, NVIDIA rose, Micron rose, SK Hynix rose, Samsung Electronics rose—almost any company related to AI received a valuation boost.

But as the sector's gains continued to expand, the market has entered a second stage.

Investors are no longer satisfied with the story of 'AI will grow,' and have begun to ask another question: Who will ultimately capture the profits created by AI growth? In recent months, from the Rubin rack system memory adjustments, to the market reaction following Broadcom's earnings, to this Korean market crash, they all essentially reflect the same thing—the market is beginning to deconstruct the AI profit pool.

SK Hynix benefits from HBM, Samsung Electronics positions itself across HBM, DRAM, and advanced packaging, while Micron benefits more from the overall AI server memory upgrade. Although they all belong to the AI supply chain, their respective profit sources and pricing power are not the same.

Previously, the market was willing to collectively expand valuations for the entire sector. Now, capital is beginning to examine, one by one, whether these profits can truly be realized.

This is also why a supply chain update, an earnings guidance, or even a capital expenditure adjustment can trigger significant volatility across the entire sector. The focus of market trading has shifted: rather than whether AI will continue to grow, investors are more concerned about whose financial statements the growth will ultimately land on.

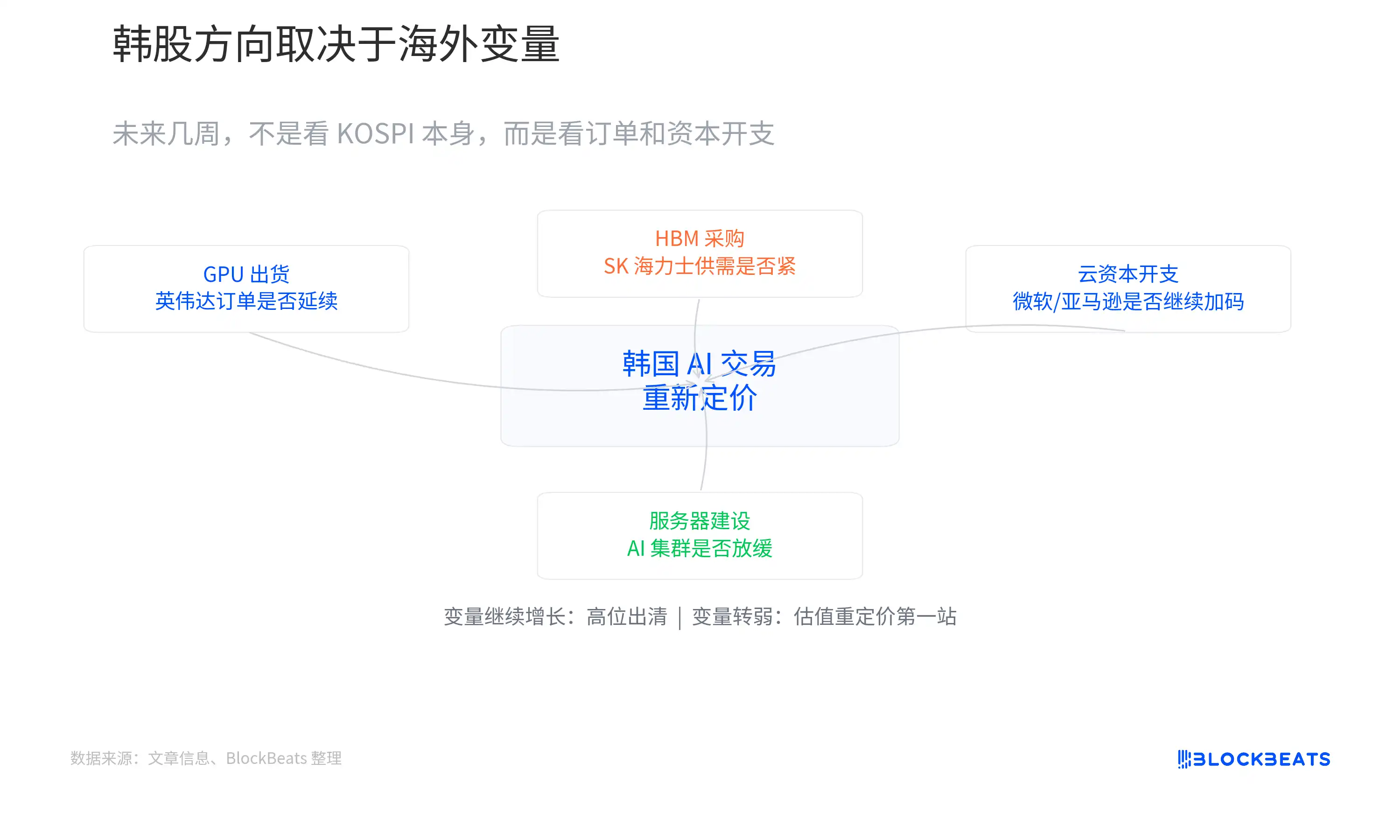

What Decides South Korean Stocks is Not South Korea

In the coming weeks, what will truly determine the direction of the South Korean market remains NVIDIA's orders, HBM supply and demand, and capital expenditures from cloud service providers.

If this data begins to weaken, then this crash may be just the beginning of a larger-scale valuation adjustment.

But if data center construction, GPU shipments, and HBM procurement continue to maintain high growth, then Monday's circuit breaker looks more like a concentrated liquidation of a crowded trade.

At least from the current vantage point, the price signaled by the market and the signal released by the industry are not entirely aligned.

On one side, South Korea's AI leaders are facing the most severe selling pressure in years; on the other, Jensen Huang is in Seoul discussing the next generation of AI infrastructure with supply chain partners.

Whose judgment is closer to reality? Perhaps we will have an answer soon.