Written by: Ponyo(@ponyo_fp), Four Pillars Researcher & Hyperliquid Core Contributor

Compiled by: AididiaoJP, Foresight News

In February, TradeXYZ launched perpetual futures contracts for Samsung Electronics, SK Hynix, Hyundai Motor, and EWY on Hyperliquid, allowing investors to gain exposure to South Korean stocks on weekends for the first time.

I reviewed the weekend price movements of these stock contracts since their launch, covering a total of 62 observation samples across the 4 assets. I compared each contract's movement from Friday close to Sunday close with the direction of the underlying asset's Monday opening auction. For South Korean stocks, I used the KRX opening price at 9:00 AM (KST); for EWY, I used the NYSE opening price at 9:30 AM (ET).

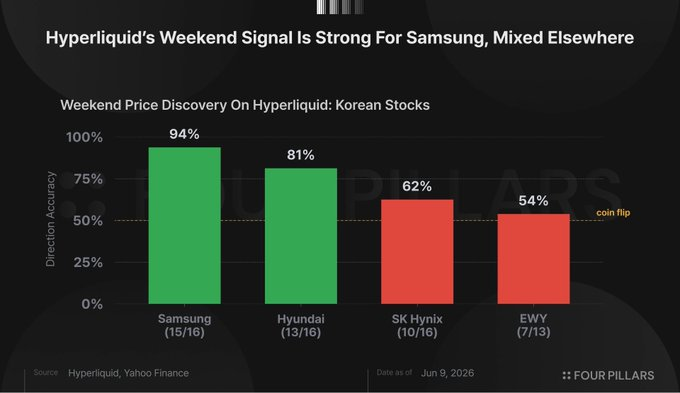

Hyperliquid correctly predicted the opening direction in 45 out of the 62 cases, an accuracy rate of 73.8%. This number sounds good, but the aggregate data masks highly uneven performance across different assets.

Samsung Electronics shows a clear outlier. Hyperliquid correctly predicted the direction 15 out of 16 weekends. Since Samsung's Monday openings were evenly distributed between up and down, there's no inherent directional bias inflating the hit rate. The binomial test (against a 50% benchmark) yields a p-value of 0.0003, meaning the probability of such a strong result occurring by random chance is only 0.03%. Although the sample size is still small, a result of 15 correct out of 16 is hard to ignore.

Hyundai Motor also performed well, with 13 correct predictions out of 16, an 81% accuracy rate. However, after accounting for the stock's slight downward bias on Mondays, this result did not reach statistical significance. During the sample period, Hyundai Motor opened lower on Mondays 62% of the time, meaning a simple strategy of always predicting "down" would have had a high baseline win rate.

SK Hynix is less convincing. It was correct only 10 out of 16 times, barely better than a coin flip. Some misses were significant. On the weekend of June 5-7, the Hyperliquid contract closed up 0.11%, while SK Hynix gapped down 10.34% at the Monday KRX open.

EWY had the worst results. It was correct only 7 out of 13 weekends, even underperforming the benchmark. Out of those 13 Mondays, EWY opened higher 10 times, accounting for 77%. A simple weekly prediction of "up" would have outperformed Hyperliquid's signal. Meanwhile, the Hyperliquid weekend contract closed down in 9 out of the 13 cases, repeatedly pointing traders in the wrong direction.

The discrepancy between Samsung Electronics and EWY can largely be explained by market time differences. The KRX opens at 9:00 KST, which is 00:00 UTC, almost exactly coinciding with Hyperliquid's daily candle reset time. Therefore, the time gap between Hyperliquid's last weekend trade and the KRX opening auction is only a few minutes.

In contrast, EWY trading on the NYSE doesn't start until 9:30 AM ET, about 14 hours after Hyperliquid's Sunday candle close. By then, the entire Monday trading session on the KRX is complete, European markets are open, and US pre-market trading has incorporated a new round of information. The information set determining EWY's Monday open simply didn't exist when Hyperliquid's weekend candle closed.

A reasonable critique is that even Samsung's results might reflect last-moment convergence rather than genuine price discovery. Informed traders might adjust positions on Hyperliquid just before the KRX opens, making this "prediction" almost tautological.

To test this, I repeated the analysis using Saturday's close instead of Sunday's, creating a lead time of about 24 hours instead of just minutes. The results show that the Saturday signal still predicted Samsung's Monday opening direction with 75% accuracy (against a 50% benchmark). Sunday trading improved the result but didn't create the signal from scratch.

In comparison, Samsung's own Friday price movement predicted Monday's direction with only 62% accuracy. This suggests Hyperliquid's weekend market provides information beyond a simple continuation of the previous KRX trading session.

Among the four assets tested, only Samsung Electronics produced a statistically significant directional signal. The sample size remains small, and the results have not been validated out-of-sample. Nevertheless, this might still be valuable information for anyone trading Samsung Electronics or the broader KOSPI market.

Despite an average weekend trading volume of only about $12,000, Hyperliquid correctly predicted the Monday opening direction for a company with a market cap of roughly $300 billion with 94% accuracy and a p-value below 0.001. For anyone trading Samsung Electronics on the KRX, checking Hyperliquid's weekend closing price before Monday's opening auction appears to be a very worthwhile practice.