Circle’s stock, CRCL, dumped 17.5% to $62.63 on the 30th of June, marking the largest daily loss since March. It’s worth noting that in March, the stock fell 20% following a draft proposal to ban stablecoin yield on idle balance.

This raised concerns about likely limited USDC adoption and the potential impact on the second-largest stablecoin issuer’s revenue outlook if the proposal were enacted. The dip on the 30th of June, however, was driven by a new rival in the stablecoin space.

Will Open USD challenge Circle, Tether’s dominance?

A consortium of 140 firms, including traditional cross-border payment players such as Visa, Mastercard, BlackRock and Google, launched a new stablecoin, Open USD (OUSD). According to the coalition, reserve earnings will be shared among partners, with zero transfer fees.

The target for OUSD? Enterprise treasury management and merchant payments. While not entirely focused on retail, the two segments are also eyed by both Tether’s USDT and Circle’s USDC.

The new stablecoin will be offered later in the year, and Circle’s stock reaction suggested the market share dominance could be challenged. In fact, Matthew Sigel, head of digital research at asset manager VanEck, echoed this stance as the stock dumped on Tuesday.

$CRCL -13% as Stripe, Coinbase and BlackRock back rival stablecoin ‘Open USD’

Sam Ruskin, an investment associate at crypto-focused venture firm Reciprocal Ventures, also reinforced Sigel’s outlook. He added,

This will either force Circle to continue their revenue share agreements, find new distributors for USDC (although nearly everyone interested in stablecoins today is backing OUSD). Whatever way you cut it, this seems bearish for Circle.

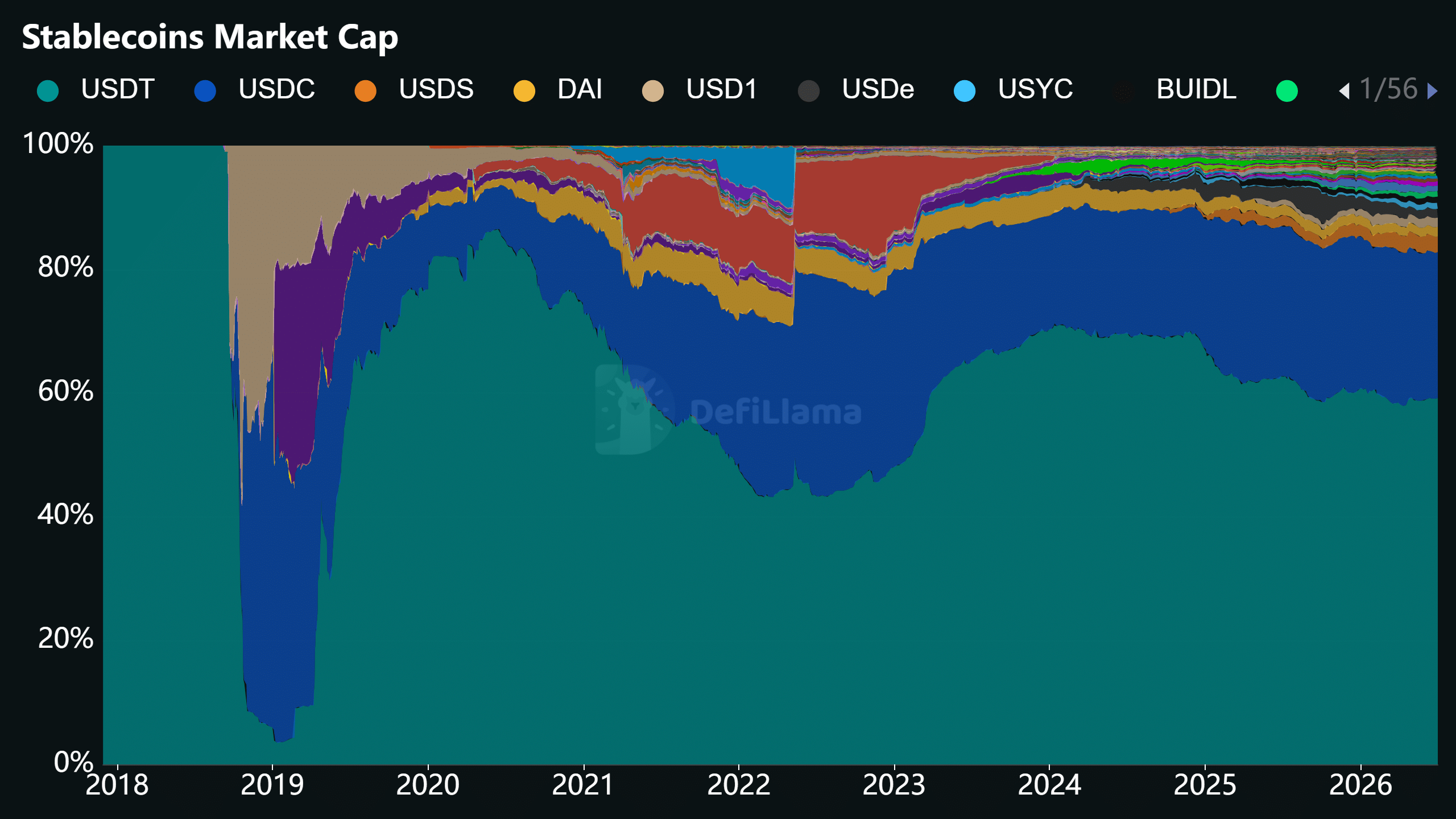

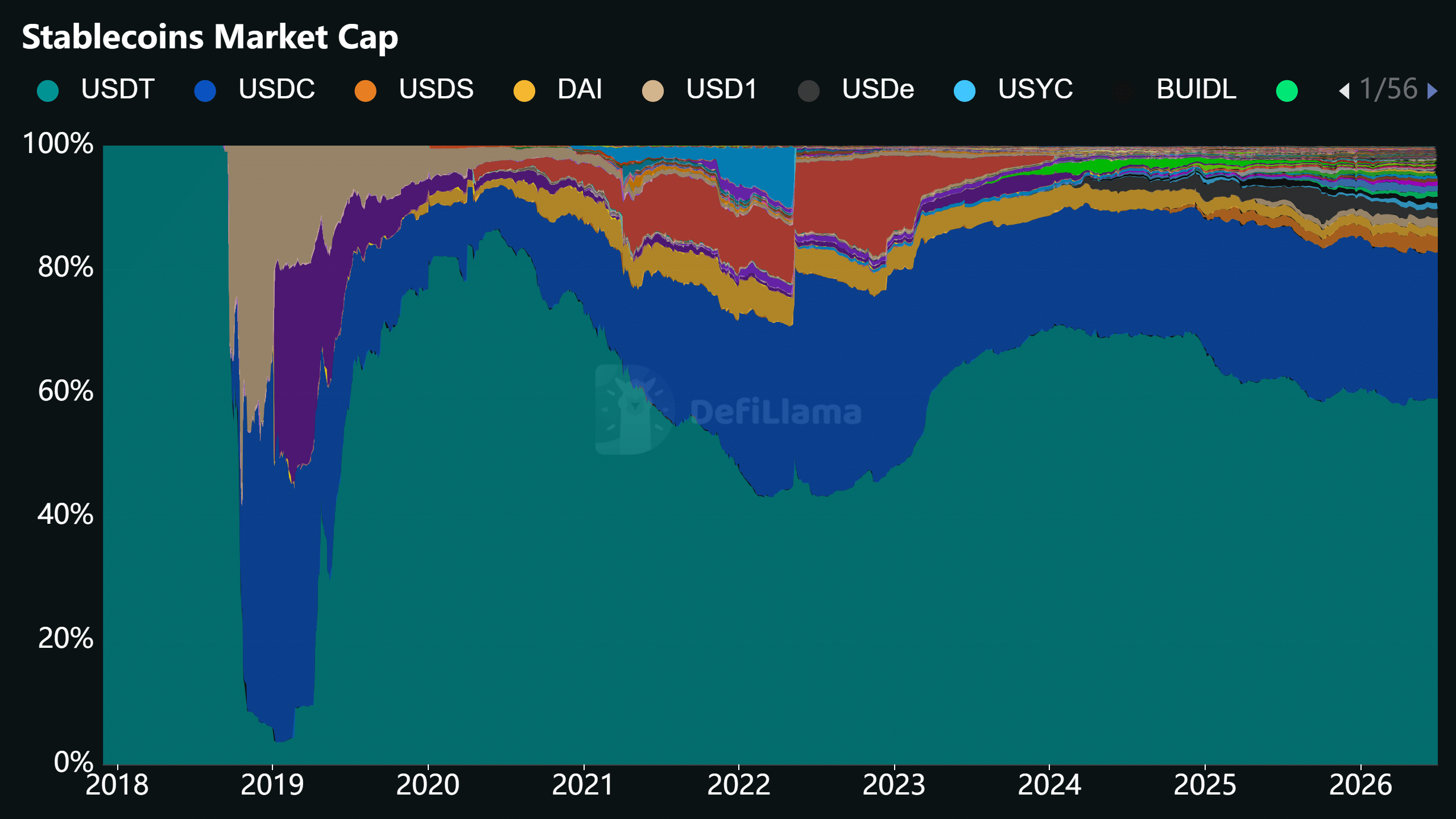

There has been increased competition in the stablecoin market after the GENIUS Act passage in 2025. In fact, over the same period, Tether’s USDT still holds dominance, but its market share shrank from 62% to 59%.

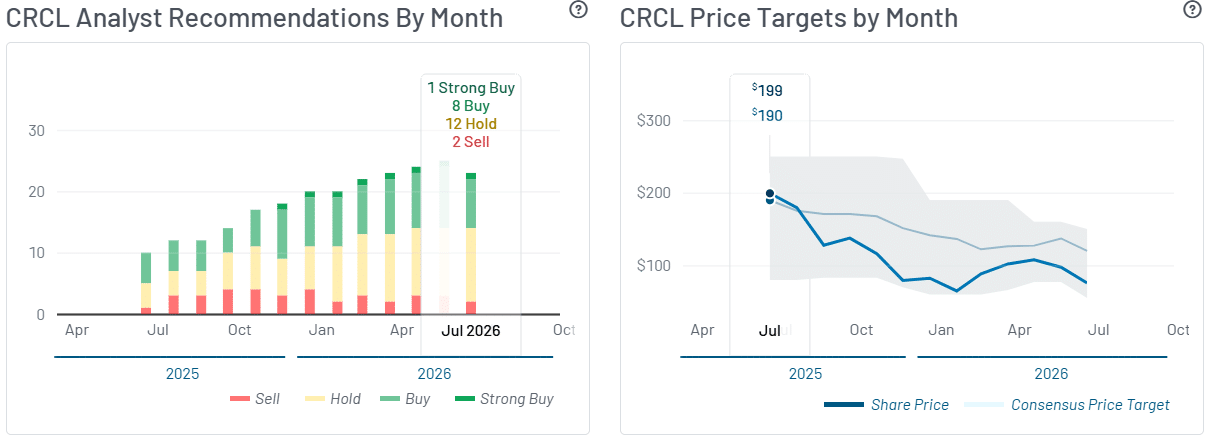

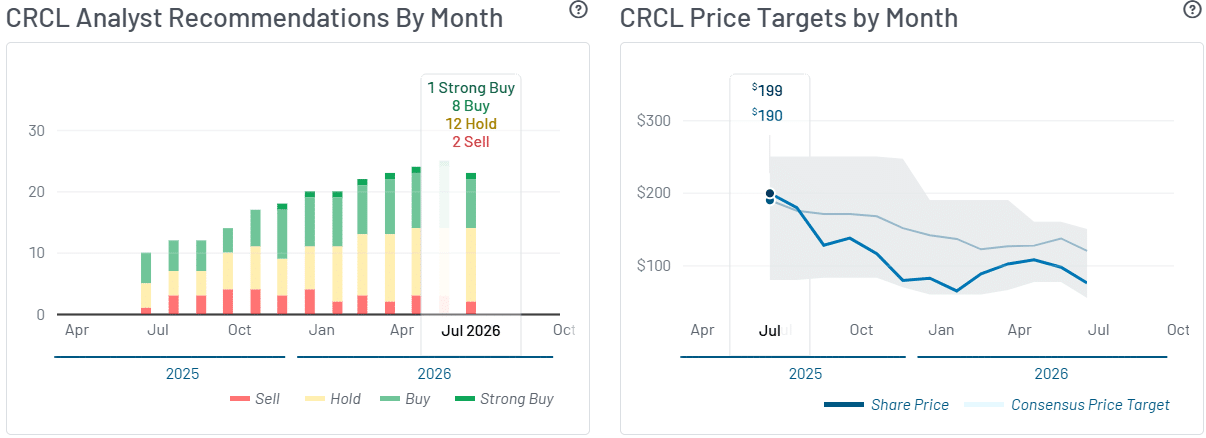

On the other hand, Circle’s market share rose from 19% to 25% before easing slightly to 24% in 2026. Whether new competitors will erode that share remains uncertain. Even so, analysts remain bullish on the stock, with a consensus price target of $120, implying roughly 91% upside from current levels.

Final Summary

- Circle stock, CRCL, saw a massive loss of 17.5% on Tuesday

- The bearish move followed a new rival, Open USD, backed by Visa and 140 other partners.