Author: Tiger Research

Compiled by: AididiaoJP, Foresight News

The U.S. Securities and Exchange Commission (SEC) is preparing to formally announce an "innovation exemption" framework this week, which will allow third parties to tokenize U.S. stocks like Apple and Tesla without approval from the listed companies. This move could accelerate the migration of traditional stock markets to blockchain, while also raising deep concerns among exchanges about liquidity fragmentation and revenue loss.

According to a Bloomberg report on May 18, this framework originates from the deregulation vision proposed by pro-crypto commissioners Paul Atkins and Hester Peirce in February. Coinbase and the Blockchain Association had previously submitted formal letters of support, strongly advocating for granting third parties the right to tokenize. However, the guidance issued by Peirce on May 22 is narrower in scope than market expectations, applying only to on-chain stock instruments that fully retain shareholder rights and explicitly excluding synthetic stock tokens that do not carry voting or dividend rights.

Two Core Threats: Liquidity Fragmentation and Revenue Fragmentation

The core impact of tokenized stocks lies in "fragmentation." While the crypto industry often discusses liquidity aggregation, the traditional finance world views it as a structural threat.

- Liquidity Fragmentation: When the same stock is tokenized on different blockchains and decentralized platforms, the trading volume and order flow originally concentrated on the NYSE or Nasdaq will disperse across multiple venues. This will lead to price disparities between platforms, increased slippage for large orders, and reduced overall market efficiency.

- Revenue Fragmentation: With the dispersion of trading venues, transaction fees and intermediary revenues that originally belonged to domestic exchanges will flow to overseas or competing platforms, directly impacting national financial competitiveness.

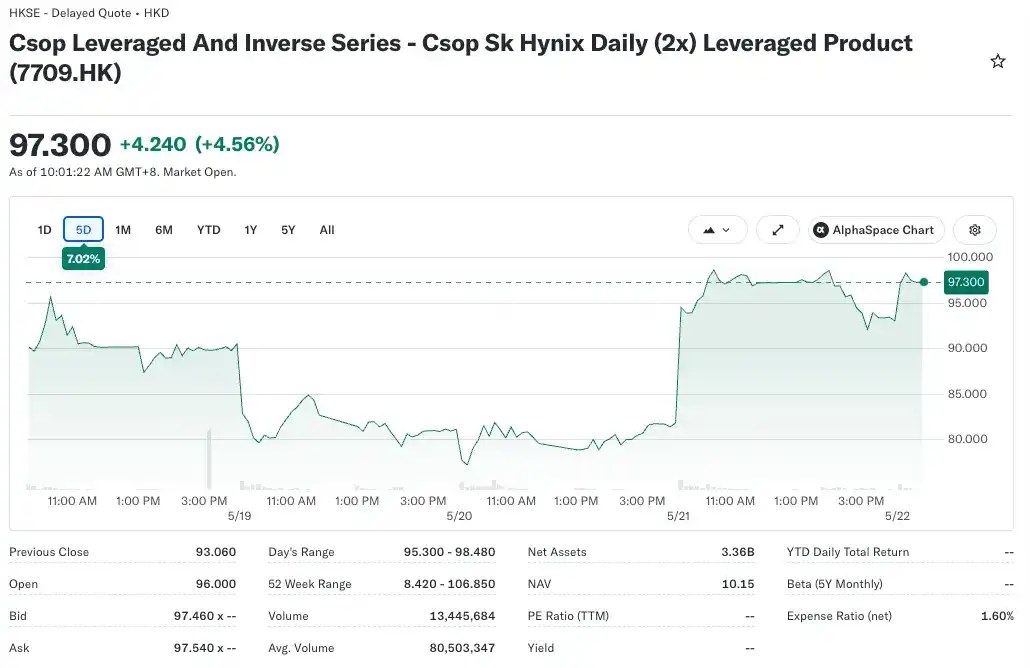

A Tiger Research report uses South Korea as an example: The SK Hynix 2x Leveraged ETF launched by Hong Kong asset manager CSOP has grown into the world's largest single-stock leveraged ETF, with assets exceeding 110 billion won (approximately $80 billion). If South Korea could have taken the lead in launching similar products through regulatory sandboxes, these management fees and financial revenues could have stayed within the country.

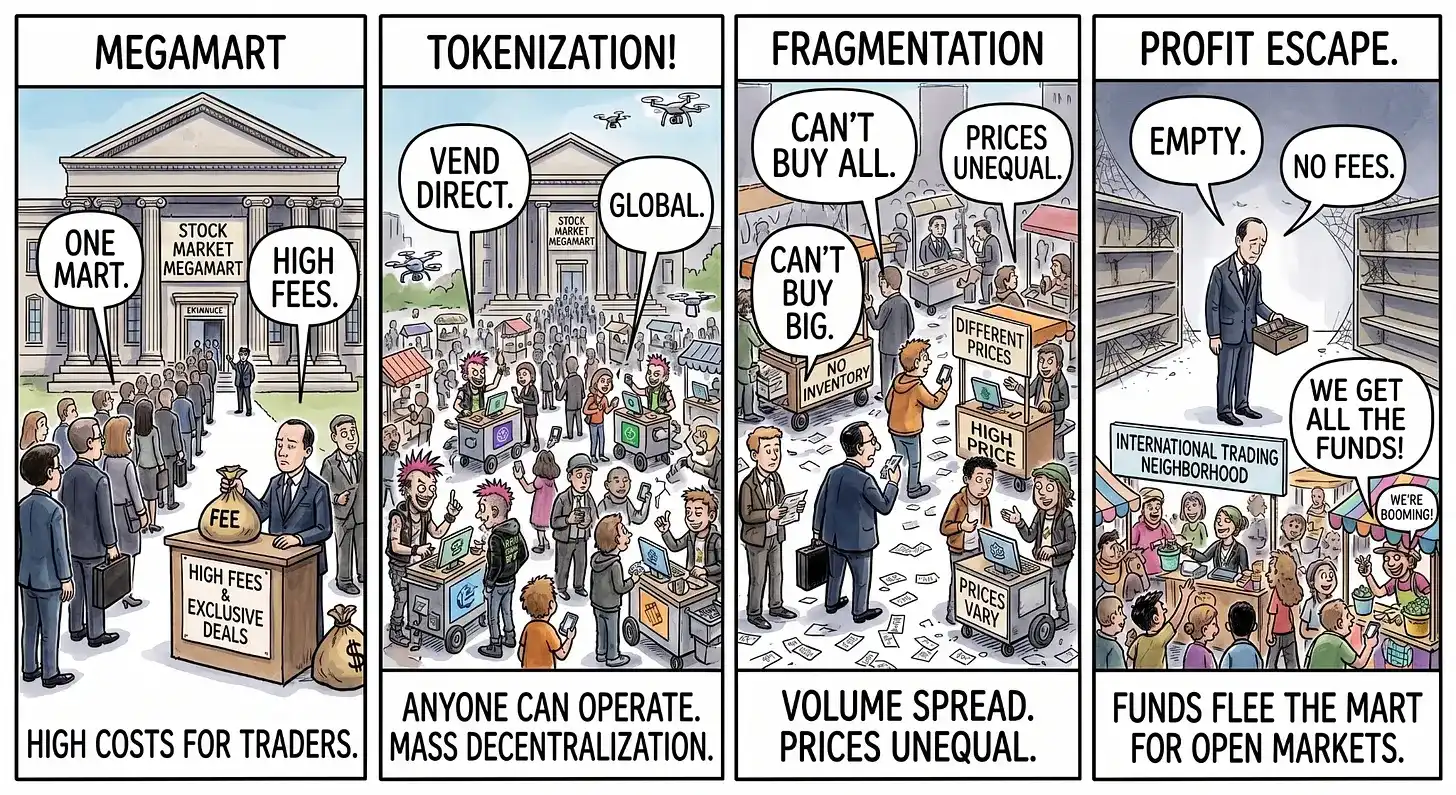

The End of Traditional Exchanges' "Supermarket" Monopoly

The report uses a vivid metaphor to describe this change: the traditional stock market is like a dominant supermarket where all buyers and sellers are concentrated, and the exchange monopolizes transactions and collects fees. Tokenized stocks are akin to allowing anyone to set up thousands of street stalls without permission, conducting trades directly outside the supermarket.

This dispersion will lead to buyer loss, thinner inventory at each stall, difficulty in executing large trades, and the slicing up of revenue sources. If domestic exchanges hesitate due to regulatory constraints, competing platforms in other jurisdictions will rush to seize global capital flows and intermediary revenues.

Capital Fragmentation Is Already Happening

On the same day the SEC signaled the framework (May 18), the open interest for RWAs (Real World Assets) on the decentralized platform Hyperliquid surpassed $2.6 billion, reaching a record high. Driven by the demand for 24/7 on-chain trading of traditional assets, RWA trading volume on perpetual DEXs is expected to surge further.

Traditional financial institutions and regulators face a dilemma: one option is to proactively build tokenization infrastructure through cooperation, like the NYSE; the other is to lobby regulators to block innovation to protect existing revenues. Regulators are also conflicted—they must control the pace of innovation while preventing domestic revenue from being siphoned off by overseas platforms.

Even if the framework is formally announced, potential conflicts are just beginning. Future focal points will include:

- A second "clarity war" surrounding shareholder rights;

- How to bring platforms like Hyperliquid, which have grown in regulatory gray areas, into the regulatory system. If deemed unlicensed exchanges, this could trigger a new wave of liquidity and uncertainty shocks.

In the era of digital assets, if financial institutions and jurisdictions do not act quickly, they will permanently lose their long-monopolized fee rights and financial leadership, and capital will continue to disperse in all directions.