Author: Nic Carter

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: A U.S. Special Forces soldier made $400,000 on Polymarket using classified information, and this is just the latest scandal. Nic Carter points out that prediction markets are stuck in a vicious cycle: they rely on insider trading to generate accurate prices, but this makes retail investors feel the market is manipulated and leave. This contradiction determines whether prediction markets can survive in the long term.

As I wrote in February of this year, prediction markets have a serious insider trading problem, and this is no accident. This leads to a major failure mode:

The social value of prediction markets comes from using monetary incentives to get insiders to leak confidential information, but this destroys retail investor confidence in the market over time.

Two days ago, the biggest scandal to date broke. The U.S. Department of Justice charged Special Forces Sergeant Major Gannon Ken Van Dyke with improper trading using classified information. Before the Maduro raid mission, he made $400,000 on Polymarket. He was not an ordinary soldier but a senior Green Beret member responsible for special operations planning and execution.

To be clear, although many people are calling for leniency for him because (legal) insider trading is widespread among members of Congress, he should still go to jail. His actions potentially leaked raid information to Venezuelans through trading activities, which is morally and legally problematic. Although the Venezuelans don't seem to have noticed, the government cannot set a precedent where elite operatives leak details of upcoming operations through market activities for personal gain. I sympathize with Van Dyke, but he did break the law and the confidentiality he swore to uphold.

This is just the latest in a series of real or suspected insider trading scandals on prediction markets. Previously, Israel arrested two reservists for using military intelligence to trade on Polymarket. Markets concerning the start time of the Iran war, ceasefire agreements, the killing of Khamenei, and Biden's pardon order have also been under suspicion, but no arrests have been made yet. Kalshi and Polymarket have also flagged and suspended accounts trading in markets where they had a vested interest, such as three congressional candidates betting on their own election markets.

You might think that as more people realize that trading with confidential information is illegal not only in securities markets but also in prediction markets, these problems would disappear. But I think the issue is deeper.

The premise of prediction markets is that they are informationally efficient because they reward informed insiders.

In other words, prediction markets are "good" because they aggregate a large number of uninformed retail investors, who create economic incentives for insiders to reveal private information. (This concept—that retail investors create incentives for informed insiders to participate—is well-documented in financial literature, and a recent paper further extends it to prediction markets.) Prediction markets can then reliably promote themselves as having social utility because they indeed provide better, more timely signals than other platforms (experts, polls, etc.). Kalshi and Polymarket both know this but are reluctant to explicitly admit it. But they do hint at it in their marketing!

Kalshi's CEO Tarek Mansour explicitly stated on the Sourcery podcast that "There is no such thing as insider trading in commodity markets. It's all insider trading actually," which is... an extremely creative interpretation of the law. He added:

I think there is a subset of non-public information that (traders) cannot trade on, but I think we are restricting it a bit too much right now.

Kalshi has used slogans like "Trade Anything" and "Everyone is an Expert at Something," both of which imply that ordinary people can monetize any privileged information they happen to have on the platform.

Polymarket's CEO Shayne Coplan had this exchange with CBS last year:

Anderson Cooper: But prediction markets do rely on some people having inside information.

Shayne Coplan: Mhmm. Yes. I think it's a good thing that people have an edge in the market. Obviously, you need to manage them, need to be very clear and strict about drawing the lines, like on the ethics side, we spend a lot of time on that. But it's somewhat inevitable, and there's a lot of good that comes from it. You know, people will adapt.

Shayne has also said that prediction markets are "the most accurate thing that we have as humans right now, until someone creates some sort of super crystal ball." Some of that accuracy comes from insiders.

Robinhood's CEO Vlad Tenev (partnering with Kalshi) said:

Prediction markets actually allow you to get news faster, in some cases even before it happens. I think it does have tremendous economic value.

Economist Robin Hanson, considered by many to be the godfather of prediction markets, directly accepts this view and has written extensive defenses of insider trading in prediction markets. In 2024 he said:

If the purpose of the (prediction) market is to get accurate information in the price, then you definitely want to allow insiders to trade, even if that makes other people less willing to bet because they think it's unfair, because it makes the price more accurate. That's the priority.

I must point out that both Kalshi and Polymarket have anti-insider trading policies. Kalshi is regulated by the CFTC and has been explicit about prohibiting trading based on Material Non-Public Information (MNPI) and conducts market surveillance. When I wrote my last blog in February, I noted that Polymarket did not explicitly sanction insider trading, but in March they updated their rulebook, adding detailed prohibitions against trading of the following types:

- Trading based on stolen confidential information (if you are a soldier, the battle plan does not belong to you, it belongs to the government)

- Trading based on information illegally passed to you by an insider

- Trading on any contract where you can influence the outcome

The point of this section is not to blame Kalshi or Polymarket or their leadership for implying that traders have an informational advantage. I think their policies (updated in March 2026) are clear enough. Instead, I want to point out the fundamental contradiction plaguing these markets:

Prediction markets rely on informed traders to generate accurate prices, but they also rely on uninformed traders to create the economic incentive to attract informed order flow. This creates a tension:

- If they are too permissive towards insider trading, uninformed traders may exit due to a perceived lack of fairness

- If they are too restrictive towards insider trading, the markets may exclude their most valuable source of information

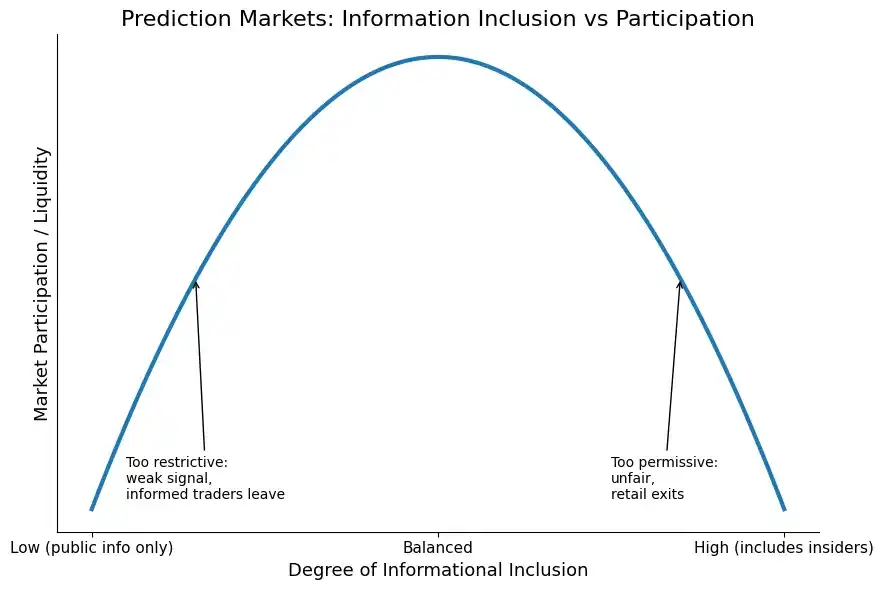

Thus, there is a trade-off between informational efficiency and perceived fairness. Here is a visual version of the same idea:

Chart: The Trade-off Curve Between Informational Efficiency and Perceived Fairness

So we end up with a few different failure modes:

Too Many Sharks, They Eat All the Fish

Insider trading standards are too loose, the market becomes very informationally efficient, but retail investors clearly feel the market is "rigged," that they are always betting against insiders. Therefore, retail leaves, and market liquidity decreases. This is the failure mode I talked about before. This is where we are now, but I think we will rebound in the other direction.

No Sharks, No Edge

This is the other end of the spectrum. Insider trading is strictly policed on the platform, with real-time market surveillance and strong regulatory reporting, so informed order flow stays away. The markets thus produce less socially valuable information, becoming mere sentiment aggregators rather than generating "news before the news." Therefore, the platform cannot market itself effectively.

The existential question is whether there is a golden mean: where liquidity is maximized, retail feels the market is "fair enough," and informed order flow is still compensated for its information gathering. The chart suggests it might exist, but reality is messier.

My prediction from February still holds. As I said then:

A serious risk remains that insider trading scandals will make retail traders feel the market is manipulated, causing them to abandon the platform. I predict a string of insider trading events this year that will convince platforms to significantly strengthen market surveillance and lead Polymarket in particular to move away from anonymous modes.

I expect Polymarket will remove the ability to trade without KYC entirely (this is currently the case for the non-US platform) and strengthen the flagging of suspicious trading on the platform. There will be a slew of criminal cases regarding stolen insider information, but the temptation will remain. While platforms won't admit it, there is a "socially optimal" amount of insider trading. But can they calibrate it optimally? Will regulators allow them to?

It's worth noting that not all informed traders are insiders. You can become informed by collecting public information and trading on it. But a subset of informed traders are indeed insiders misappropriating information.