Editor's Note: This article argues that what truly drives oil prices is not just whether the conflict ends, but "when the tipping point is crossed".

In the Iran conflict, now in its fourth week, the oil market is experiencing a classic case of "time-based pricing." The release of strategic reserves has delayed the impact but cannot eliminate the supply gap; disruptions in tanker transport and lagging production recovery are causing inventory pressures to accumulate into the future. Once the key node in mid-April is passed, the pricing mechanism will shift from "buffered volatility" to "re-pricing dominated by the gap."

More notably, the structure of the game itself is changing. The conflict no longer follows an "escalate to de-escalate" path but has turned into an endurance test against the market's tipping point. Whoever can hold out until the supply-demand imbalance is priced in by the market gains the initiative in negotiations. This means that even if the conflict ends shortly, oil prices will struggle to return to their previous range. The supply losses occurring now are reshaping the global oil balance for the foreseeable future.

The original text follows:

In this article, I will break down the possible scenarios. With the Iran conflict now in its fourth week, how will this situation affect the oil market?

On March 9, we published a public article titled "My Latest Assessment of the Oil and Gas Market Under the Iran Conflict," which stated:

Below is the impact on oil prices under different scenarios ("barrels lost" already includes the time required for production recovery):

Scenario 1: Tanker transport resumes the next day

→ Brent crude annual average will be in the high $70s to low $80s range (approx. 210 million barrels lost)

Scenario 2: Tanker transport resumes by March 15

→ Brent annual average will be in the mid-to-high $80s (approx. 290 million barrels lost)

Scenario 3: Tanker transport resumes by March 22

→ Brent annual average will be in the low $90s (approx. 370 million barrels lost)

Scenario 4: Tanker transport resumes by March 29

→ Brent annual average will be in the mid-to-high $90s (approx. 450 million barrels lost)

If tanker transport cannot return to normal by March 29, the situation the oil market will face is almost unthinkable. The only way out would be forced demand contraction, pushing prices to extreme levels.

Shortly after the report was published, the International Energy Agency (IEA) announced a coordinated release of a total of 400 million barrels from global strategic petroleum reserves (SPR). This will somewhat mitigate the impact of the supply loss. But as we pointed out in a subsequent article, "IEA's Coordinated SPR Release is the Biggest Gift for the Bulls":

From a trading perspective, traders are in no rush to push oil prices higher until this "cushion" is depleted. The concentrated SPR release does ease short-term supply anxiety, but it is only a temporary solution. The market will remain tense; as long as tanker transport remains disrupted, oil prices will gradually rise.

On the other hand, if the situation eases quickly—for example, with an immediate ceasefire or agreement—oil prices will fall rapidly. For instance, if a peace deal is reached before March 15, global inventories would see an net increase of 110 million barrels (400 million released - 290 million lost).

This could push Brent prices back down to the mid-$70s range.

Conversely, without a peace deal and with the supply disruption lasting until the end of March, global inventories would see a net reduction of 50 million barrels, and the gap would widen by about 80 million barrels for each additional week.

Therefore, the SPR's role is merely to "buy time" and does not solve the core problem. Tanker transport must return to normal. However, it does prevent a catastrophic price spike in the short term, thereby avoiding a large-scale demand collapse.

Fast forward to now, we have entered the "March 29 scenario" set at the beginning of the month. Next, we assess the oil market's direction based on the latest facts.

Facts

Total production shutdowns from Saudi Arabia, UAE, Kuwait, Iraq, and Bahrain have reached 10.98 million barrels per day:

Iraq: -3.6 million bpd

Kuwait: -2.35 million bpd

UAE: -1.8 million bpd

Saudi Arabia: -3.05 million bpd

Bahrain: -0.18 million bpd

Saudi Arabia has maxed out the capacity of its East-West pipeline, currently exporting about 4 million bpd via the Red Sea. The UAE is also using bypass transport via the Abu Dhabi pipeline (Habshan-Fujairah), whose capacity of about 1.8 million bpd is also at its limit. Tanker traffic through the Strait of Hormuz remains completely interrupted. In fact, even if the war ended tomorrow, it would take months to restore production and rebuild normal transport.

Scenario Projections

I will outline three possible paths:

1) The war ends this week, transport resumes by the weekend

2) The war ends in mid-April

3) The war ends at the end of April

It is important to note that the release of 400 million barrels of SPR, compared to our initial assessment on March 9, has bought the market more time. The oil price scenarios below already reflect this change.

Scenario 1: Ends this week

Impact on global inventory: -50 million barrels (SPR already factored in)

Impact on Brent: Short-term pullback to low $80s, annual average in the mid-to-high $80s

Scenario 2: Ends in mid-April

Impact on global inventory: -210 million barrels

Impact on Brent: Short-term pullback to low $90s, annual average in the mid-to-high $90s

Scenario 3: Ends at the end of April

Impact on global inventory: -370 million barrels

Impact on Brent: Short-term spike to the $110 range, annual average at $110–$120

Key Inflection Point: Mid-April

For the oil market, there is a clear "tipping point." The current market consensus expects the conflict to end before mid-April, and this expectation is crucial for oil price pricing.

Oil prices are a product of "marginal pricing." As long as the market believes supply is "just about sufficient," panic will not ensue. This is precisely the current state of the oil market—a lack of panic.

Policy statements from the Trump administration, the relaxation of sanctions on Iranian and Russian crude, and the SPR release have collectively suppressed oil prices.

But once this tipping point is crossed, these factors will become ineffective.

Currently, the evaporation effect of global "oil in transit" has not yet fully transmitted to onshore inventories. But our judgment is that by mid-April, this impact will become fully evident.

If the conflict remains unresolved by mid-April, the International Energy Agency (IEA) will have to coordinate another release of approximately 400 million barrels of strategic petroleum reserves (SPR). Otherwise, oil prices will surge into the "demand destruction" range ($200+).

Long-Term Impact

In Energy Aspect's latest weekly report, their estimate of the market's cumulative supply loss is about 930 million barrels. Among this, the cumulative production loss from May to December is about 340 million barrels.

This assessment is significantly more aggressive than ours. In our inventory sensitivity analysis, we did not fully account for the reality that countries like Iraq and Kuwait might need 3 to 4 months to restore production capacity. This means our previous estimates might have been too conservative.

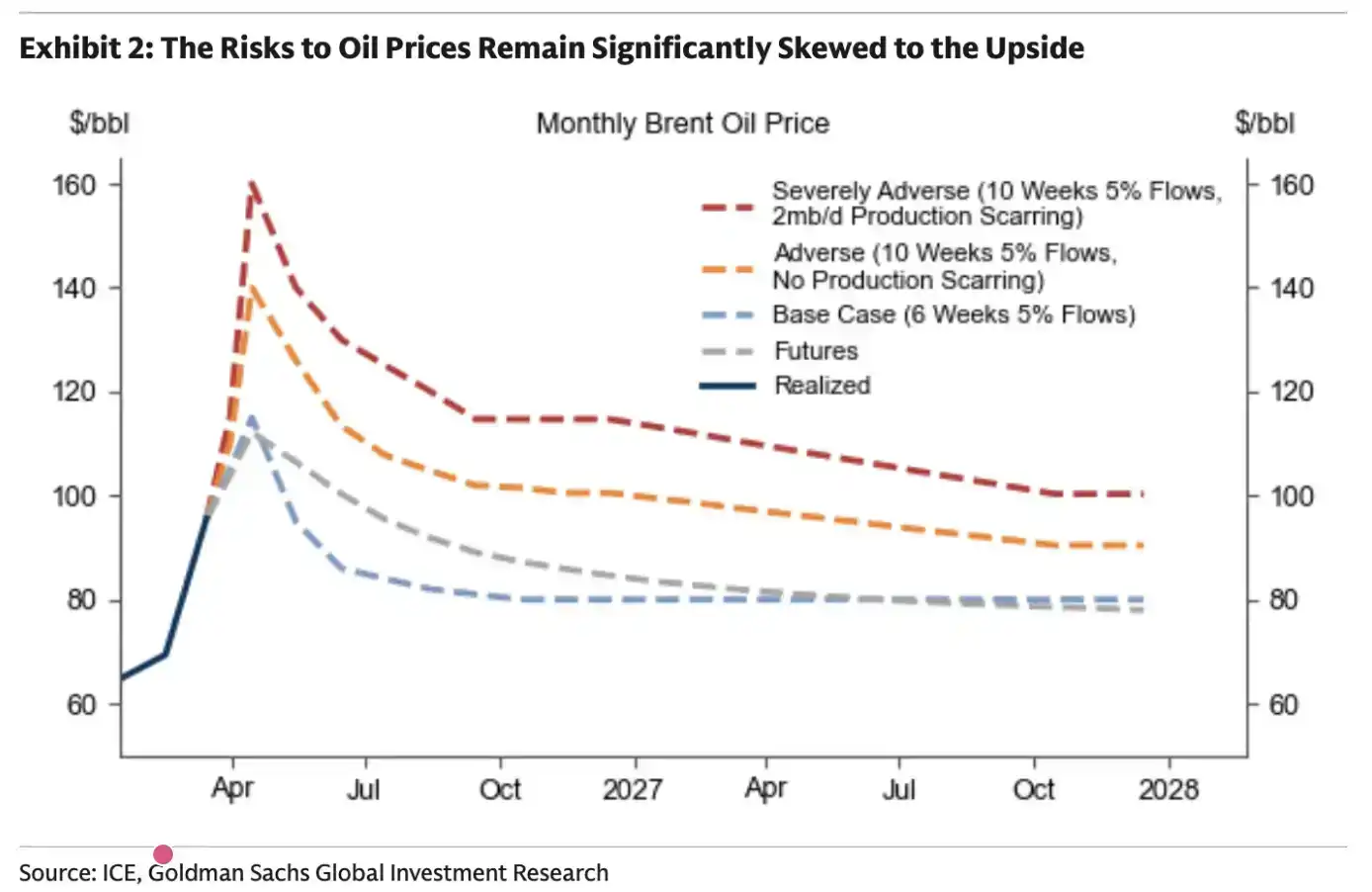

For Goldman Sachs, the conclusion is straightforward: the longer the conflict lasts, the longer high oil prices will persist.

Under the above scenarios, Goldman Sachs also provided a hypothesis: what the market would look like if the conflict lasted another 10 weeks. Their judgment is largely consistent with our earlier projections.

In essence, the oil market has a "tipping point." Once this line is crossed, there is no turning back.

Readers should be prepared for expectations: future oil prices will be structurally higher. Even if the war ends this week, the supply losses that have already occurred will have a substantive impact on the future global oil supply-demand balance.

How long will it last?

Until now, I have avoided making judgments on "when this conflict will end." On one hand, I don't want to "tempt fate," and on the other hand, it is truly unpredictable.

But one thing is clear: this time is different from past conflicts. The common strategy of "escalate to de-escalate" is not evident this time.

Retaliatory strikes occurred without warning; Iran's strike range also seems to have expanded beyond Israel to include Gulf countries. It was this pattern of response that made me realize from the beginning—this time, it's different.

As the conflict has lasted nearly four weeks, I am increasingly concerned: with an agreement迟迟无法达成, each day of delay significantly reduces the probability of reaching a deal. As we analyzed in "Time is Running Out," Iran understands the operating logic of the oil market very well. It only needs to wait for the market to hit that "tipping point" to secure the maximum concessions from the US in negotiations. From a tactical perspective, reaching an agreement now offers no advantage. The Strait of Hormuz card has been played and cannot be easily reused in the future.

For the Gulf countries, if the current Iranian regime is not overthrown, this situation of being "strangled" will recur in the future. Even if some kind of "toll" mechanism is established, this uncertainty would still be hard to accept.

Therefore, logically, the initiative does not lie with the US but with Iran. In this case, Iran has more incentive to push the situation towards the oil market's "tipping point" to test US endurance. All it needs to do is "hold on" for another three weeks, until the market begins to crack.

However, it must be emphasized that I am not a geopolitical expert and have no absolute certainty about such judgments. What I can provide is an assessment of the current situation based on fundamental analysis.