The landscape of crypto investment continues to expand. Hundreds of new tokens are launched each year, the number of equity stocks related to digital asset businesses is increasing, and tokenization technology is gradually bringing traditional assets like stocks and commodities on-chain. While investment choices are becoming more abundant, market capital is also becoming more selective.

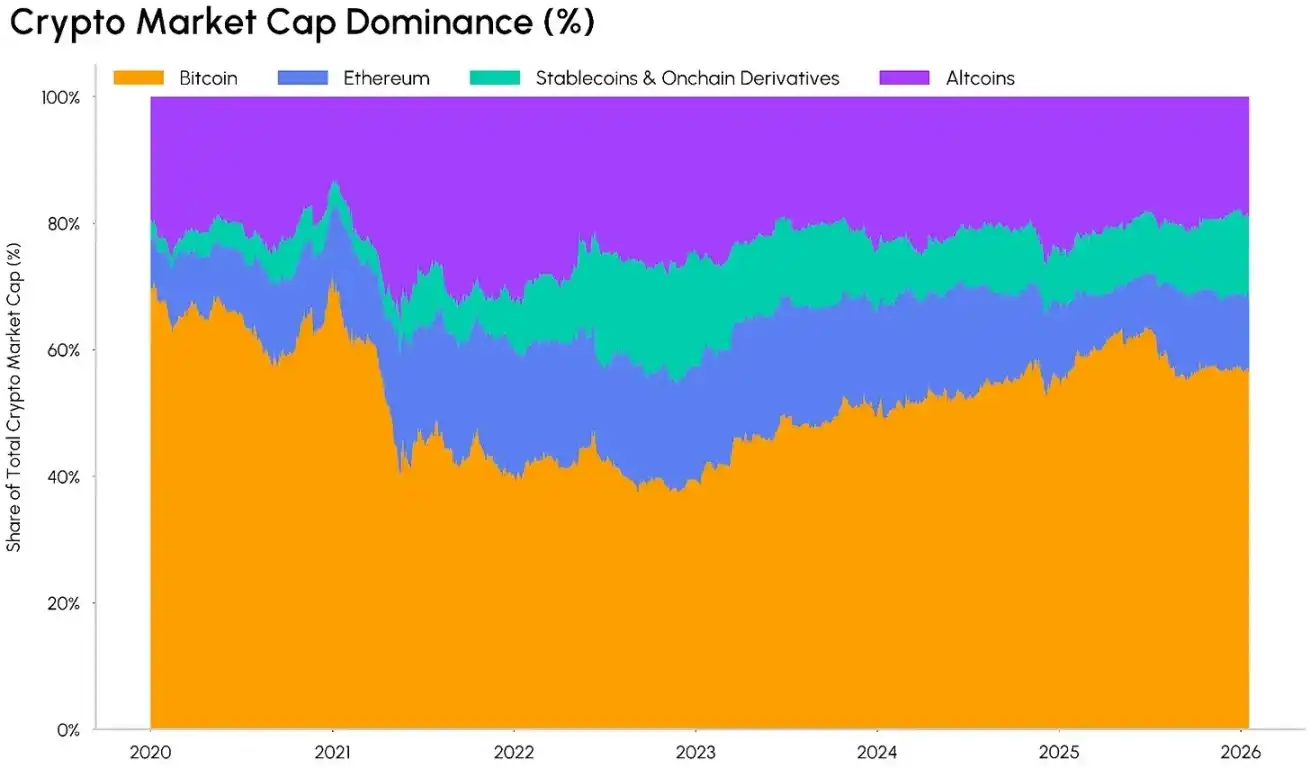

Bitcoin's market dominance has rebounded to around 65%, reaching its highest level since early 2021; at the same time, the combined market capitalization of stablecoins and on-chain derivatives (such as wrapped tokens, staked tokens, cross-chain bridge tokens, etc.) now accounts for nearly 12.5% of the total crypto market cap. As a result, altcoins are facing a double squeeze—despite the growing number of tokens, their overall market share is shrinking.

This issue of the "State of the Network Market" report explores whether the crypto market is undergoing a structural shift towards capital concentration. We will analyze trends in market dominance and returns across assets of different market cap tiers and sectors to investigate whether capital is consistently aggregating towards fewer, larger, and more mature tokens, or if investment opportunities remain widely distributed.

Evolution of Market Cap Dominance

First, we begin our analysis from market cap dominance. Bitcoin's market dominance (i.e., Bitcoin's market cap as a percentage of the total crypto market cap) climbed to 65% in 2025, hitting a new high since 2021. Notably, this growth is not a short-term spike but a long-term, steady upward trend since its trough in 2022.

The launch of Bitcoin spot ETFs has deepened institutionalization, attracting over $150 billion in long-term capital, further driving the sustained rise in its market dominance. This trend solidifies Bitcoin's position as a "safe-haven asset" in the crypto market and makes it a highly liquid, standardized entry point for traditional institutional investors. Compared to previous bull markets where "altcoin seasons" quickly diluted Bitcoin's market share, Bitcoin's dominance in this cycle is more enduring.

Bitcoin Dominance, Data Source: Coin Metrics

The structure of other assets in the crypto market is also changing. Stablecoins, with a current market cap exceeding $300 billion, and on-chain derivatives are increasingly accounting for a larger share of the total market capitalization. These tokens serve different functions within the crypto ecosystem: stablecoins are the primary medium of exchange in the market, while on-chain derivatives provide investors with claims on the returns of underlying assets or channels for generating yield.

Crypto Market Dominance Distribution, Data Source: Coin Metrics

As a result, the altcoin market is facing a dilemma. The range of investable targets is continuously narrowing, and the concentration effect at the top is becoming more pronounced: market value is consistently aggregating towards more liquid and mature assets, which often have clear use cases, defined regulatory development paths, and can fully benefit from the growth waves of stablecoins, decentralized finance (DeFi), and asset tokenization.

Unlike previous market cycles, the speed of capital rotation from major coins to altcoins has significantly slowed in this cycle. ETFs and various institutional investment tools have locked market liquidity firmly in top-tier assets. However, this market structure may change with the implementation of universal listing standards, the launch of altcoin and multi-asset ETFs broadening investment channels for more large-cap altcoins, and the advancement of market structure-related legislation.

The 'Giant Monopoly' Trend Within the Altcoin Sector

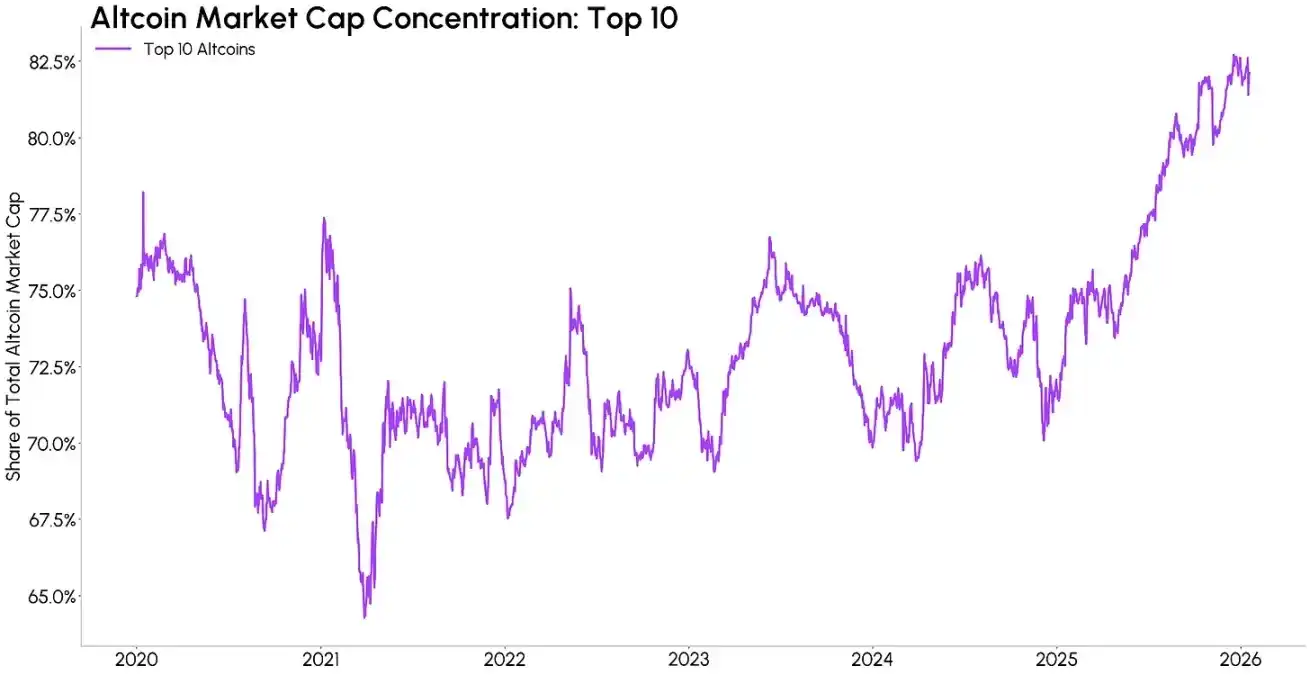

Even within the altcoin sector itself, the trend of capital concentration is intensifying. The current top 10 altcoins by market cap (excluding Bitcoin) account for about 82% of the sector's total market value, a significant increase from 64% during the 2021 bull market. In the previous bull cycle, a large number of small-cap altcoins that briefly created value have gradually exited the market, replaced by a sector structure with stronger top-heavy effects, and the lifecycle of various short-term market narratives has shortened, making it difficult to sustain the continued rise in asset value.

Top 10 Altcoin Market Cap Share, Data Source: Coin Metrics

We can also observe this concentration trend by looking at the number of tokens breaking through specific market cap thresholds. Although the total crypto market cap has repeatedly reached new all-time highs, the number of altcoins with a market cap exceeding $1 billion has shrunk from about 105 at the peak in 2021 to about 58 currently. This means that even as the total number of assets in the market increases, the number of truly "investable" altcoins is decreasing. While this does not necessarily mean the altcoin sector is declining, the focus of market funds may further aggregate towards targets with solid fundamentals and stronger risk resistance.

Number of Altcoins with Market Cap Over $1 Billion, Data Source: Coin Metrics

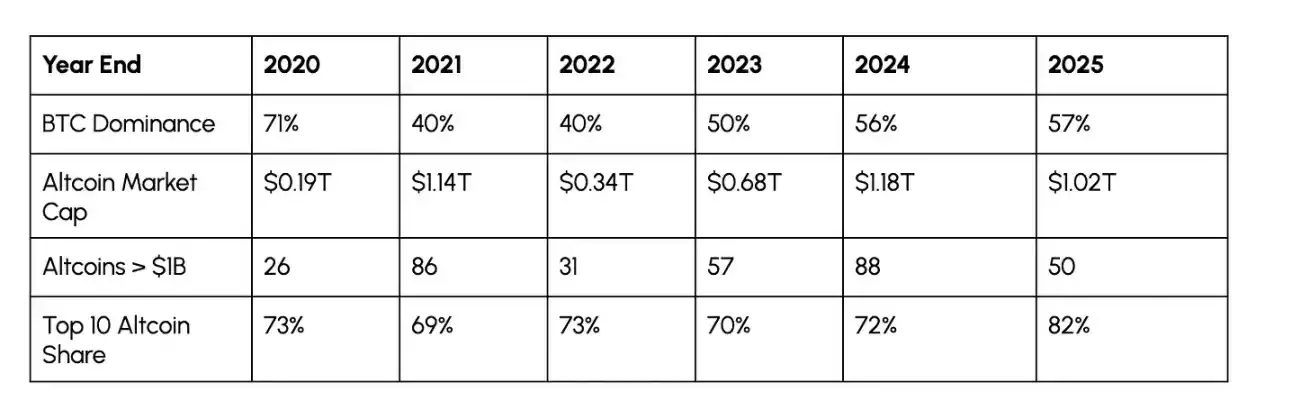

The table below summarizes the annual evolution characteristics of the aforementioned market trends. Some indicators still show cyclical features, such as Bitcoin's market dominance falling in bull markets and rising in bear markets, but the market share of the top 10 altcoins has shown a different trend: from 2020 to 2024, regardless of market conditions, this ratio remained stable between 69%-73%, but it surged to 82% in 2025. This change indicates a structural shift tilting towards mature leading assets, rather than merely short-term "chasing quality assets" behavior.

Data Source: Coin Metrics

Capital Flows to Major Coins

This capital concentration trend is also reflected in asset return performance. Since 2023, mid-cap coins (market cap $1B - $10B) and especially small-cap coins (market cap $10B) during early and late phases of 2024, but this trend reversed sharply in 2025, driven by a rapid fading of market sentiment towards Meme coins and other short-term narrative rotations.

Calculated on an equal-weight basis, from January 2023 to the present, the overall return of crypto large-cap coins is approximately 365%, while the returns of mid-cap and small-cap coins are only about 70% and 55% respectively, with most of the earlier gains being given back. This divergence in returns fully demonstrates that market performance is increasingly tilting towards developed, liquid assets, and the gains of small-cap tokens are unlikely to replicate the sustainability seen in previous cycles.

Market Performance of Tokens by Market Cap Sizes, Data Source: Coin Metrics

On October 10, 2025, the market experienced a large-scale liquidation event triggered by high leverage and liquidity drying up. This event may further strengthen the trend of capital shifting towards defensive assets, with investors increasingly favoring highly liquid assets over significantly more volatile small-cap assets.

Conclusion

Various data indicate that the crypto market is in a stage of structural change, gradual maturation, and consolidation. Although the number of crypto assets continues to increase, and as underlying infrastructure, the types of traditional assets being onboarded are becoming richer, the overall liquidity of the market is limited. Furthermore, within multi-asset portfolios, crypto assets must also compete for space with popular investment themes in the stock market and traditional safe-haven assets like gold.

Currently, capital is continuously aggregating towards crypto large-cap coins and the infrastructure sectors supporting stablecoins, tokenized assets, and decentralized finance. The importance of liquidity and scale has increased further compared to the past, and the threshold for altcoins to attract long-term capital has risen significantly.

Of course, if market structure-related rules become clearer, altcoin and multi-asset ETFs continue to gain popularity, coupled with improved market liquidity conditions, a new altcoin season could still be catalyzed. However, it is foreseeable that the beneficiaries among altcoins in this cycle will be more concentrated, and capital's choices will be more selective than in any previous cycle.