Author: 0xMedia

Naval is stepping into the arena.

This time, he's not just discussing wealth, freedom, and leverage on a podcast, nor is he commenting on startup trends as a Silicon Valley thinker and angel investor. Instead, he is directly taking on the role of Chairman of the Investment Committee at USVC.

This signal itself is very telling. Naval is not someone who would easily endorse a financial product. His persona is complex: co-founder of @AngelList, a representative figure of early-stage investment culture, an evangelist for the Silicon Valley entrepreneurial spirit, and a long-standing intellectual symbol in the Web3 world.

So when Naval @naval chooses to step into the forefront for USVC, it's not just about the launch of a new fund. It seems more like a retail extension of AngelList's over-a-decade-long infrastructure for startup financing.

In the past, AngelList served entrepreneurs, angel investors, fund managers, and private capital networks. Now, it is attempting to break down a portion of the access to venture capital, once reserved for a select few, into a gateway that ordinary people can also participate in.

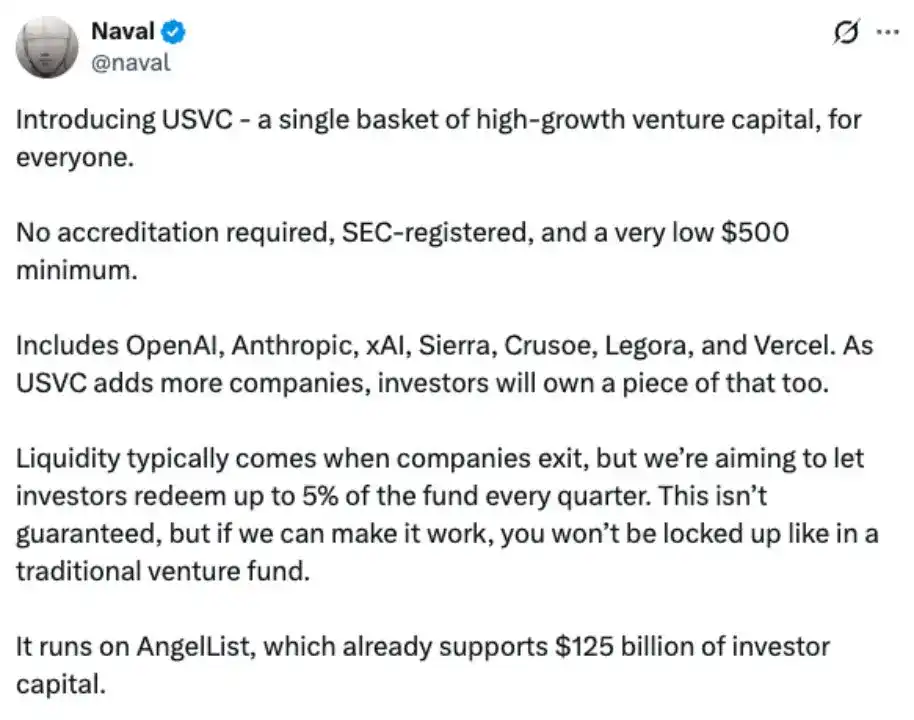

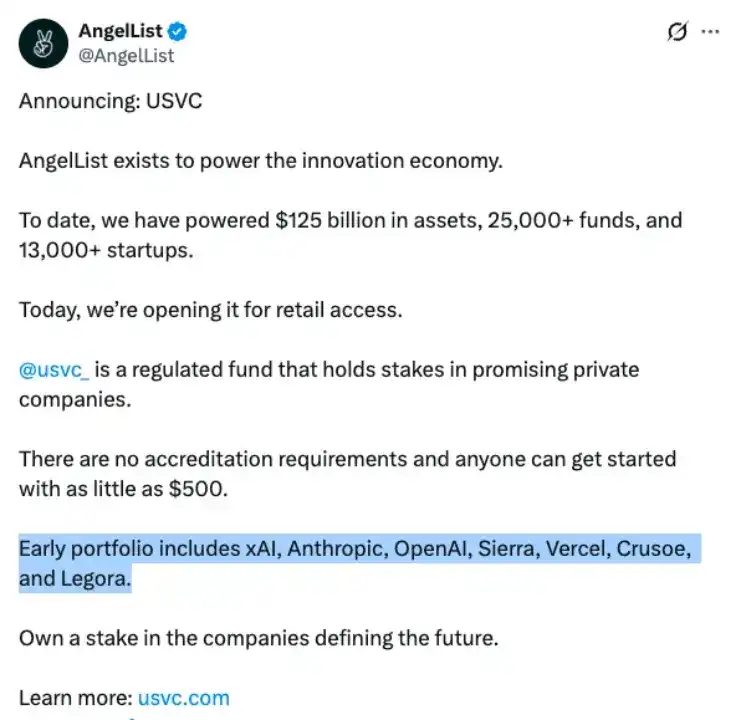

USVC is an SEC-registered fund with a minimum investment of $500, requiring no accredited investor status. Its early portfolio includes companies like OpenAI, Anthropic, xAI, Sierra, Crusoe, Legora, and Vercel.

This is the real point of discussion that USVC provokes. It's not simply selling a basket of AI star companies; it's responding to an increasingly尖锐的时代问题: when the most explosive tech growth happens earlier and earlier in the private markets, can ordinary people still participate in the future sooner?

Over the past decade, the most brutal change in tech investing hasn't been the AI explosion, nor the revaluation of SaaS or chip stocks, but the overall forward shift of the wealth creation timeline.

Many of the most important companies complete multiple rounds of massive funding and value leaps long before entering the public markets. By the time ordinary investors can finally buy in through an IPO or the secondary market, the story has often been told many times over, valuations have been fully priced by earlier rounds of capital, and the truly asymmetric alpha has already been captured upfront by private capital.

For example, as we all know, Benchmark merely led a $75 million funding round in April 2025 for Manus, securing a position in this AI Agent newcomer's most critical growth window.

At that time, Manus @ManusAI was valued at around $500 million, and just months later, Meta acquired it for over $2 billion, delivering early capital an approximate 4x paper return in a very short time.

This is the most alluring aspect of venture capital. The real alpha often occurs when ordinary people don't yet have the qualifications to enter.

Names like OpenAI, Anthropic, xAI, and Vercel are exciting not just because they represent AI, large models, developer tools, and next-generation software infrastructure, but because they symbolize a fact: the future is being bought earlier and earlier.

Ordinary people use these products daily, contributing data, attention, subscription revenue, and ecosystem growth, but at the capital level, they often can only stand outside the glass window, watching institutions, funds, and high-net-worth investors participate in the value revaluation.

It is precisely this glass pane that USVC is attempting to shatter.

The entry point it offers is very direct: ordinary people can participate with a minimum of $500 in a venture capital basket composed of high-growth private tech companies. This threshold, placed alongside the names of these assets, creates a stark contrast.

* US Early VC vs. S&P 500 returns, from USVC website https://usvc.com/

In the past, those who could access such assets were typically top VCs, family offices, sovereign wealth funds, university endowments, or accredited high-net-worth investors. Now, USVC is attempting to productize,合规化, and retail this asset exposure, placing it before ordinary investors.

But precisely because of this, USVC cannot be understood merely as an emotional product of "$500 to buy OpenAI." The真正复杂的地方在于, venture capital is never just about buying the name of a good company, but about the price, stage, structure, fees, and liquidity terms at which one buys.

OpenAI, Anthropic, and xAI are certainly the most watched tech companies of this era, but a great company does not automatically equate to a great investment. Especially after they have undergone multiple rounds of high-valuation funding, what investors真正需要判断 is not whether these companies are strong enough, but whether the future returns through USVC still possess sufficient吸引力.

This is also why Naval's involvement is crucial. Naval's symbolic significance is not just his influence, but that he represents a long-term understanding of entrepreneurship, capital, networks, and leverage.

One of the most important things AngelList did back in the day was to partially loosen startup financing from extremely closed circles, allowing more angel investors, entrepreneurs, and new fund managers to connect through the platform.

What USVC is doing today is, in a sense, a continuation of the same logic: if AngelList once reduced the organizational cost of the startup financing network, then USVC is now attempting to lower the barrier to entry for ordinary people to access venture capital assets.

However, the expansion of access does not mean the disappearance of risk.

USVC is not an ETF. It cannot be traded intraday like a Nasdaq ETF, nor can it be bought and sold at any time like public stocks. Its underlying assets are private companies and private fund shares, inherently characterized by low liquidity, opaque valuation, and long exit cycles.

The team mentions hoping to achieve up to 5% fund redemptions quarterly in the future, but this does not mean investors can exit at any time. More accurately, this is a designed partial liquidity, not the天然具备的高流动性 of the underlying assets.

The fee issue同样不能回避. USVC's current all-in fee for the first year is 2.5%. At first glance, this number is certainly high compared to S&P 500 ETFs, Nasdaq ETFs, or other low-cost index products.

But if compared within the traditional venture capital system, the situation becomes much more complex. The common fee structure for traditional VCs is 2/20, meaning a 2% annual management fee plus a 20% performance fee (carried interest).

If investing indirectly through a fund of funds, an additional layer of fees might be stacked on top of the underlying VC fees. USVC's proposition is that the current 2.5% includes fees related to the underlying funds, with AngelList absorbing costs exceeding that比例 in the first year, and USVC charging no additional fees for direct investments.

If it were merely repackaging already very expensive late-stage star assets for retail investors, then 2.5% would be hard to call cheap. But if it can consistently secure truly scarce, completely inaccessible-to-ordinary-people, and still attractively valued优质私募资产 through the AngelList and Naval network, then this fee更像是一种进入风险资本网络的通行成本.

In other words, the greatest value of USVC lies not in being cheap, but in whether it can持续提供真实的、稀缺的、值得付费的风投权限.

This is also where USVC subtly intersects with the Web3 narrative.

Over the past few years, Web3 has been talking about financial inclusion. DeFi allows ordinary people to lend, trade, market-make, and participate in yield strategies on-chain; RWA attempts to bring real-world assets on-chain; stablecoins have made dollar payments globalized, low-friction, and real-time.

But USVC is taking a different path. It hasn't used tokens to achieve asset openness, nor has it used on-chain mechanisms to provide liquidity. Instead, through an SEC-registered fund, NAV, an investment committee, the AngelList network, and compliant distribution channels, it is bringing exposure to previously closed private tech assets before ordinary investors.

The paths are different, but the underlying question is similar: Who is qualified to own the future? USVC might not be a ticket to guaranteed returns, but rather a ticket to get closer to the future, sooner. DYOR.