Who would have thought that Microsoft—the tech giant that has cumulatively invested over $10 billion in OpenAI—has recently suspended the internal use of Claude internally, also citing that it is "too expensive to use."

Here's what happened: Recently, an internal message circulated at Microsoft, stating that starting June 30, thousands of engineers responsible for work related to Windows, Microsoft 365, Teams, Outlook, and Surface will no longer be permitted to use Claude Code. Microsoft is directing them to switch to its own GitHub Copilot CLI.

Microsoft has not publicly disclosed the specific amount spent on Claude Code, but informed sources reveal that the suspension of Claude Code was indeed due to the excessively high costs, high enough to make even Microsoft feel the "pinch."

Not long ago, Uber made the same choice as Microsoft.

According to leaks, Claude Code costs Uber roughly $500 to $2000 per engineer per month in AI tool expenses.

What does this mean? For a hundred-person technical team, this single AI tool alone amounts to several million dollars per year. Uber's AI budget for 2026 was "burned through" by April.

Behind this lies a change many companies haven't yet grasped but are starting to find troublesome: the pricing model for AI is shifting from a previous "subscription plan" to a current "pay-per-use" model.

In the past, many AI tools adopted a fixed monthly fee model, with relatively predictable costs. But now, more and more AI assistants for programming scenarios are switching to a token-based billing method—the more complex the query, the more frequent the calls, the deeper the tasks, the higher the cost incurred. For technical teams that need to handle large volumes of coding work daily, this expense is rapidly swelling into a significant financial pressure that cannot be ignored.

Against this backdrop, even tech companies the size of Microsoft and Uber are forced to recalculate: Are the high costs of third-party AI tools truly worth it? Should they continue paying the ever-increasing bills, or switch to more economical open-source solutions, or use their own tools as replacements?

Microsoft's choice is clear: replace Claude Code with its own GitHub Copilot CLI. Although the feature experience might be slightly inferior, the costs are controllable, and internal resource flow is more efficient.

This choice sends a clear signal—AI pricing that even Microsoft finds "expensive" is forcing companies to re-examine their technology procurement strategies.

After all, the saved costs will ultimately be directly reflected in profits.

However, The Verge also points out that canceling the Claude Code license will not affect the Foundry agreement between Microsoft and Anthropic. This agreement includes an investment of up to $5 billion in Anthropic, providing Foundry customers with access to Claude models, and Anthropic's commitment to spend $30 billion on Azure computing capacity.

2 Was Letting Employees Use Claude Code Just an Experiment?

Microsoft's sudden revocation of Claude Code usage permissions for internal engineers came six months after allowing employees to use the tool, leading outsiders to view this not as a hasty ban, but rather a carefully arranged experiment.

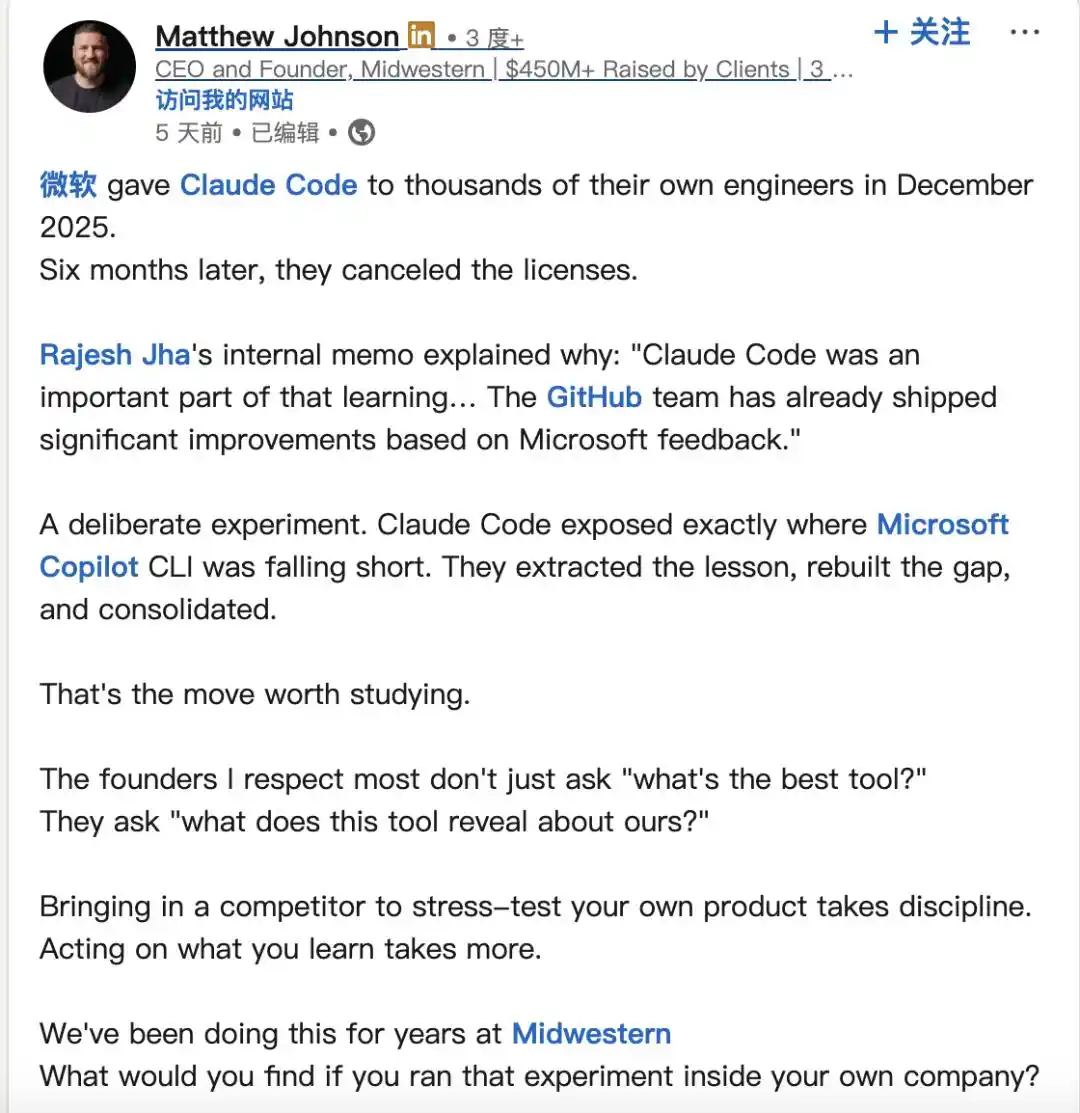

According to an internal Microsoft memo, Rajesh Jha, Executive Vice President of the Experiences & Devices group, provided an explanation: "When we started offering both Copilot CLI and Claude Code, our goal was to learn quickly, benchmark these tools in real engineering workflows, and understand which tools best support our teams. Claude Code played a significant role in this learning process... At the same time, Copilot CLI brought us something particularly important: a product we can build directly with GitHub, tailored to Microsoft's codebases, workflows, security expectations, and engineering needs."

In other words, Microsoft proactively allowed a competitor's product into its engineering teams, exposing Copilot CLI's shortcomings using Claude Code. Then, over six months, they collected feedback, closed the gaps, and finally shut down the competitor's tool, migrating all engineers back to their own product.

On LinkedIn, a user summarized this strategy as: first let the competitor be the "sparring partner," then close the net after learning.

A LinkedIn user commented on this: "If Microsoft wanted to continue using Claude, cost would definitely not be a hindering factor. Microsoft's former Tokenmaxxing strategy seems like it was aimed at learning from the start."

Another user stated, "Using a competitor's product to stress-test your own requires strong discipline. And putting the learned knowledge into practice requires even more effort."

Looking at the results, Microsoft indeed did this. Copilot CLI underwent multiple iterations over the six months based on engineers' comparative usage feedback.

Therefore, this discontinuation is interpreted not as a passive abandonment due to "can't afford it," but as an active conclusion of this internal experiment after leveraging the competitor's strength to patch up its own weaknesses.

However, outside views on this are not unanimous. Some developers point out that Microsoft could do this because it simultaneously possesses underlying cloud infrastructure, its own code hosting platform GitHub, and a sufficiently large engineer base as "experimental samples." Most companies lack these conditions—they can only simply "not afford it," whereas Microsoft can choose to "learn and then stop."

3 Behind Halting Claude Code, Microsoft Faces Three Major Dilemmas

However, cost pressure and external speculation about an "experimental test" might only be the tip of the iceberg. Microsoft's decision to halt Claude Code touches upon a more unsettling fact for this software giant: in the industrial chain of the large model era, Microsoft is losing its power to define.

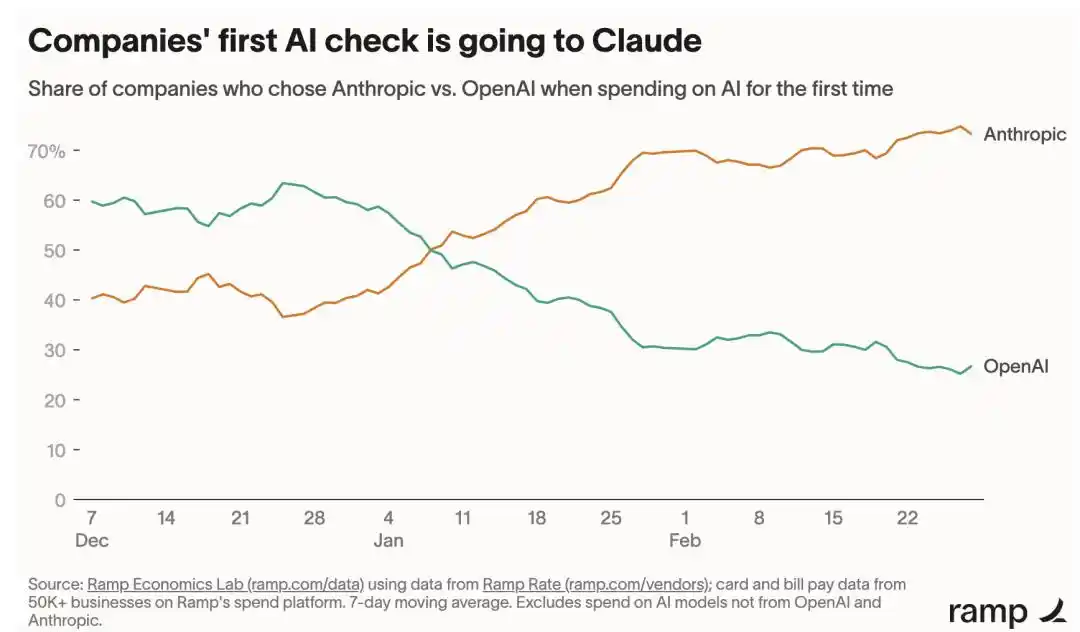

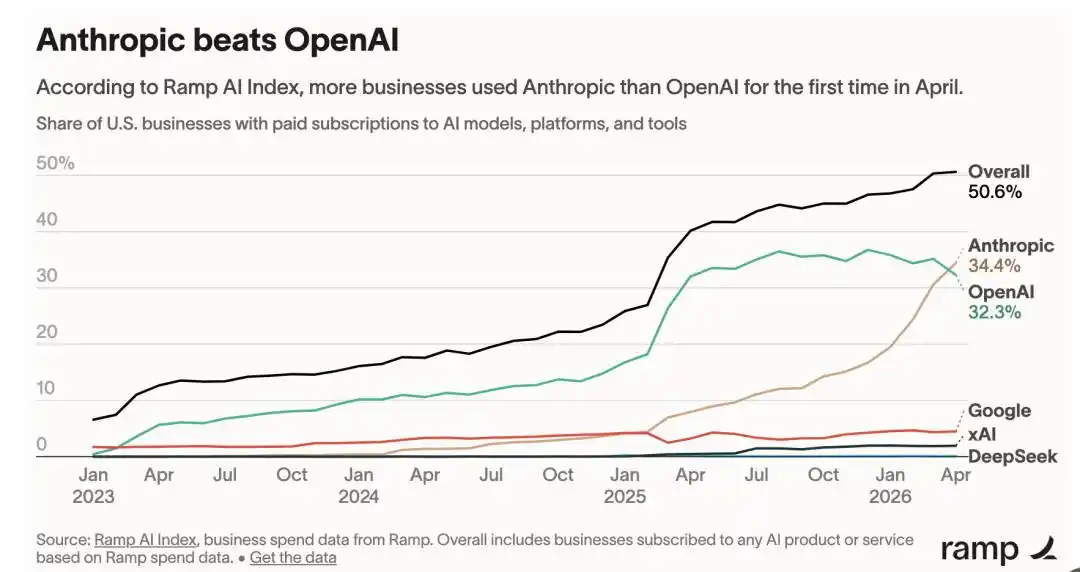

In March 2026, enterprise spend management platform Ramp released an AI Index report. Among enterprises purchasing AI services for the first time, Anthropic won about 70% of direct confrontations with OpenAI. This was completely opposite to the trend Ramp observed in 2025, when OpenAI's adoption rate surpassed any other model company. Anthropic's annualized revenue soared to $19 billion, closing in on OpenAI's $25 billion.

By April, according to Ramp, Anthropic's enterprise AI adoption rate had reached 34.4%, surpassing OpenAI's 32.3% for the first time, becoming the new top AI supplier in the enterprise market. The core engine driving this reversal was precisely Claude Code—this programming tool achieved $1 billion in annualized revenue within just six months of its release, accounting for 4% of all GitHub code commits at the time.

In this market shift, Microsoft occupied almost no significant position.

While Microsoft was forced to rely on external models from OpenAI and Anthropic, the annualized revenue of AI startups reached $80 billion in 2026, with OpenAI and Anthropic together capturing 89% of that.

This reveals a harsh reality: the commercial value of foundation models is flowing back to the model developers, while Microsoft—is just a distributor. When a distributor tries to block the source, it can only indicate one thing: it can no longer purchase a real ticket to the game.

Summarizing perhaps: Microsoft has been marginalized on three battlefields: models, developers, and ecosystem control.

Dilemma One: No Cutting-Edge Foundation Model, Heavy External Reliance

To this day, Microsoft's biggest hidden worry is that it still lacks a truly cutting-edge general-purpose large model of its own.

Since 2019, Microsoft has cumulatively invested over $13 billion in OpenAI, acquiring approximately 27% equity, but its self-developed large language models have never managed to match GPT-4 or Claude.

In April 2026, the three MAI series models released by Microsoft's AI research lab—MAI-Transcribe-1, MAI-Voice-1, and MAI-Image-2—only covered speech transcription, voice generation, and image creation, and did not launch a general-purpose large language model.

Although Microsoft possesses one of the world's strongest AI commercial entry points, it lacks the "foundation model control" that truly determines the upper limit of AI capabilities.

Lacking a self-developed general model, Microsoft cannot achieve a technological closed loop in core scenarios like general conversation and programming reasoning. Its core AI capabilities are tied to OpenAI. In April 2026, Microsoft and OpenAI jointly announced the end of their seven-year exclusive binding. Azure is no longer OpenAI's only cloud outlet, and IP licensing has shifted from exclusive to non-exclusive.

In the past, one of Microsoft's biggest moats was "exclusive access to OpenAI." But now, that exclusivity is loosening.

And once Microsoft loses its exclusive binding with OpenAI, it must face a brutal reality: it does not have an underlying model capable of replacing GPT-4 or Claude. This is why Microsoft today exhibits a very fragmented state in the AI field: it is one of the companies with the deepest AI commercialization globally, but simultaneously, it is highly reliant on external models for core capabilities. This "strong platform, weak model" structure is essentially a form of technological hollowing out.

Dilemma Two: Its Own Product Prowess Is Inferior to Competitors

What's even more disheartening for Microsoft is that not only does it lack a standout general-purpose large model, but even Copilot, which once captured the early intelligent programming window, is being substantively surpassed by Claude Code.

Over the past two years, GitHub Copilot has been synonymous with AI programming. But the AI programming market in 2026 has fundamentally changed. Where Claude Code truly revolutionized the industry is by turning a "code completion tool" into a "long-context engineering agent."

Traditional Copilot is more like: "help you write a few lines of code." Claude Code can directly participate in the entire software engineering process.

Inside Microsoft, the most popular programming tool is not its own Copilot, but Claude Code.

According to The Verge reporter Tom Warren, Microsoft engineers have "clearly preferred" Claude Code over their own tool in recent months. This preference does not stem from employees "not loving their own product," but from a substantive gap in product capability itself.

According to test data, Claude Code scored 80.8% on SWE-bench, while GitHub Copilot based on GPT-4o scored only 72.5%, a difference of 8.3 percentage points.

Claude Code supports a million-token context window, capable of processing about 3000 files in a single session, whereas Copilot CLI's limit is only 128K tokens. In scenarios involving refactoring or debugging across dozens of files, Claude Code's completion rate is 89%, while Copilot's is only 60%.

Engineers using Claude Code daily means development workflows, debugging data, and operational habits are all being deposited within Anthropic's ecosystem. According to The Verge, before opening Claude Code internally, 91% of Microsoft engineering teams used GitHub Copilot, but over the past six months, Claude Code usage has "severely eroded" this proportion.

Rajesh Jha, head of Microsoft's Experiences & Devices group, acknowledged in the memo that Claude Code was "an important part of the learning process," yet still mandated the switch. The root of this contradiction lies in a fundamental anxiety at the strategic level—when engineers entrust a key link in the development toolchain to an external product, Microsoft's control over its own technology stack is gradually weakening.

Long-term employee use of external tools means cultivating user habits for competitors, potentially taking development skills and process knowledge directly to competing companies in the future.

A Microsoft insider told The Information that Claude Code satisfaction among Microsoft engineers is as high as 91%. When a company's core developers are less satisfied with their own tools than with an external competitor's product, its technological cohesion faces a major challenge. This is not about "fearing the competitor making money," but worrying about the development culture being infiltrated by external tools, leading to core talent and development processes being locked into a competitor's product.

Dilemma Three: Weakening Ecosystem Control

What makes Microsoft even more uncomfortable is: not only are internal engineers shifting to Claude, but the entire enterprise market is also beginning to show a similar trend.

Microsoft has invested in its two main partners, OpenAI and Anthropic, but both are gradually shedding their dependence on Microsoft.

According to Ramp's AI Index data, in April 2026, Anthropic's enterprise-paid adoption rate reached 34.4%, surpassing OpenAI's 32.3% for the first time. Over the past 12 months, Anthropic's enterprise adoption rate surged from just 9% to 34.4%, a near four-fold increase, while OpenAI's enterprise adoption rate grew only 0.3% over the same period.

When enterprises purchased AI services for the first time in 2026, in about 70% of direct confrontations, the final contract went to Claude, not ChatGPT.

The core engine driving this reversal is precisely Claude Code.

According to market estimates, approximately 4% of global GitHub public commits involve participation by Claude Code, and Anthropic expects this to exceed 20% by the end of 2026. Claude Code holds 54% share of the AI programming tools market, with 8 of the world's top ten Fortune companies as paying customers. In terms of annualized revenue, Claude Code surpassed $1 billion in November 2025, reaching $2.5 billion by early 2026. In comparison, OpenAI's Codex annualized revenue is about $1 billion.

According to Goldman Sachs statistics, the total annualized revenue of AI startups in 2026 is about $80 billion, with OpenAI around $25 billion, Anthropic around $19 billion, the two combined accounting for 89%. When Claude Code's revenue is captured by Anthropic and not Microsoft, the role Microsoft essentially plays is still that of a distributor—providing computing power and some investment, yet failing to capture the thickest profits from the core value of large models.

In April 2026, Amazon and OpenAI reached a strategic partnership, with Amazon committing to invest up to $50 billion, and AWS also becoming the exclusive third-party cloud distributor for OpenAI's enterprise-level platform Frontier.

According to Business Insider, internal Microsoft assessments show GitHub Copilot's share in the AI programming tools market has fallen to about 25%.

These data points mean: AI competition is shifting from "chatbots" to "engineering systems."

And in this round of competition, Claude Code is becoming the new infrastructure entry point. The problem is—Microsoft was supposed to be the biggest beneficiary of this AI programming revolution. Because GitHub already holds the world's largest developer ecosystem.

But now Claude Code captures developer mindshare, Anthropic takes enterprise growth, OpenAI gradually detaches from Microsoft's exclusive system, and more frighteningly, GitHub Copilot is starting to be marginalized.

Microsoft suddenly realizes: it owns GitHub, but may not own the next-generation AI programming ecosystem.

4 One Misstep Leads to Another

The problem Microsoft faces today is no longer as simple as a single product lagging.

On the surface, this is just a management action of "internally discontinuing Claude Code." But looking deeper, one finds behind it an entire chain that is spiraling out of control.

In the beginning, it was Microsoft's delay in creating a truly self-developed general-purpose large model capable of matching GPT-4 or Claude. After lacking foundational model capabilities, it could only long-term rely on OpenAI for core AI capabilities. But the problem is, OpenAI is now also gradually shedding its exclusive binding with Microsoft. Their relationship has shifted from "deep binding" to "cooperative but non-exclusive."

On the other side, something even more dangerous is happening inside Microsoft.

More and more Microsoft engineers are starting to use Claude Code daily, instead of their own Copilot. Superficially, it's just a choice of development tool, but in reality, it affects the entire development ecosystem: code workflows, debugging habits, engineering context, Agent usage patterns—all migrate along with the tool. For a platform company, the scariest thing is never that competitors make money, but that its own developers start working within a competitor's ecosystem.

Next, the problem begins to transmit further.

After developers shift en masse to Claude Code, the real money is made by Anthropic. Enterprise clients also start migrating, and Claude's voice in the AI programming field rapidly expands. Although Microsoft can still make money by providing computing power through Azure, the portion of value with the thickest profits and strongest control in the AI era is being taken by model companies and Agent platforms.

In this situation, a subtle state begins to emerge within Microsoft: products cannot compete, but they cannot continue allowing employees to fully defect to external tools. So the final approach taken is not to first catch up with Copilot's capabilities, but to first suspend internal usage permissions for Claude Code.

This actually shows that the problem is evolving from "product competition" to "organizational defense."

According to The Verge, Microsoft even once considered acquiring Cursor to bridge the gap in AI programming experience for Copilot, but later did not proceed due to factors like regulatory risks.

To some extent, this precisely exposes Microsoft's most awkward position now: it possesses one of the world's strongest developer platforms and the most extensive enterprise customer system, but the most critical entry point in the AI programming era—the Agent tool developers actually use daily—is falling into others' hands.

And once developer habits, workflows, and engineering ecosystems are all re-established, trying to reclaim them later is no longer as simple as adding a few features or changing a product strategy once.

References:

https://ramp.com/leading-indicators/ai-index-may-2026?utm_source=chatgpt.com

https://tech.yahoo.com/ai/copilot/articles/microsoft-ditching-claude-code-copilot-133318848.htmlhttps://fortune.com/2026/05/22/microsoft-ai-cost-problem-tokens-agents/https://www.linkedin.com/posts/matthew-johnson-71a059b3_microsoft-gave-claude-code-to-thousands-of-activity-7462552767300272128-b0dx/

This article is from the WeChat public account "InfoQ" (ID: infoqchina), author: Dongmei.