Author: Andy, Founder of The Rollup

Compiled by: Felix, PANews

Andy, the founder of The Rollup, recently published an article discussing the market landscape of Neo Finance in 2026, pointing out that Neo Finance will become the fastest-growing sector in the global financial system. Below are the details.

The Neo Finance sector will give birth to more true 'billion-dollar unicorn' companies than ever before. It is poised to become the fastest-growing sector in the global financial system for years, and even decades, to come.

Below is the market landscape for Neo Finance in 2026, covering nine major segments and over 100 ecosystem projects:

The combination of front-end consumer-grade user experience and back-end efficient DeFi infrastructure will provide users with a 'bank-like experience' that is both familiar and far superior to traditional banking.

Users' savings can be traded and transferred globally and are available 24/7. A simple example: a user's 'checking account' could earn a 5% annual interest rate, compared to 0.25% from a traditional bank.

Driven by teams focusing on different parts of the technology stack, the Neo Finance market has the potential to fundamentally change how the world interacts with money.

Let's take a look at some key areas in the market map.

Tokenization

Tokenization is the process of bringing real-world assets (such as treasury bonds, stocks, commodities, credit, money markets, etc.) on-chain.

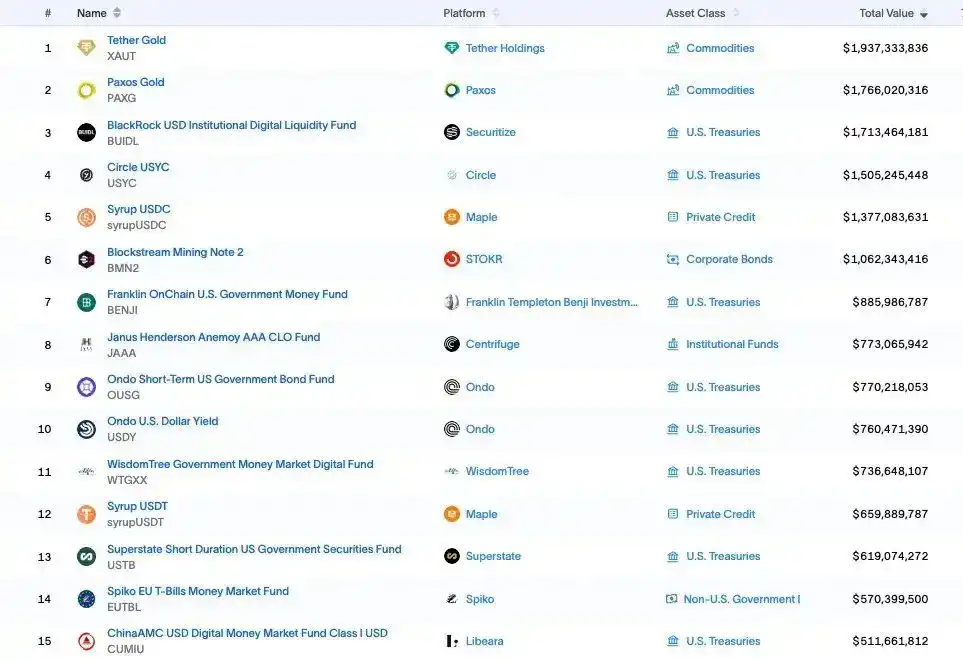

The infrastructure and tokenization agent layer includes: Figure, Ondo Finance, Paxos, Centrifuge, Superstate Inc, Midas, Grove Finance, Nest, Dinari, Securitize, and other companies.

Tokenization has been discussed for years, but 2025 is the year it truly begins to scale.

Stablecoins

Stablecoins are by far the most successful crypto product, with 90% of new finance customers preferring stablecoins as their first point of contact with cryptocurrency.

The stablecoin issuer sector is booming, with numerous companies emerging, such as: Circle, Paxos, Tether, and Sky.

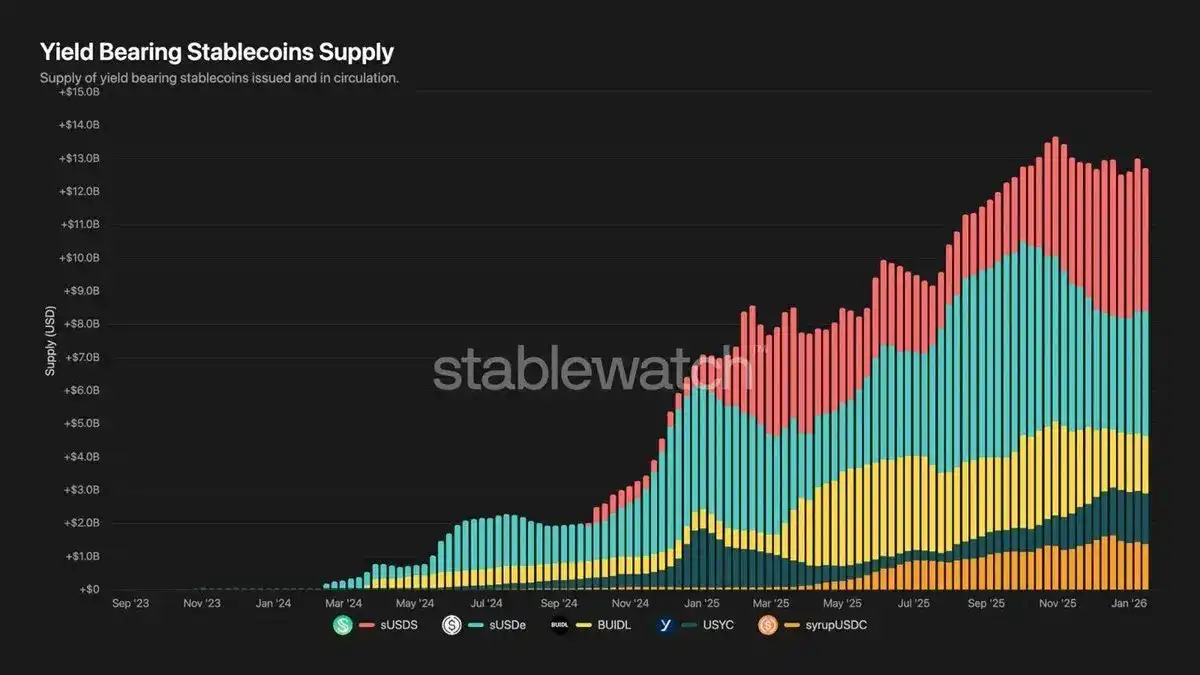

Meanwhile, yield-bearing stablecoins (or 'yield coins') like $sUSDS, $sUSDe, $BUIDL, $USYC, and $syrupUSDC have seen exponential growth over the past 18 months, with a supply exceeding $13 billion.

Users no longer have to choose between stability and yield as they did in the CeDeFi space during 2020-2022; now they can have both.

Neo-Banks

In the neo-bank sector, many teams are emerging, such as ether.fi, KAST, Tuyo, Galaxy, and others. These teams are leveraging DeFi backends to build consumer-facing 'bank-like' experiences from the ground up.

Remember the 'DeFi Mullet'? (PANews Note: Refers to a front-end with a TradFi user-friendly interface and a back-end powered by DeFi underlying technology) It's still here, and the data proves it.

Tokenization, stablecoins, and neo-banks are the three key areas of focus currently, expected to see the most significant growth in 2026 and beyond.

Beyond this, the crypto market is facing a harsh reality: old strategies are failing.

High FDV, low circulating supply launches aimed at dumping on retail; protocols lacking value accrual pathways; alt DEXs on 'ghost' chains; VC-backed projects where founders cash out hundreds of millions before achieving any PMF (Product-Market Fit).

All these plays are outdated, and this trend will continue.

In fact, I got into crypto after reading 'The Truth Machine' in 2017. Back then, I was almost certain this technology would reshape finance. Somehow, it feels like we veered off the original mission. Nine years later, we are closer than ever to that dream becoming a reality.

Everything is in place, the opportunity is here. Welcome to the era of Neo Finance.

Related reading: Nihilism and Vicious Cycles: Why Should We Oppose Over-Financialization?