Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

On January 6th of this year, Polymarket officially ended its "zero-fee" model, beginning a trial implementation of transaction fees starting with the "15-minute cryptocurrency up/down" markets. The specific fee rate varies with the market's real-time odds — the closer the odds are to 0% or 100%, the lower the fee; conversely, the closer the odds are to 50%, the higher the fee, up to a maximum of 1.56%.

Later, on January 28th, about three weeks after the fees were introduced, we published an article titled "Data Estimates Show Polymarket Could Easily Exceed $100 Million in Annual Revenue, Assuming...". The article provided a static estimate based on Polymarket's trading volume and activity structure at the time: in the most conservative scenario, if the scope of fee-charging markets remained unchanged, Polymarket was projected to generate approximately $38 million in annual income; in the most aggressive scenario, if Polymarket extended fees to all markets, it was projected to earn $418 million in annual fee revenue.

When we last estimated Polymarket's revenue, we were hampered by an overly short observation period and too few calculable samples. Now, nearly two months later, we have used richer data to re-estimate Polymarket's revenue expectations. The results show that the so-called "conservative" estimate was indeed too conservative, and the "aggressive" expectation isn't too exaggerated.

Changes in Revenue Data

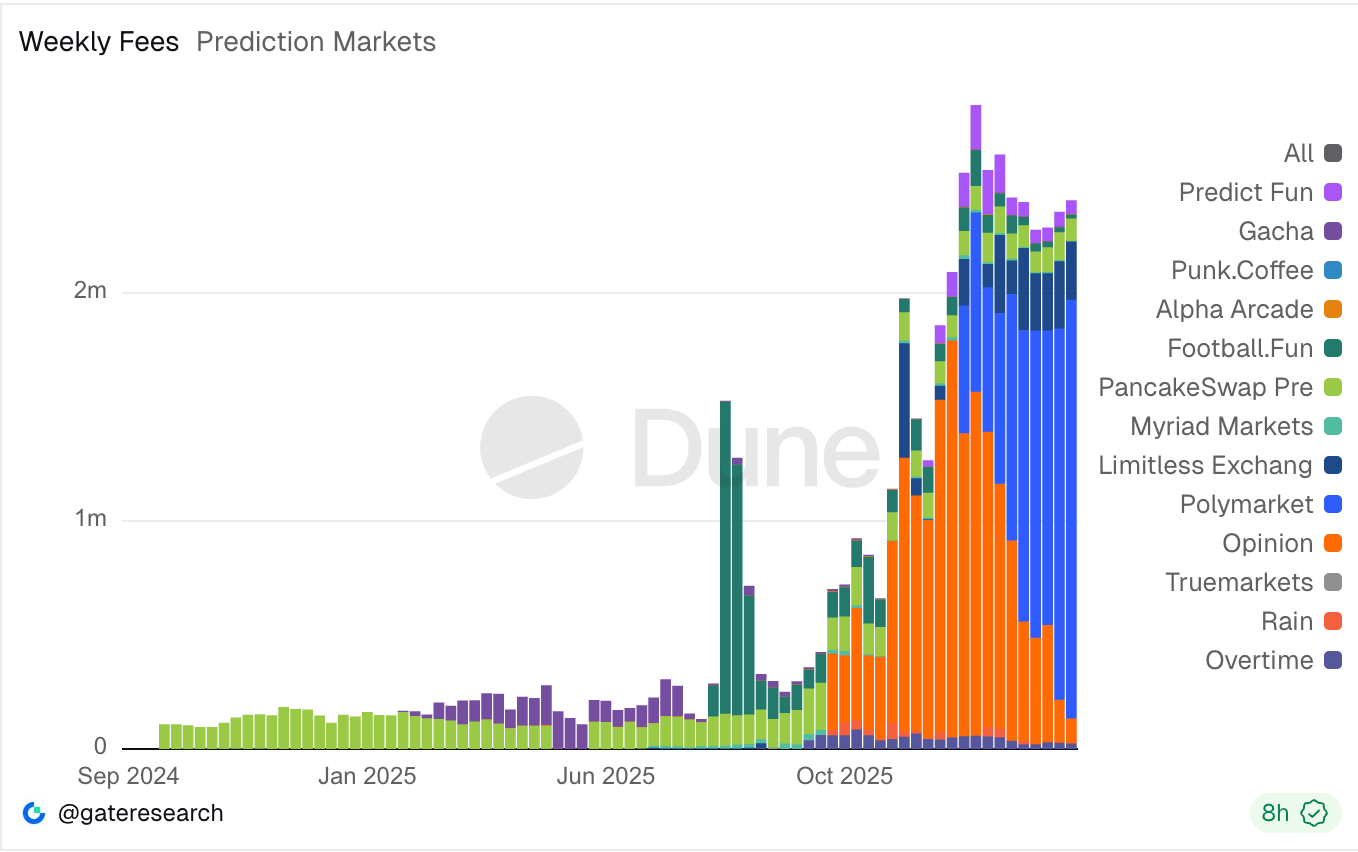

According to data compiled by Gate Research on Dune, since transaction fees were introduced on January 6th, Polymarket has accumulated over $11.2 million in fee revenue.

Using the most conservative method for another static estimate, assuming the trading volume and activity structure of the relevant markets remain unchanged, Polymarket is projected to generate approximately $58.4 million in annual revenue.

However, this estimation method does not accurately reflect Polymarket's revenue-generating capability.

The reason is that Polymarket's revenue data is clearly in a growth trend — over the past 10 weeks, the platform's weekly fee revenue has been $560,000, $786,000, $633,000, $749,000, $1.08 million, $1.28 million, $1.35 million, $1.29 million, $1.63 million, $1.84 million... showing almost weekly significant growth.

Reasons for Revenue Growth

There are two reasons for the growth in Polymarket's fee revenue. First, Polymarket has expanded the scope of fee-charging markets; second, Polymarket's overall trading volume and the trading volume in fee-charging markets have been growing continuously.

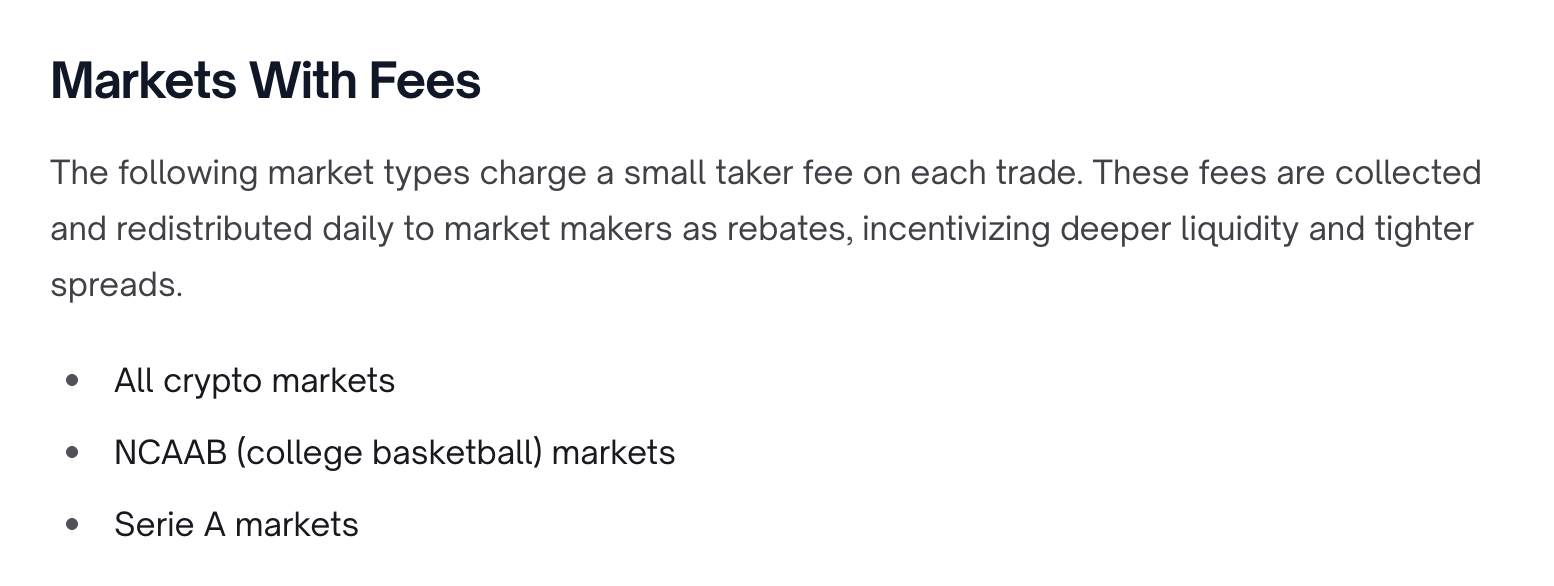

Regarding the scope of fee-charging markets, Polymarket extended the fee mechanism to all cryptocurrency-related markets on March 6th. Additionally, even earlier, it had begun trialing fee collection in sports markets like NCAA and Serie A. However, the former (cryptocurrency-related markets) currently remains the primary source of fee revenue.

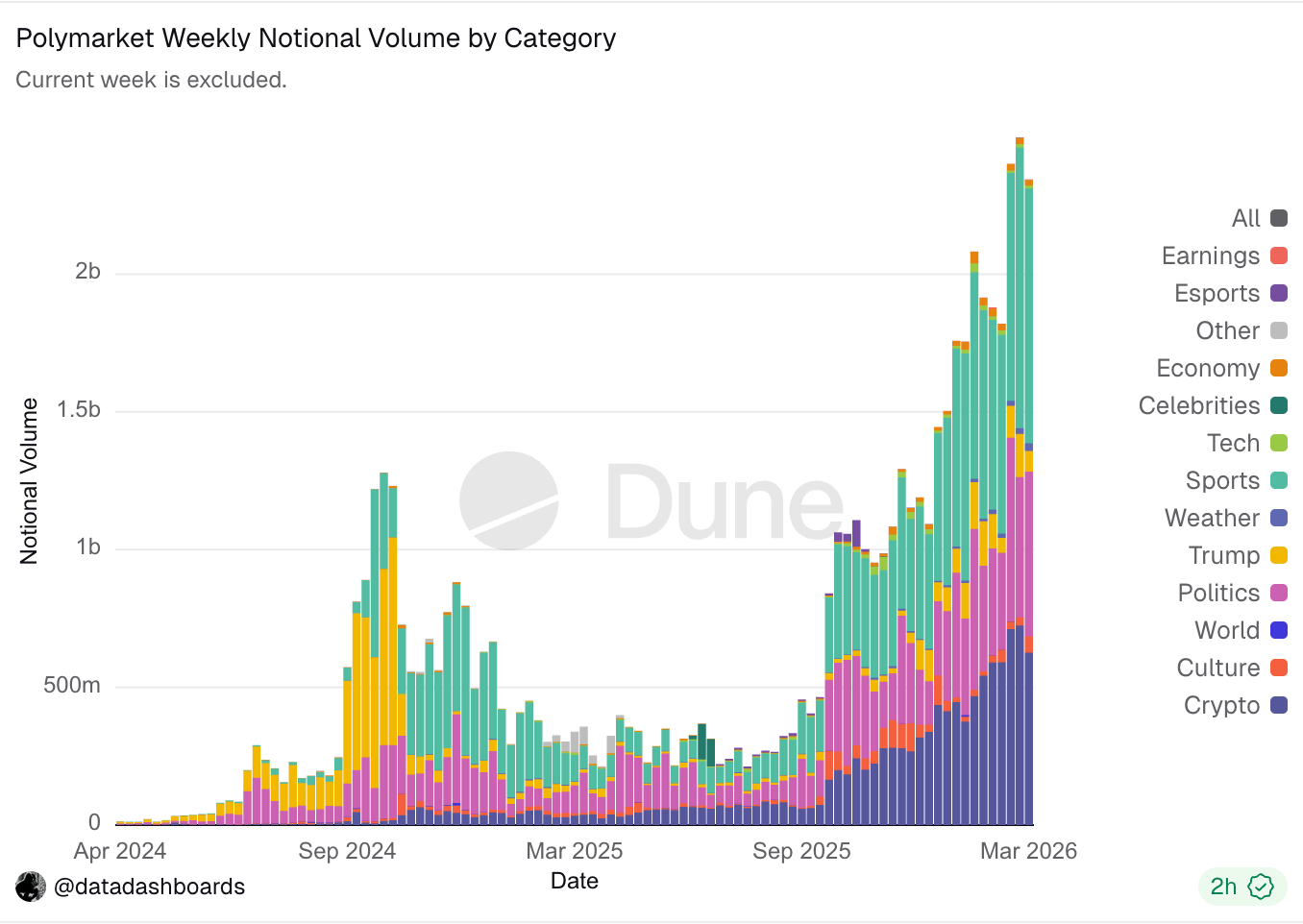

Regarding trading volume, the data dashboard compiled by Data Dashboards on Dune shows that Polymarket's weekly overall trading volume and cryptocurrency market volume (the bottom purple bars) have been growing steadily.

Future Revenue Projections

When we last projected Polymarket's revenue, we had to manually extract the trading volume proportion of "15-minute cryptocurrency up/down" related markets within all cryptocurrency-related markets. But now, since Polymarket extended fees to all cryptocurrency-related markets on March 6th, this estimation is much more straightforward. As for NCAA and Serie A, perhaps because the former hasn't entered the "March Madness" official tournament yet, and the latter has relatively low cultural attention in the US, the trading volume scale of these markets is significantly smaller compared to cryptocurrencies, so they are temporarily ignored here.

Taking data from the only full week after March 6th (March 9th-15th), the trading volume of cryptocurrency-related events accounted for 26.7% of the platform's total trading volume that week. In the same week, Polymarket's fee revenue was approximately $1.84 million. Based on this ratio for a static projection, under the current trading volume level and structure, if Polymarket introduces a similar fee model across all markets, it is projected to bring in $360 million in annual revenue for the platform.

The Money Printer is Already Running

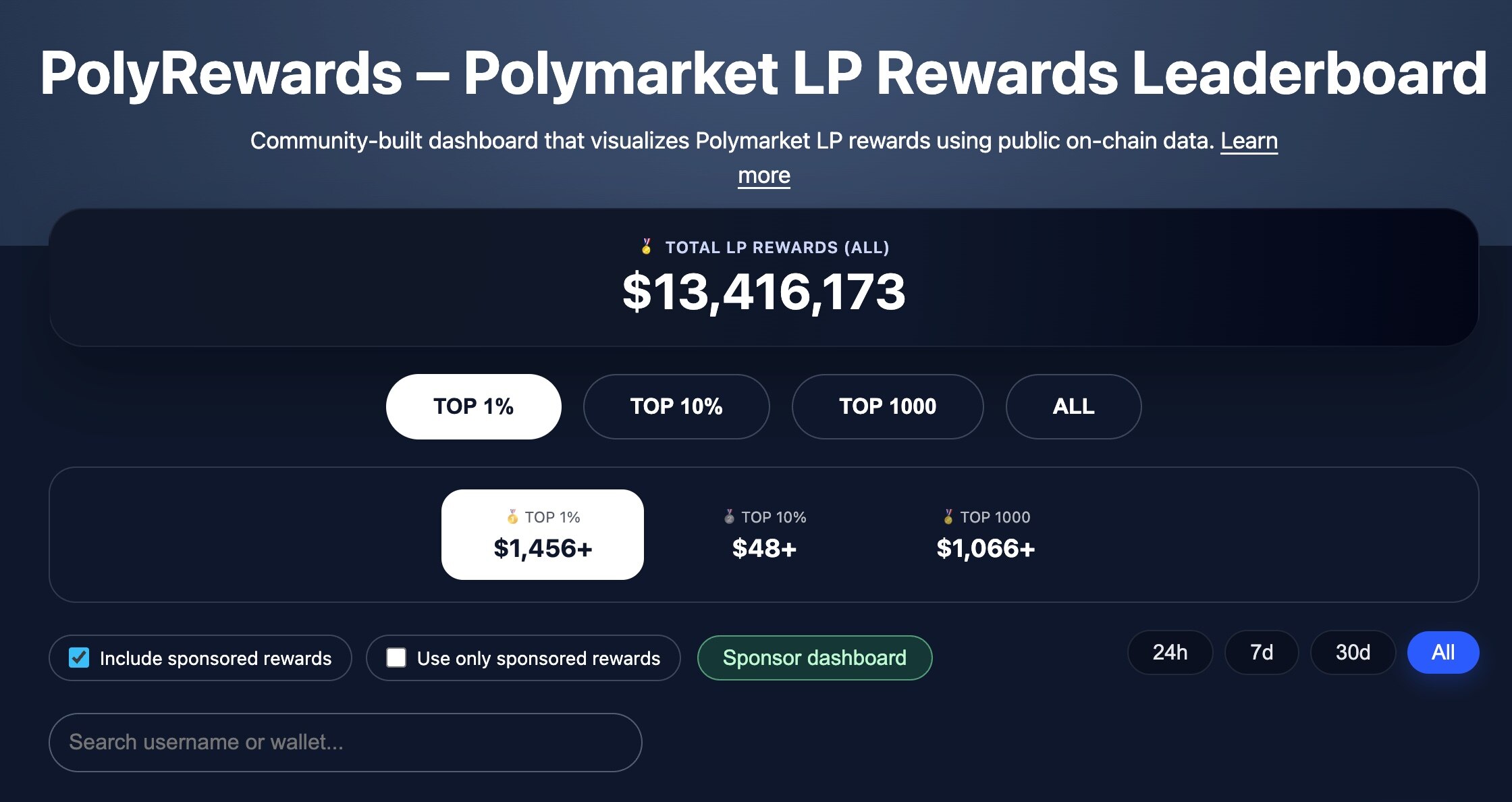

It is worth mentioning that, as a key measure for Polymarket to expand liquidity, the platform has so far distributed a total of $13.41 million in subsidies to liquidity providers (LPs). In contrast, if the data for the remainder of March can continue the performance of the first half, the fee revenue generated by Polymarket within this month alone could cover the total expenditure on liquidity subsidies.

Polymarket has largely proven the revenue-generating capability of this new form of prediction markets. Future revenue growth will mainly depend on two variables — how much more trading volume can grow, and whether fees can be further extended to more markets.

If these two variables continue to trend upwards, prediction markets might become the simplest and most direct "money printer" in the cryptocurrency industry.