Every conflict involving Trump follows the same script.

According to Xinhua News Agency, Trump spoke about the Iran conflict in Miami on the 9th: he believes the conflict will end "soon," but "not" this week. This statement sounds ambiguous, but if you've been tracking his approach to handling geopolitical conflicts, you'll recognize it as a familiar signal—negotiation terms are quietly taking shape.

This is precisely the seventh step described by The Kobeissi Letter—the emergence of conditional de-escalation signals. After the market has already begun seriously pricing in a "longer fight," conditional cooling rhetoric appears—not a retreat, but a test of whether the opponent and the market can withstand the next stage of escalation.

In a report dated March 3, The Kobeissi Letter, an independent U.S. macro market research newsletter, systematically reviewed every geopolitical and trade conflict involving Trump since his inauguration in January 2025, from tariff wars, the arrest of Venezuela's Maduro, and Greenland negotiations, to the current Iran conflict. The negotiation logic Trump follows in handling these conflicts is highly consistent.

This research compiles a complete 10-step "conflict script" for Trump's approach to conflicts: from verbal pressure and posturing, to a preference for making key moves on Friday nights, to the spread of risk premiums across stocks, bonds, and commodities, and finally ending with a "deal" that triggers violent market repricing. For the next 2 to 4 weeks, the institution outlines three scenarios, with the outcome likely still being an agreement—but before that, the market may have to endure another round of pain.

Step One to Step Three: From Verbal Pressure to the "Friday Night Surprise"

Trump's conflicts often don't start with the first missile or the first tariff notice, but with linguistic pressure to "make a deal."

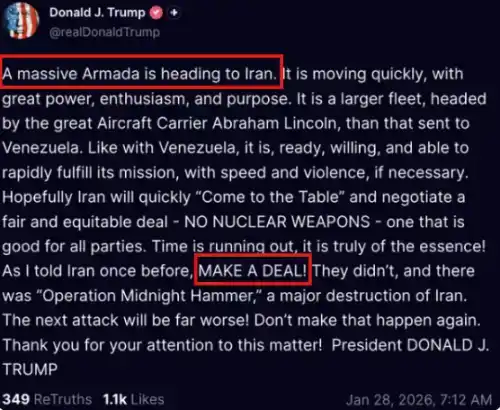

The Kobeissi Letter defines the starting point of Trump's conflict mode as verbal pressure. Taking the Iran conflict as an example, the first strike on Iranian nuclear facilities occurred on February 28, but as early as two months prior, Trump had repeatedly posted on Truth Social that "a massive fleet is heading towards Iran" and continuously urged Iran to "make a deal."

The institution points out that this pattern was equally clear in the Venezuela and EU tariff events: Trump announced the closure of Venezuelan airspace more than a month before taking action against Venezuela; before imposing tariffs on the EU, he continuously threatened Denmark and claimed it was "time" to acquire Greenland.

The second step is strategic posturing and demonstration of strength, including visible preparatory actions like military deployments and public ally coordination, aimed at enhancing credibility without triggering full-scale conflict. The institution cites Trump's meeting with Intel CEO Lip-Bu Tan in August 2025 as an example—prior to this, Trump had publicly demanded his "immediate resignation," after which both sides reached an agreement for a 10% government stake. This investment recorded over 80% paper gains in less than two months.

The third step is the signature "Friday Night Surprise." The Kobeissi Letter's statistics show that Trump's major actions are highly concentrated from Friday night to early Saturday morning, including: the June 21 U.S.-Israel joint airstrike on Iranian nuclear facilities, the September 1 strike on drug boats in the Caribbean, the October 10 threat of 100% tariffs on China, the November 29 closure of Venezuelan airspace, the December 25 military action in Nigeria, and the February 28 airstrike on Iran.

Why always act on Friday night? The report suggests that if major news breaks during trading hours, liquidity dries up instantly, algorithmic programs amplify volatility, and intraday panic intensifies. Announcing on Friday evening gives investors, institutions, and governments the entire weekend to digest the information.

More importantly, Trump is highly sensitive to severe market volatility—he needs a time window to observe market reactions and leave room for possible negotiations. According to this script, after acting on Friday night, Trump often begins hinting at the possibility of a "deal" before the Sunday futures market opens. In the case of Iran, that signal did not come.

Step Four to Step Six: How the Market Gets "Educated"

After the third step, the research divides the market's typical reaction into three layers:

Step Four: The shock occurs, but the market initially bets on a "quick deal." The report describes a common path: severe volatility occurs during the Sunday night session (18:00 EST), but by the time the Monday cash market opens, some of the moves are "reversed," as investors assume Trump loves deals and the conflict won't drag on. The research cites the March 2 movement as an example: WTI crude oil erased about 70% of its gains at one point, and the S&P 500 even turned green, but these moves were subsequently reversed, with oil hitting new highs and stocks hitting new lows.

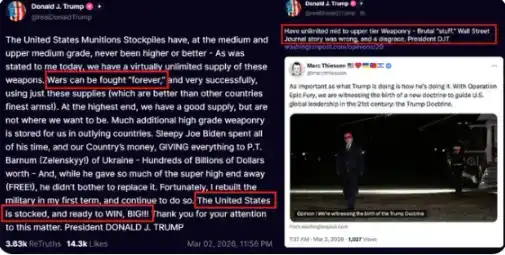

Step Five: Trump uses rhetoric like "we can fight forever" to burst the market's optimism. After investors buy the dip, the market is often hit with a counter-punch. On March 2, Trump publicly stated that "the war can go on forever" and that the U.S. has "unlimited mid-to-high-end weapons." The Kobeissi Letter believes this "forever" type of statement is more of a negotiation tactic, showing the bearable upper limit, but does not equate to a genuine desire for a prolonged war.

Step Six: The market begins formally pricing in a "longer duration." As of the report's writing on March 3, Brent crude oil prices broke above $85/barrel for the first time in nearly two years; the Dow Jones Index fell over 1100 points in a single day; stocks fell to weekly lows, and defensive capital outflows accelerated. This stage marks a structural shift in market psychology—"The first dip is bought because investors expect an agreement is coming; the second dip is bought because investors believe the escalation is temporary; the third dip is when positions begin to change structurally."

Step Seven to Step Eight: De-escalation Signals and the Market Feedback Loop

Step Seven is the emergence of conditional de-escalation signals, which corresponds to the stage of Trump's latest statement on the 9th. The Kobeissi Letter emphasizes that the time window between Step Six and Step Seven is "highly uncertain"—in the early 2025 tariff war, this transition took months, ultimately catalyzed by a rapid surge in U.S. Treasury yields before tariffs were "paused" on April 9.

The institution points out that the historical catalysts prompting Trump to back down have either been the target actively seeking to "make a deal" or a structural break in the market. On the Iran issue, this catalyst would be the collapse of the Iranian government or some event with structural implications for the U.S. and global economy.

Step Eight is the feedback loop between the market and politics. The financial market itself has become part of the negotiation environment, as oil prices, stock markets, and inflation expectations in turn influence the political narrative.

Trump has three policy priorities: being a "peace president," suppressing inflation, and lowering U.S. gasoline prices. From this, it follows that: rising oil prices, if prolonged, directly conflict with his goals, especially in a critical midterm election year.

According to JPMorgan estimates, a blockade of the Strait of Hormuz could push oil prices to $120-$130/barrel and cause U.S. CPI inflation to soar to around 5%. Based on this, the institution set three key monitoring thresholds: Brent crude sustaining above $90/barrel, a stock market decline of 5% or more, and a gasoline price increase of over 10%. "When these thresholds are breached, the probability of negotiation-related headlines appearing increases significantly."

Step Nine to Step Ten: Agreement Reached and Violent Repricing

Step Nine is agreement reached and narrative framing. The Kobeissi Letter points out that every major confrontation within Trump's framework ultimately ends with a narrative of "maximum pressure in exchange for concessions," whether it's trade deals with China, the EU, India, corporate negotiations with Intel or in the rare earths sector, or the multiple conflicts Trump helped end in 2025.

On the Iran issue, the institution believes that if the Iranian government does not collapse, the final agreement might involve a ceasefire linked to nuclear issues, a regional security arrangement with enforcement mechanisms, or a sanctions adjustment plan conditional on compliance benchmarks. "The specific architecture is far less important than the timing and narrative framework."

Step Ten is violent market repricing and declaration of political victory. The Kobeissi Letter emphasizes that market repricing after an agreement is announced is often sudden rather than gradual, because investors are generally in defensive positions by then—energy exposure is high, equity risk has been compressed, and volatility remains elevated due to latent uncertainty.

Once uncertainty dissipates abruptly, these positions are rapidly unwound. The institution cites historical cases from April, August, October 2025 and January 2026, noting that each time tariffs were paused or a framework agreement was announced, stocks surged sharply, while oil prices plummeted rapidly as expectations for the reopening of shipping channels were established.

Three Paths for the Next 2-4 Weeks: "The Deal Will Be Back on the Table"

The Kobeissi Letter outlines three scenarios for the next two to four weeks.

Scenario One: Escalation briefly intensifies, oil prices rise, stocks fall, then negotiation language suddenly appears, and the market reverses sharply due to overly defensive positioning.

Scenario Two: The conflict continues in a controlled but sustained manner, oil prices remain high without sharp spikes, stocks wait for clarity amid high volatility, and an agreement is reached under sustained pressure later this month.

Scenario Three: Regional escalation expands significantly, including substantial disruption to shipping channels or direct involvement by more state actors. Oil prices would move towards triple digits, and global risk assets face deeper repricing. Given historical precedent and the current critical midterm election year, the probability of the third scenario is low, but not impossible.

Regardless of the path, the common bet of this handbook is clear: Trump does not like "forever wars"; he is better at pushing escalation to a sufficient leverage point, then writing the ending as a "deal." The Kobeissi Letter concludes: "Don't forget, in the 13 months since Trump took office, every conflict he has been involved in has ended with a deal. Trump is a dealmaker. Follow the pattern, and you will be rewarded."