Original | Odaily Planet Daily (@OdailyChina)

Author | Ding Dang (@XiaMiPP)

On February 24, Backpack CEO Armani Ferrante announced a staking-for-equity conversion plan, where users who stake the platform's native token for at least one year will have the opportunity to convert these tokens into real company equity at a fixed ratio. The company has reserved 20% of its equity for this plan.

From this short statement, the amount of information released far exceeds that of a conventional TGE narrative.

Because, in the traditional TGE narrative, users are seen as traffic and community token holders; but in this design, Backpack attempts to upgrade users from product users to legal company owners.

The question is: Can it really work? Is this a financial innovation, or a high-risk experiment dancing on the edge of regulation? Does it change the power structure, or is it just a more advanced chip management technique? To understand this, we must return to Backpack's own historical trajectory.

Backpack: A Company Rising from the Ruins

Backpack is a "wallet + exchange" integrated platform centered on the Solana ecosystem, founded by former FTX and Alameda Research member Armani Ferrante. It was established after the collapse of FTX, emphasizing compliance and user custody.

However, unlike the development path of "first trading, then ecosystem" followed by centralized exchanges like Binance, Backpack's path is the reverse. It started with a wallet and NFTs, gradually accumulating users, community, and technical foundation, and finally launched an exchange.

Looking back at Backpack's history. In 2022, the collapse of FTX not only tore apart the credit structure of the entire crypto industry but also directly hit projects associated with it. Backpack had just completed a $20 million funding round led by FTX Ventures and Jump Crypto before FTX's collapse. But as the empire fell, approximately 80% of Backpack's operating capital evaporated. At that time, Backpack was positioned as a "wallet + xNFT operating system," aiming to provide Solana users with a safer, integrated entry point, avoiding reliance on centralized platforms.

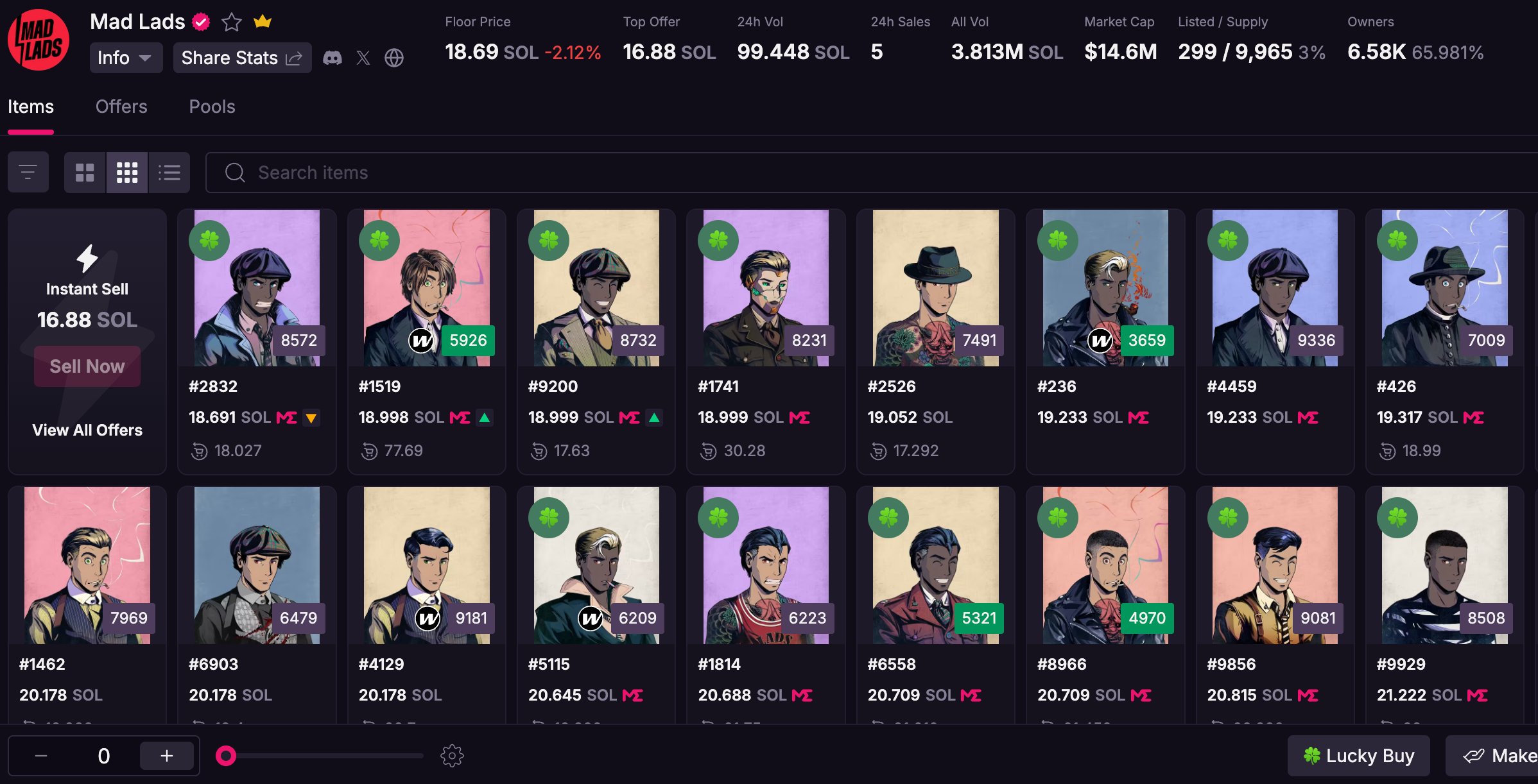

In April 2023, during the bear market trough, Backpack quietly launched the Mad Lads NFT series, with a minting cost of 6.9 SOL. It quickly became one of the top NFT communities on Solana that year, with the highest floor price reaching 229.4 SOL. Today, when the NFT trend has largely passed, the Mad Lads floor price remains at 18.8 SOL, more than double the original minting price.

In November of the same year, Backpack obtained a Dubai VARA license and launched Backpack Exchange, but it was only in a testing phase at the time. By then, it had already accumulated user trust through its wallet and NFT, and then monetized the traffic through the exchange. In February 2024, Backpack completed a $17 million Series A funding round, with a valuation of $120 million. In January 2025, it acquired FTX Europe's assets for $32.7 million, obtaining a European MiFID II license, further strengthening its compliance foundation, and committing to handle FTX EU customer claims.

Backpack was born with a silver spoon but also rebuilt from the ruins. After nearly three years, Backpack's cumulative trading volume has exceeded $400 billion, with user assets exceeding $350 million.

Now, it is about to make a bigger leap.

Token Issuance Plan and Equity Linkage

On February 17, Backpack announced the start of identity verification before TGE, the first step for users to claim tokens.

In the token economic model announced by Backpack, the total token supply is 1 billion. The pre-IPO total supply is 625 million tokens (62.5%), released in three phases:

- Phase 1 (TGE): Releases 25% of the total supply, i.e., 250 million tokens. Among them, 240 million (24%) are allocated to points holders, and 10 million (1%) are allocated to Mad Lads holders. This phase is 100% allocated to users, with no internal team share.

- Phase 2 (Pre-IPO): Accounts for 37.5%, i.e., 375 million tokens, as "growth-triggered unlocks," released gradually based on key milestones (such as regulatory approval, new product launches, and geographic expansion).

- Phase 3 (Post-IPO): Also accounts for 37.5%, i.e., 375 million tokens, deposited into company treasury, locked for one year after IPO, for the team and investors.

From its token distribution plan, we can already see that token issuance is closely tied to the IPO. Backpack is currently negotiating terms for a new $50 million funding round with a valuation of $1 billion. If calculated based on this valuation, the 20% equity is worth $200 million.

In the short history of the cryptocurrency industry, token issuance has quietly evolved from an optional financing tool to an almost "instinctive choice" and default path for almost all projects. As users, we are familiar with this method, but this goes beyond what we are familiar with.

From the perspective of the entire industry, this play fills a gap. Coinbase successfully IPOed in 2021 but never issued a native token; DeFi projects like Uniswap issued governance tokens but did not take the equity listing route. Backpack is trying a "dual-track system," where tokens are used for community incentives and equity for long-term ownership, but there is no precedent for this in the crypto industry.

Is Token Issuance + IPO Feasible?

Although this plan is bold and innovative, it faces regulatory challenges.

In the context of U.S. regulation, most tokens could be considered securities by the SEC. Once that happens, companies must comply with registration, disclosure, and anti-fraud rules. If an IPO is pursued in the future, the SEC will review the history of token issuance, structural design, and potential violation records.

More complex is that the coexistence of equity and tokens may trigger "ownership conflicts": IPO investors worry about dilution of rights (such as voting rights, dividends), while token holders expect value capture, which could be seen as "dual financing" or misleading behavior. Especially during the Gensler era from 2022 to 2024, enforcement tightened, and many projects directly abandoned IPOs.

In short, token issuance takes the fast lane of "decentralized/on-chain financing," while IPO takes the slow lane of "centralized compliance/equity financing." Backpack is trying to drive two cars at the same time, which requires extremely strong structural design and regulatory communication capabilities; otherwise, it may face listing delays or regulatory fines.

Although there is no complete precedent in the crypto industry, there are precedents. Coinbase, also a centralized exchange, completed its IPO in 2021, but they had actually considered issuing a token. Backpack co-founder Can Sun revealed in a podcast two years ago that he participated in Coinbase's listing work and helped design their token economic model. Although Coinbase ultimately chose a pure equity listing, this experience provided valuable reference for Backpack. And at that time, he had already planned to realize this unfulfilled wish at Backpack.

Can It Change the Industry?

Today, the现状 of the crypto industry is that a large number of tokens shrink by more than 80% in price one year after listing. "Listing is the peak" has almost become a curse. Backpack seems to be looking for another path: giving tokens the possibility of leading to equity, promoting a change in incentive methods.

In the past, the model we were familiar with was "earning tokens with products," where the project first creates a good product, and users earn token rewards by using it, such as fee sharing, liquidity mining, airdrops, etc. The token's value comes from the product's actual performance. Backpack's method is more like using token expectations to feed back into the company's valuation, i.e., equity binding, IPO narrative, using the expected value of tokens to quickly gather funds, community, and attention, thereby raising the company's valuation and accelerating financing and product iteration. Tokens are no longer just reward tools but valuation engines.

Of course, this transformation is full of uncertainty. How will regulation define it? How to balance rights between equity and tokens? Will the market really buy into the narrative of future shareholders? There are no ready-made answers to these questions. But in a pessimistic moment for the crypto industry, Backpack is at least trying to provide a new tension.

Backpack once rebuilt from the ruins; this time, it is building a bridge in the cracks of the system.