Written by: Tiger Research

Compiled by: AididiaoJP, Foresight News

Key Points

Different asset classes are accelerating their integration: Stocks, cryptocurrencies, and prediction markets were once independent. Today, the trend of integrating all assets on a single platform is accelerating. Robinhood has proven this model with data; Polymarket and Kalshi are moving in the same direction.

In prediction markets, collateral utilization will become a core competitive advantage: In prediction markets, collateral is locked until the outcome is determined. Polymarket's launch of perpetual futures trading is likely an effort to generate returns from idle assets.

Traditional finance is also moving toward the same integration: The new generation of users has grown up accustomed to interacting with multiple asset classes simultaneously. As generations shift, the demand for integrated platforms will only grow, and large financial institutions will gradually incorporate crypto spot trading and prediction markets as the environment opens up to regulation.

On April 21, 2026, the two leading prediction market platforms, @Polymarket and @Kalshi, announced the launch of perpetual futures trading on the same day. The trading targets are expected to include cryptocurrencies like Bitcoin, commodities like gold, and stocks like Nvidia. Both platforms stated that they will officially launch after receiving regulatory approval.

Why Now

This can be understood through the "Robinhood model." The trend of integrating previously independent asset classes into a single platform has long been underway; the announcements from Polymarket and Kalshi are merely a continuation of this trend.

Robinhood started as a stock trading app, added cryptocurrency trading in 2018, and incorporated prediction markets in 2025, pioneering the model of consolidating fragmented trading markets under one platform.

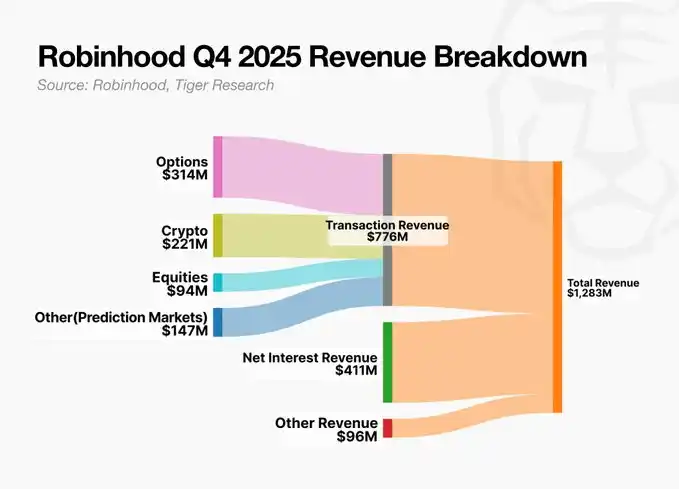

This model has been validated by data. After expanding its crypto business, crypto trading revenue became Robinhood's largest single revenue source in Q4 2024. Although crypto revenue fell 38% year-over-year in Q4 2025, total revenue remained stable, with options, stocks, and prediction markets filling the gap. A structure of resilience through diversification has taken shape.

Polymarket and Kalshi are starting from the opposite direction but heading toward the same endpoint. They originated in prediction markets and are now adding futures trading. The starting points differ, but the destination is the same. As the Robinhood model proves successful, traditional finance is likely exploring the same path.

A Simple Analogy

Smartphones integrated cameras, MP3 players, and navigation into a single device; the era of carrying separate devices for each function is over. The same transformation is happening in finance.

Brokerage accounts, crypto exchanges, and prediction markets are merging into a single platform. Robinhood started as a stock app and gradually added cryptocurrencies and prediction markets; Polymarket started with prediction markets and is now adding crypto perpetual contracts. The starting points differ, but the direction is the same.

The Generalization of the Robinhood Model

As generations shift, this trend will accelerate further. The new generation of users has grown up simultaneously exposed to stocks, cryptocurrencies, and prediction markets. Just as smartphone users would not accept separate devices for a camera, MP3 player, and map, this generation finds the idea of using separate apps for each asset class unfamiliar from the start. The demand for an integrated platform that handles all assets within a familiar interface will grow naturally with each generation.

This is the generalization of the Robinhood model.

Polymarket and Kalshi have a particular advantage in this model. Because collateral in prediction markets is locked until the outcome is determined, how to utilize these idle assets will become a key competitive differentiator.

On December 3, 2025, a developer proposed the concept of PolyAave: depositing Polymarket's outcome tokens into an Aave liquidity pool to earn interest. This was an early attempt to convert prediction market collateral into DeFi yields. Polymarket's launch of perpetual futures is likely an extension of this logic. The strategy of not letting locked capital sit idle is sound.

Polymarket and Kalshi are moving first, but traditional finance faces the same pressure. As the regulatory environment gradually opens up, large financial institutions will directly support crypto spot trading and gradually incorporate new asset classes, including prediction markets.