Original | Odaily Planet Daily(@OdailyChina)

Author|Azuma(@azuma_eth)

Recently, Robinhood (HOOD) stock has performed quite strongly, even briefly breaking back above $100 last night, although it unfortunately couldn't hold that level by the close. Personally, I remain optimistic about HOOD's future performance.

During this downtrend cycle, HOOD has been one of the few targets I have consistently been accumulating (including via rotation). So, I've been wanting to write an article about HOOD for a long time. In previous Odaily Tea Chat sessions, I briefly shared the accumulation logic. Today, taking advantage of the favorable stock price movement, I want to elaborate on it in detail. It must be stated that this is not investment advice and does not represent the platform's view; it is merely my personal thoughts when accumulating HOOD.

Multi-dimensional Analysis of Positive Factors

Regarding the reasons for HOOD's recent rise, you can find many positive explanations across different dimensions.

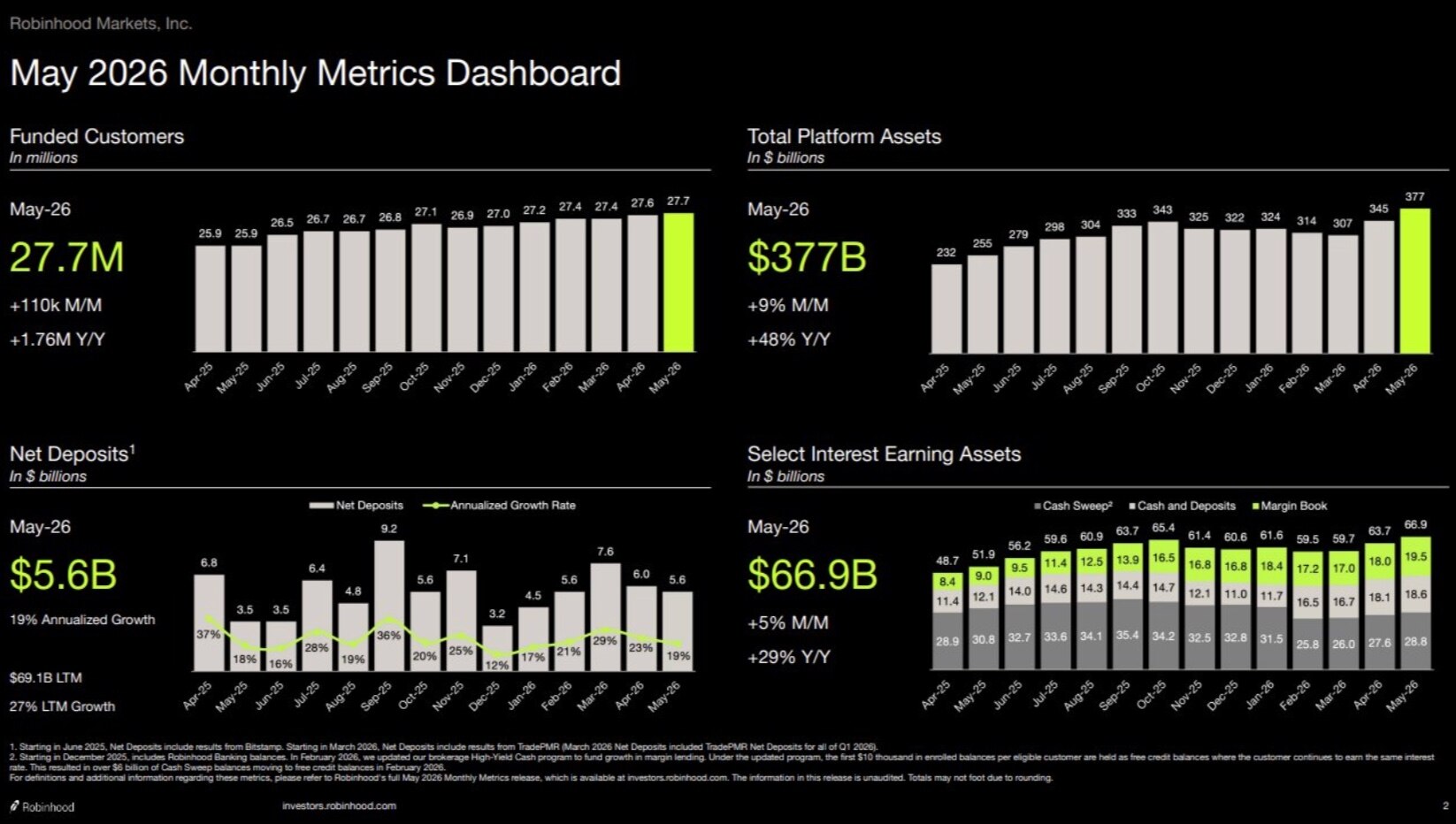

First, looking at fundamentals, Robinhood released its May operational data last week, details as follows.

- Total Assets: $377 billion, a record high;

- Funded Customers: 27.7 million, a record high;

- Margin Book: $19.5 billion, a record high;

- Event Contracts: 3.9 billion, a record high;

- Cash & Deposits: $18.6 billion, a record high;

- Options ADV: 11.6 million contracts, tying the historical record;

- Equity Volume: $315 billion, the second-highest historical point;

- Options Contracts: 231 million contracts. The second-highest historical point;

- The only "lagging" data point is Crypto Volume: $12.2 billion, ranking only 16th in historical monthly data...

Some positive factors on the news front might be more effective in stirring investor sentiment.

- First, regarding the rapidly growing prediction market, Robinhood has started intercepting Kalshi's flow by building its own prediction market, Rothera. Going forward, related revenue is expected to no longer need to be shared with Kalshi. For details, please refer to the article we published yesterday: 'The First Prediction Market Concept Stock Has Appeared!'.

- Second, regarding the IPO front, SpaceX's historic IPO brought record-breaking traffic to Robinhood. More crucially, Robinhood's brokerage and clearing arm, Robinhood Securities, was approved last week to act as an IPO underwriter. This means Robinhood is expected to play a more central role in future IPO activities (e.g., Anthropic, OpenAI).

- Third, Robinhood has been selected by the US Treasury Department to serve as the broker and initial trustee for the "Trump Account." The so-called "Trump Account" is a tax-deferred investment account plan authorized by President Trump on June 9, 2025, under the "Big and Beautiful" Act. It aims to establish government-funded savings accounts for children of US citizens born between January 1, 2025, and January 1, 2029. This means that tens of millions of newborn American children in the coming years will, by default, use Robinhood as their brokerage platform. Details can be found in 'Robinhood Gets a Batch of New Investors, the Oldest is 1, the Youngest is -3'.

There are also some more direct signals in market movements.

- Robinhood director Meyer Malka has been continuously increasing his holdings of HOOD recently. Over the past week or two, Malka has accumulated over $50 million worth of HOOD.

- Institutions have also given HOOD more positive price targets. Goldman Sachs maintains a "Buy" rating and has raised its target price from $105 to $108; Mizuho has set a target of $115; Piper Sandler is the most optimistic, giving a target price expectation of $135.

Personally, my initial main reason for accumulating HOOD was optimism about its Q2 earnings report. First, expecting a massive explosion in stock trading-related revenue this quarter under the epic US stock market conditions, and second, the potential surge in prediction market trading volume due to the World Cup, along with the revenue intercept effect of Rothera.

However, the reason for later rotating a significant portion of my holdings (mainly remaining crypto assets) into HOOD follows another logic. This is what this article truly wants to discuss.

The Altcoin Alternative

In early May, a friend asked me what I had bought recently, and I mentioned HOOD. But at that time, HOOD had just dropped from above $90 due to a disappointing Q1 earnings report (mainly due to an unexpected $100 million expense related to the "Trump Account"), and the short-term trend looked quite bad.

My friend asked why. I briefly explained the reasons above. He thought for a moment and said, unfortunately, his positions were mostly trapped, and he had little ammunition left. I asked him what he was holding; unsurprisingly, it was mostly altcoins.

I said to him at the time: "Instead of still holding onto altcoins, why not just rotate into HOOD."

The background for this judgment is that for a long time, cryptocurrency-related revenue has been a significant part of Robinhood's total revenue, and HOOD's stock price movement has been strongly correlated with cryptocurrencies. However, recently, there have been signs that Robinhood is breaking through its dependence on the crypto business and is positively decoupling from this correlation.

First, let's look at Robinhood's cryptocurrency-related revenue over the past five quarters. It's not hard to see that the overall proportion of this revenue stream is on a downward trend, and the Q1 proportion has dropped to its lowest level since 2025.

- 2025 Q1, Total Revenue $927 million, Crypto Revenue $329 million, share 35%;

- 2025 Q2, Total Revenue $989 million, Crypto Revenue $160 million, share 16%;

- 2025 Q3, Total Revenue $1.274 billion, Crypto Revenue $268 million, share 21%;

- 2025 Q4, Total Revenue $1.283 billion, Crypto Revenue $221 million, share 17%;

- 2026 Q1, Total Revenue $1.067 billion, Crypto Revenue $134 million, share 13%.

Now, look at the direct comparison between HOOD and BTC price fluctuations. Since the beginning of the year, HOOD mostly followed a similar trend to BTC, but a significant divergence has recently appeared.

Emphasizing these two points mainly aims to illustrate that the valuation logic surrounding HOOD is beginning to change. In the past, HOOD was often seen as a "shadow stock" of the crypto market, its business performance showing clear cyclicality with crypto bull and bear markets — when the crypto market skyrocketed, retail investors rushed into Robinhood to trade altcoins frantically, commission income surged, and the stock price soared; when the crypto market was sluggish and retail investors withdrew, Robinhood's revenue would quickly decline.

But now, Robinhood is no longer as highly dependent on the crypto business as before. Even if the crypto market continues its current half-dead state, its stock trading, prediction markets, Pre-IPO business, and the newly added underwriting business can still potentially support its earnings growth.

This does not mean the cryptocurrency market will no longer affect HOOD. On the contrary, if the crypto market returns to a bull market in the future, Robinhood's crypto trading revenue will likely explode again, and HOOD can still enjoy the benefits of industry growth.

In more straightforward terms: the crypto space can still affect HOOD, but HOOD no longer depends on the crypto space — if a crypto bull market returns, HOOD will still rise with it; if the crypto space remains half-dead, HOOD doesn't care.

For all those who still hold expectations for altcoins but are increasingly worried about liquidity drying up, narrative failure, and value capture problems, instead of continuing to pin hopes on some token waiting for its next narrative cycle, the current HOOD might be an option with a higher margin of safety.