Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web3_golem)

Blockchain is killing people again. Bitcoin has been falling for days, dropping over 15% in the past 24 hours at one point, quickly sliding to $60,000, down more than 40% from the October 2025 high, hitting a new low for the phase, and potentially recording its largest single-day drop since the FTX incident in 2022. Altcoins have been hit even harder, with a river of blood. (Related reading: Plunging nearly 20% in a single day, how long has it been since you saw Bitcoin at $60,000?)

Regarding the reasons behind this decline, the market mostly links it to macro-level factors, such as the "Warsh effect" triggered by the new Fed Chair Warsh taking office, the AI capital race sucking liquidity from other global assets, and the escalation of US-Iran tensions.

In addition, there have been many baseless speculations. Because this decline was so smooth, almost without pause, and lacked specific event drivers, many voices speculate whether a major institution has exploded, and a hidden black swan may surface soon. It's like watching a pile of explosives detonate without knowing who lit the fuse. According to Alternative.me data, today's crypto market Fear and Greed Index dropped to 9, in the "Extreme Fear" zone, further declining from the previous day's 12 and last week's 16. Last month, this index was still 42.

"The peak produces虚伪的拥护 (hypocritical supporters), the twilight witnesses the true believers".

The more it is this kind of moment where "analysis fails", the more one can see investors' true thoughts from their positions. While we fear the deep bear is coming, which whales in the market are selling, and who is truly buying the dip on a large scale?

Who is Selling Valuable Coins?

Vitalik and Aave Founder Sell ETH to Cash Out

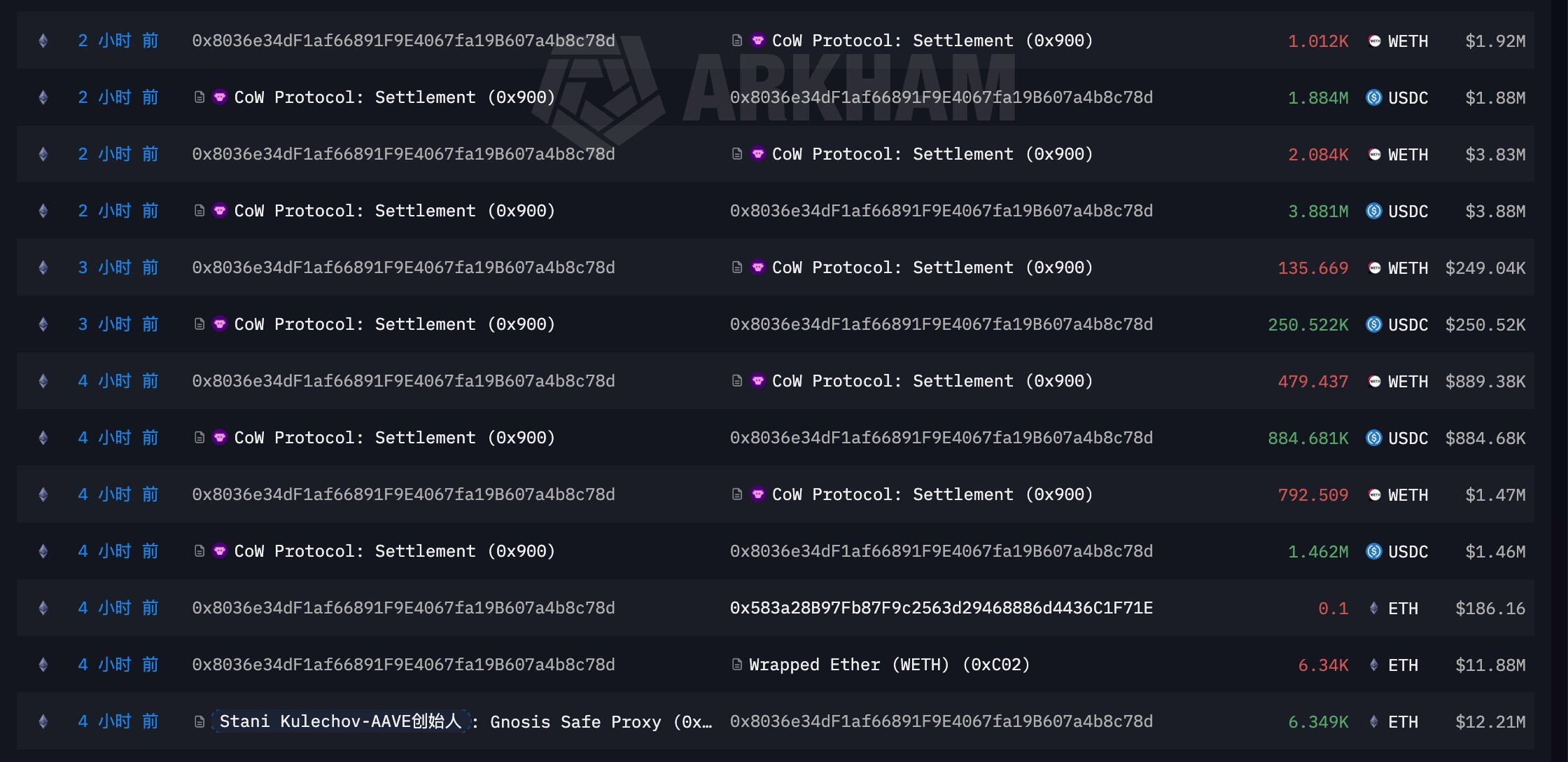

During the market drop in the early hours of February 6th, Aave founder Stani Kulechov (0x803...c78d) sold 4,504 ETH on-chain at a price of $1,855, converting it into 8.36 million USDC. ETH fell to a low of $1,747 in the early hours of February 6th.

Aave Founder Sells ETH

Besides the Aave founder, Ethereum founder Vitalik has also been frequently selling ETH recently. On January 30th, Vitalik posted that he had withdrawn 16,384 ETH for a multi-year donation plan, focusing on supporting an open, verifiable, end-to-end software and hardware technology stack to protect personal life and the public environment.

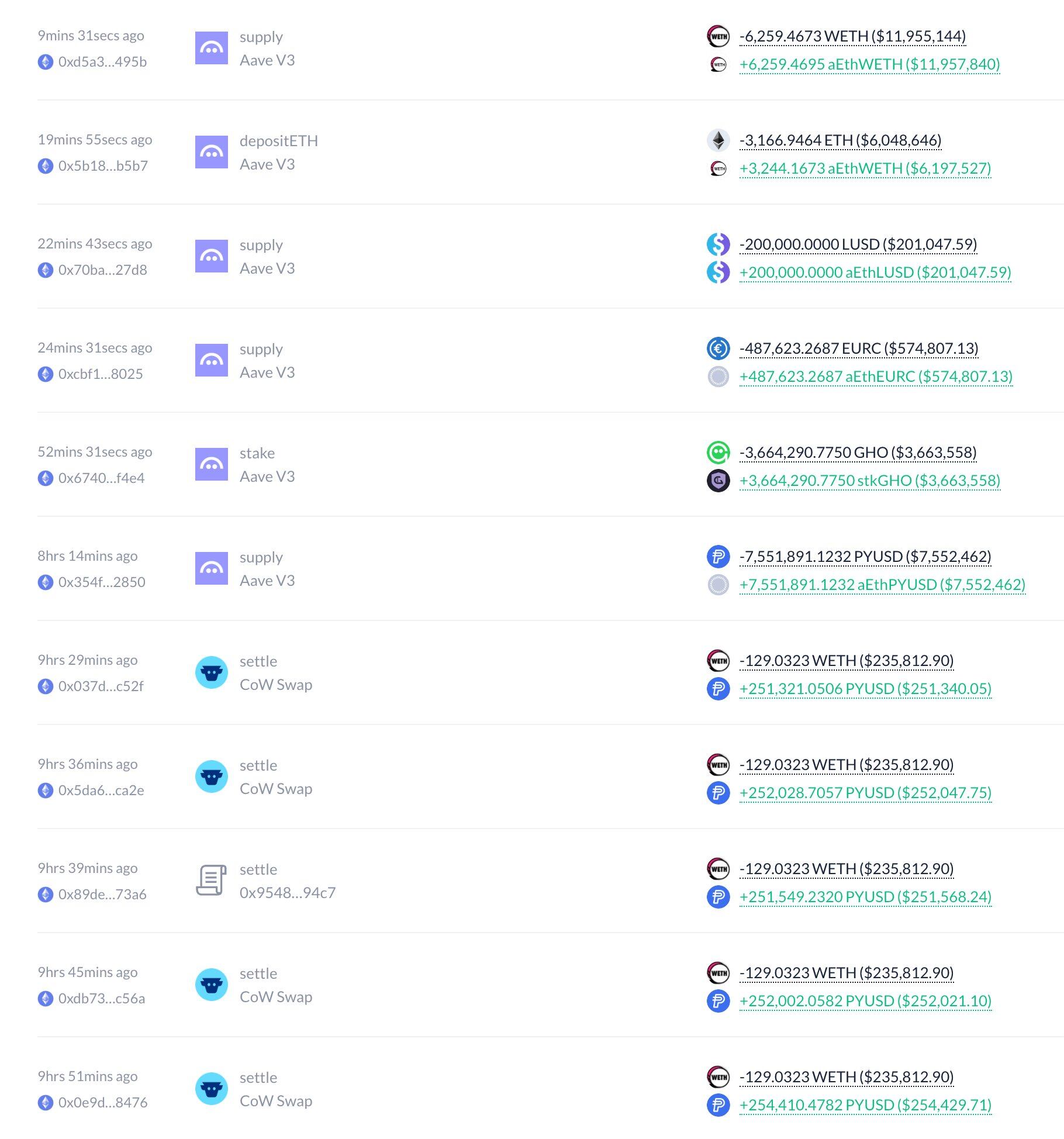

On February 3rd, Vitalik began selling these ETH, selling 493 ETH that day, worth about $1.16 million. As of February 6th, the sale progress of the 16,384 ETH planned for donation had reached 42.1%, with a cumulative sale of 6,899.5 ETH, totaling $14.15 million, at an average selling price of $2,052. However, Vitalik has deposited the remaining 9,484.5 ETH into Aave, which may mean he does not plan to sell in the short term.

"ETH Mega-Bull" Yi Lihua Falls, Sells About 250,000 ETH

Yi Lihua's Trend Research was one of the most watched ETH bulls in this cycle, and he himself often publicly sang the praises of the bull market on social media, with the community drawing the analogy "Tom Lee in the West, Yi Lihua in the East".

However, as ETH fell, Yi Lihua couldn't hold on either. On February 1st, according to monitoring, Yi Lihua's Trend Research began depositing over 10,000 ETH into Binance. On February 2nd, Yi Lihua posted on platform X admitting that he was indeed too early in being bullish on ETH, the profits from the previous top's sell-off had been wiped out, and he decided to continue waiting for the market to go up while controlling risks.

On February 3rd, he posted again, saying he still看好 (is optimistic about) the new bull market performance, expecting ETH to reach over $10,000 and BTC to exceed $200,000, but recently adjusted some positions to control risks.

This statement may have paved the way for subsequent ETH transfers. As of now, the six publicly known addresses of Trend Research hold only about 396,000 ETH. On February 1st, Trend Research publicly held 650,000 ETH, meaning they sold about 250,000 ETH, worth $554 million. Simultaneously, Yi Lihua's latest liquidation range is between $1,509 and $1,800.

But from firmly buying long to being forced to "cut losses", Yi Lihua's heart must be full of helplessness (无奈).

Whales Sold 81,068 BTC in the Past 8 Days

Besides these celebrities selling their公开 (public) positions, hidden on-chain are also纷纷 "fleeing". According to Santiment statistics, whales holding 10 to 10,000 BTC currently hold 68.04% of the total BTC supply, a new low in 9 months, having sold 81,068 BTC in just the past 8 days.

After the market fell, whales also began to stop losses and卸杠杠 (deleverage). According to monitoring, during yesterday's market drop, a certain whale deposited 10,128 ETH into Galaxy and FalconX, worth $20.44 million. A whale (0xfdd...6a92) holding an ETH lending position on Spark also began selling ETH to stop losses when the ETH price fell to $2,050. This whale累计 (cumulatively) sold 27,800 ETH, repaying $44.14 million in loans.

However, unlike the whales, retail investors are more inclined to buy the dip at this time. According to Santiment statistics, addresses holding less than 0.01 BTC, the "shrimp addresses," hold 0.249% of the total BTC supply, hitting a 20-month high, reflecting retail investors buying on the dip. But it is important to be cautious, as this combination of whale selling and retail buying has historically created bear market cycles.

Who is Silently Buying the Dip

Besides retail investors buying the dip, some faithful large holders/institutions are also buying the dip. According to statistics, after the market fell, Bitfinex margin long positions rose to about 77,100 BTC, hitting a nearly two-year high. This trend shows that there is still明显的 (obvious) leveraged funds buying the dip during the decline. Additionally, the scale of Bitfinex margin longs has grown by about 64% in the past six months,通常被视为 (often seen as) large holders or high-risk preference funds continuously adding positions during periods of market stress.

Well-known trader Eugene Ng Ah Sio also posted on his personal channel, "Buy when there's blood in the streets, even if it's your own."

"Machi" Going Long with Unlimited Bullets

The iron-headed" Machi" is a representative of large holders who go long on the dip. According to monitoring, in the early hours of February 6th, during the market decline, Brother Machi insisted on going long, depositing 250,000 USDC into Hyperliquid, opening a 25x leveraged ETH long, a 40x leveraged BTC long, a 10x leveraged HYPE long, and a 10x leveraged PUMP long. However, the BTC and PUMP long positions were quickly liquidated in the subsequent market drop. The HYPE and ETH long positions were partially liquidated before adding more.

As of now, "Machi" still holds a 25x leveraged Ethereum long position, with a position of 320 ETH, liquidation price $1,841; he also holds a 10x leveraged HYPE long position, with a position of 14,720 HYPE, liquidation price about $31.

This week, Brother Machi had 11平仓 (position closures), of which 3 were profitable and 8 were losses, with a win rate of 27.27%, and a net loss of about $286,000 for the single week. In the hyperbot弹屏 (live screen) comments, there were all voices encouraging Machi.

BTC's Eternal "Backstop" MicroStrategy: Cost Basis $76,052

Fortunately, during the market crash, the largest BTC treasury, MicroStrategy, did not choose to sell. MicroStrategy CEO Phong Le said at the MicroStrategy Q4 financial results webinar that Bitcoin would need to fall to $8,000 and stay at that level for five to six years to pose a real threat to repaying its convertible debt. This means that only then might MicroStrategy sell BTC, which is somewhat reassuring for the market.

Meanwhile, during the market decline earlier this month, MicroStrategy bought another 855 BTC for approximately $75.3 million, at a unit price of about $87,974. As of now, MicroStrategy holds

713,502 BTC, with a total acquisition cost of approximately $54.26 billion, and an average acquisition price of about $76,052. Therefore, at the current Bitcoin price of $66,000, MicroStrategy has a floating loss of over $7.168 billion.

Besides MicroStrategy firmly holding and buying, Japan's largest BTC treasury company, Metaplanet, also expressed faith in BTC on February 6th. Its CEO Simon Gerovich posted on platform X, "Regarding the recent stock price movements and the severe situation faced by shareholders, Metaplanet's strategy remains unchanged. The company will continue to accumulate BTC." But data shows that Metaplanet has not purchased BTC for three consecutive weeks.

ETH's Staunch Supporter Tom Lee: $6.6 Billion Floating Loss is Just a "Small Problem"

Just from the perspective of holding ETH, Tom Lee is显然 (clearly) more resilient than Yi Lihua. His ETH treasury company, Bitmine, not only did not sell ETH but also continued to buy during the market decline.

In the last week of January, when ETH fell to a low of $2,200, Bitmine bought 41,788 ETH that week, worth $96.55 million. Subsequently, Tom Lee said on February 2nd, "The company currently has no debt. Given the strengthening fundamentals of Ethereum, the recent market pullback is极具吸引力 (extremely attractive)", which basically indicates Tom Lee's strategy of buying the dip. On February 3rd, Bitmine bought 20,000 ETH through FalconX, worth $46.04 million.

On February 4th, in response to外界称 (external claims that) Bitmine's ETH holdings had a floating loss of up to $6.6 billion, Tom Lee responded that this was normal. But as of now, Bitmine holds 4,285,125 ETH, with an average cost basis above $3,500. With ETH falling below $2,000, Bitmine's floating loss has exceeded $8 billion.

On-Chain Whales Still Bullish on ETH

For on-chain whales, the declining market is also a rare opportunity to buy the dip. According to monitoring, a whale dormant for 7 months (3M4p1i) began buying the dip after the sharp drop in BTC on February 6th. This whale bought 482 BTC, worth $32.5 million, and currently holds a total of 1,960 BTC, worth $128 million.

Compared to BTC, on-chain whales seem to prefer ETH more. A newly created wallet withdrew 55,483 ETH from WhiteBIT in the past 2 days, worth $115.16 million.

From the evening of February 5th to February 6th, several on-chain whales/institutions also continued to buy ETH. According to Lookonchain monitoring, a wallet associated with Longling Capital withdrew 8,500 ETH from Binance on the evening of February 5th, worth $17.51 million. The whale/institution "7 Siblings" added another 6,923.85 ETH in the early hours when ETH fell below $2,000, about $13.91 million, with an average cost of $2,009.8. The current ETH holding reached 318,508.07. Meanwhile, another whale account spent 28 million USDT to buy 13,837 ETH, with an average purchase price of $2,024, but this whale wallet is also believed to可能属于 (possibly belong to) "7 Siblings".