Author: Matt Brown

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Matrix VC partner Matt Brown presents a counterintuitive argument: AI is making code increasingly cheaper, but it's making the truly hard-to-replicate elements in Fintech—banking licenses, underwriting data accumulated from credit losses, risk control models fed by real transaction volumes—more valuable than ever before.

"You can't vibe-code your way into a banking charter," a phrase that captures the core of the entire article.

This is not just a Fintech analysis; it's a map of "what moats are stronger" in the AI era.

Full Text Below:

The term "Fintech" has long relied on ambiguity arbitrage within its name.

"Fin" implies a flood of emails from .gov domains, months-long audits, compliance officers who know your SAR filing history better than you do, and weekday trips to Charlotte or Washington D.C. "Tech" implies a sleek mobile app, a 10x user experience, and discussing investments over coffee at Blue Bottle.

"Fin" and "tech" have always existed on a spectrum, but the market has typically rewarded those Fintech companies that act as much like "tech" and as little like "fin" as possible.

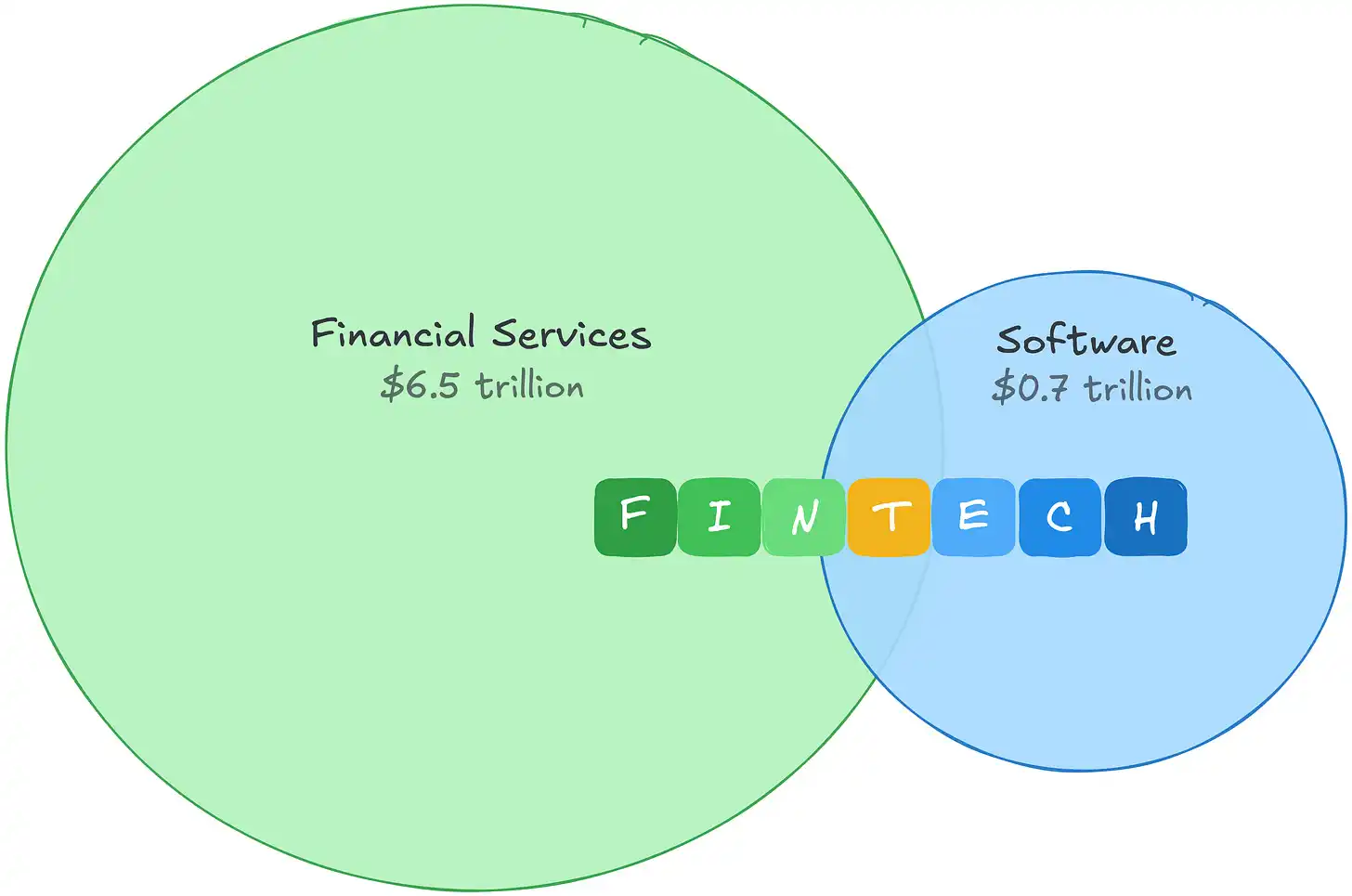

This is understandable. In 2021, the gross profit pool for software was about $0.7 trillion, commanding high premium valuations. The gross profit pool for financial services was an order of magnitude larger, yet valued much more conservatively. Fintech allowed you to arbitrage both sides: the economics of financial services, paired with the valuation multiples of software companies.

The size of this profit pool also tells you where the real money is. Financial services generate the most gross profit among global industries. The "fin" side of Fintech is not only more defensive; it's a vastly larger market.

Then AI, and the arbitrage space vanished. As investors repriced "what code is worth in a world where code is getting cheaper," software valuations compressed. Fintech companies, being categorized by the market as software companies, were caught in the crossfire.

But the market got the categorization wrong. Fintech's costs, and its moats, were never in the code, and in the face of AI-driven cost compression, they look increasingly anti-fragile.

A Tale of Two Cost Structures

Software once had one of the best business models in history: code was expensive to produce, but once written, distribution was nearly free. The gap between "expensive to build" and "free to distribute" was the margin. If you were a SaaS company spending 22 to 25% of revenue on R&D, that expenditure was also your barrier to entry. Competitors couldn't easily replicate something that took years and tens of millions of dollars to build.

AI compresses this gap from the top. If code is both cheap to build *and* cheap to distribute, margins narrow. The wall keeping competitors out gets lower, more players enter, and pricing power erodes.

If your business *is* software, this is a real problem. But Fintech's spend isn't engineering spend. Follow the money, and the difference becomes obvious quickly.

PayPal spends 9% of revenue on R&D; Block spends 12%. This isn't because Fintech engineering isn't important—Stripe's engineering capability is world-class and a real competitive advantage. It's that most of the money doesn't flow to engineering.

The money flows to the "fin". Unlike R&D spend, these costs don't just produce the product; they produce the moat:

Credit Losses Buy Underwriting Data

Affirm spends 35% of its revenue on credit losses and funding costs *before* it pays a single engineer. Every dollar lost to a bad loan is repayment data a competitor doesn't get. A new entrant training a model on synthetic data has no real benchmark. You cannot build a reliable loss history on synthetic data alone.

Compliance Spend Buys Regulatory Permission

Wise dedicates a third of its employees to compliance and financial crime prevention across 65+ regulatory licenses. Money transmitter licenses in 50 states, BSA/AML compliance programs, bank charter requirements. These aren't advantages you build; they're permissions you continually earn. You can't vibe-code your way into a banking charter.

Volume Buys Proprietary Data

Toast's Payments segment has gross margins around 22%, far below its 70% SaaS margins, but generates nearly twice the gross profit dollars. Those costs buy merchant-level transaction data, which in turn feeds Toast Capital, which has originated over $1 billion in loans. Adyen's risk models are trained on transaction patterns across 30+ markets.

Fintech Margins Were Never High, and That's the Point

Payment companies have gross margins of 20 to 50%, not 80%. But low margins don't equal a weak business. Fintech margins are low because a huge portion of the costs are generating compounding advantages. And even the costs that don't generate advantages are outside the reach of AI-driven cost compression.

AI makes every one of these moats stronger. Better models push down loss rates, better fraud detection reduces chargebacks, better compliance tools let smaller teams hold more licenses. AI doesn't replace the moat; it rewards the companies that chose to build in the hardest parts of Fintech: money movement, risk-taking, proprietary data, and regulation.

So the real argument isn't just "AI helps Fintech," but that AI is shifting value away from product surface area and towards proprietary data, risk-taking capacity, regulatory permission, and distribution embedded in real money movement. If you're building in these areas, AI is compounding in your direction. If your differentiation is in the code, AI is compounding in the opposite direction.

Demand-side growth continues, too. Every vibe-coded checkout flow is a new fraud vector, every autonomously transacting AI agent is a chargeback risk. The more that gets built on top of Fintech infrastructure, the more indispensable that infrastructure itself becomes.

"Fin" is Where You Win

This realization is already forcing smart Fintech founders to rethink their place on the "fin" vs. "tech" spectrum:

Do we take and price risk ourselves, or pass it to a counterparty and let them take the profit?

Do we own the regulatory relationship, or rent it from someone who does?

Is every transaction making our own risk model sharper, or training someone else's?

Is our ledger the source of truth for data, or an incomplete mirror of someone else's ledger?

This distinction splits the Fintech landscape in two. Companies that own the regulatory relationships, take their own credit losses, and accumulate transaction data are building moats that AI will deepen. Companies that rent the "fin"—slapping a better interface on a partner bank's charter, a BaaS provider's ledger, someone else's risk model—face the exact same problem as SaaS companies. Their differentiation was in the code, and the code just got cheaper.

The old arbitrage of applying software multiples to financial services economics is dead. The new arbitrage is simpler: own the "fin".