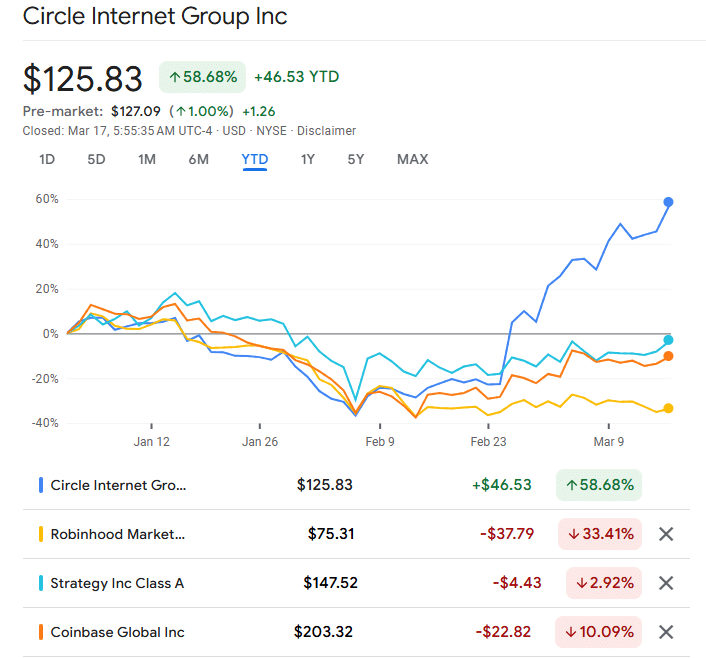

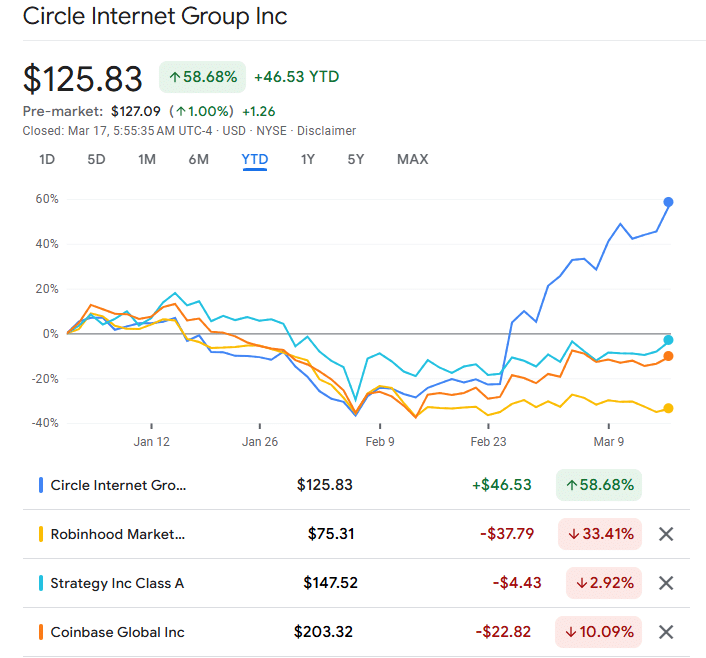

Circle Internet Group stock, CRCL, has recovered by over 150% from its February lows of $49.9 – A 2.5x pump in a month. On the 17th of March alone, the stock added an extra 9%, closing at $125.83.

Despite the remarkable bounce, the stock had fallen hard in late 2025 and early this year. After the initial IPO hype faded and the crypto rout intensified, CRCL slumped 83%, dropping from $298 to $49.

While Bitcoin’s rebound could be partly responsible for the CRCL lift-off, analysts singled out the growing adoption of Circle’s stablecoin USDC as a key driver.

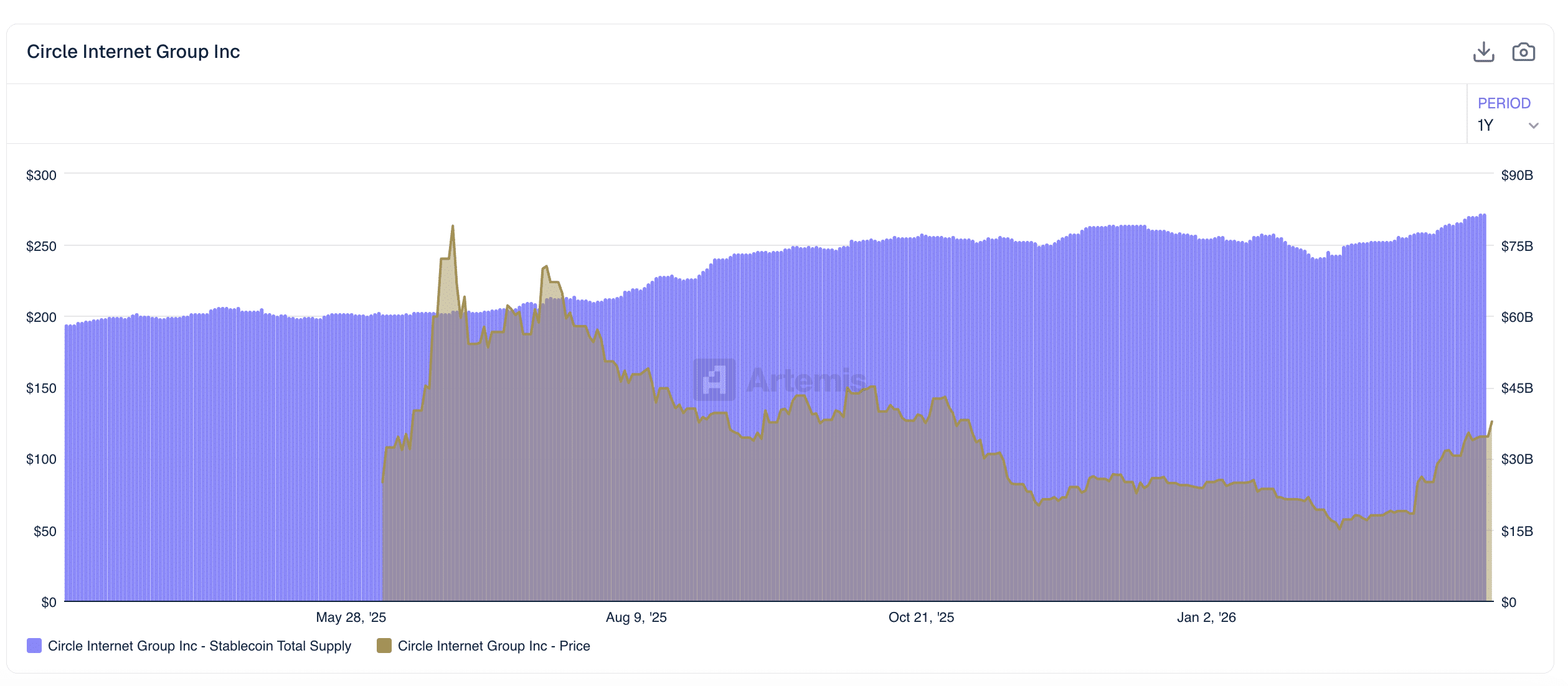

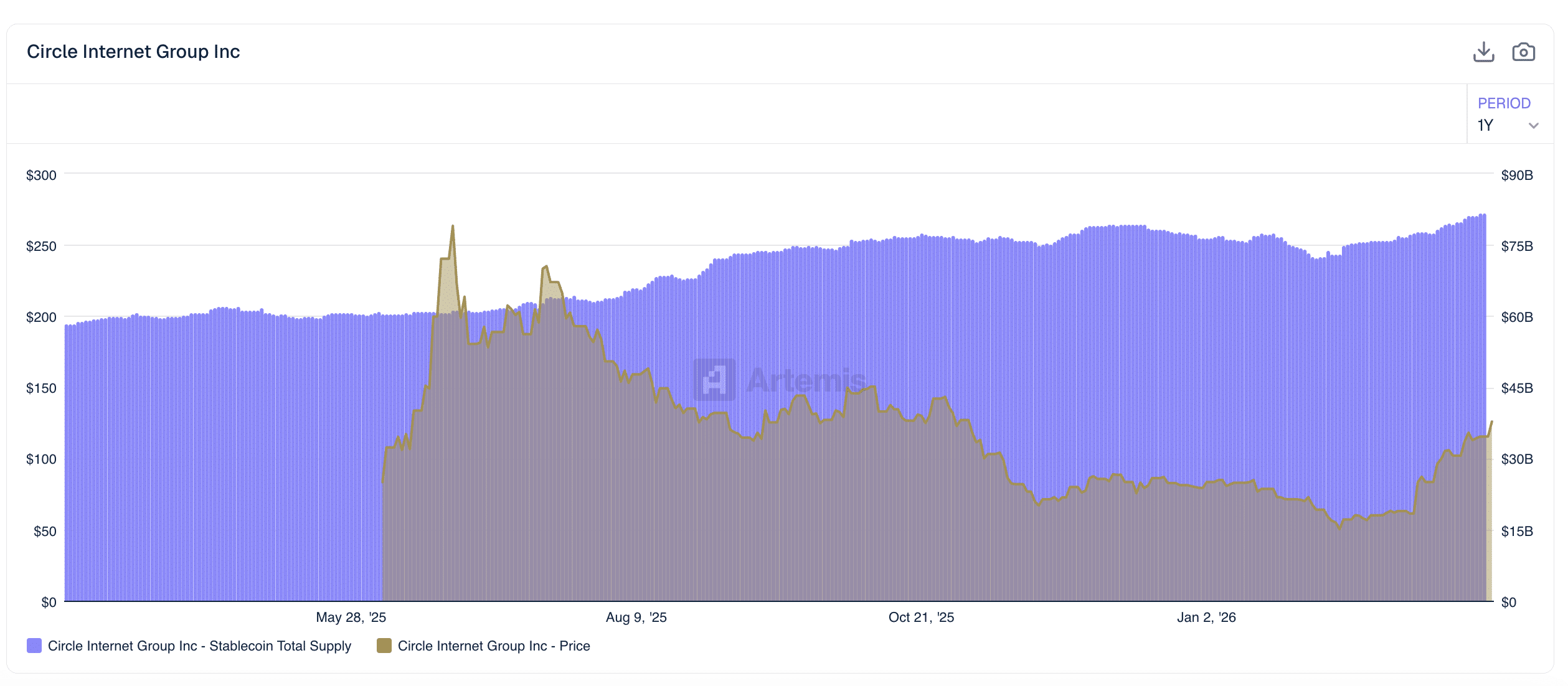

USDC supply hits record $79B

According to Jon Ma, founder of the crypto analytics platform Artemis, USDC adoption could be the greatest catalyst for CRCL’s Q1 recovery.

Noting that the $50 was an evident buy zone, Ma added,

Circle at $50/share was obvious. Stablecoin supply was $73B +25% YoY. Agentic payments were mentioned by Citrini as a winner in 2028.

During the February dip, USDC supply was about $70B. Now, its has expanded to $79B, marking a 13% increased in two months.

At the network level, over 10% of the USDC supply is concentrated in Solana [SOL]. Other trading platforms like Hyperliquid have seen 155% growth in USDC supply in the past month alone.

Interestingly, USDC’s push toward a record supply came amid a broader contraction in crypto trading. For analysts, this meant stablecoin was decoupling from the broader crypto market.

Ma’s agentic payments comment referenced a Citrini Research report that theorized that AI agents will transact on stablecoin rails and bypass traditional intermediaries by 2028.

In fact, Circle is already betting on AI agentic payment systems and the possibility that stablecoins could replace the current global foreign exchange (FX) market.

Can CRCL reclaim key levels?

Amid strong fundamentals growth, CRCL has reversed most of its late 2025 losses. Reclaiming the $125-$160 price range could effectively erase all the H2 2025 losses.

Meanwhile, the BTC recovery lifted other crypto stocks too, including Robinhood (Nasdaq: HOOD), Coinbase (Nasdaq: COIN), and Strategy (Nasdaq: MSTR). Notably, MSTR was up 14%, and COIN had recovered 22% over the past month.

But on a year-to-date (YTD) basis, Circle’s CRCL still outperformed them all. Despite the 150% upswing, the Wall Street analyst consensus rating for CRCL was a ‘HOLD’ with some projecting a price target of $145.

Final Summary

- CRCL stock has recovered by 150% from the February low of $49, reversing all Q1 2026 losses.

- Analysts cited strong USDC adoption and AI agentic payments as key catalysts behind the explosive run.