Data shows the crypto Fear & Greed Index is still inside the extreme fear territory despite the recovery that Bitcoin and other coins have made.

Bitcoin Fear & Greed Index Is Still Pointing At ‘Extreme Fear’

The “Fear & Greed Index” is an indicator created by Alternative that tells us about the average sentiment present among traders in the Bitcoin and wider cryptocurrency markets. The index takes into account for the data of the following five factors to determine the investor mentality: trading volume, market cap dominance, volatility, social media sentiment, and Google Trends.

To represent the market sentiment, the metric makes use of a numerical scale running from zero to hundred. All values on this scale that lie below 47 correspond to a net sentiment of fear, while those above 53 suggest the dominance of greed among investors. Naturally, the values lying between these two cutoffs imply a neutral mentality.

Besides these three main zones, there are also two ‘extreme’ regions called the extreme fear (25 and under) and extreme greed (above 75). Historically, these two have held significance for the market as they have been where major tops and bottoms have tended to form.

The relationship between prices and sentiment has been an inverse one, however, with tops appearing during extreme greed and bottoms alongside extreme fear.

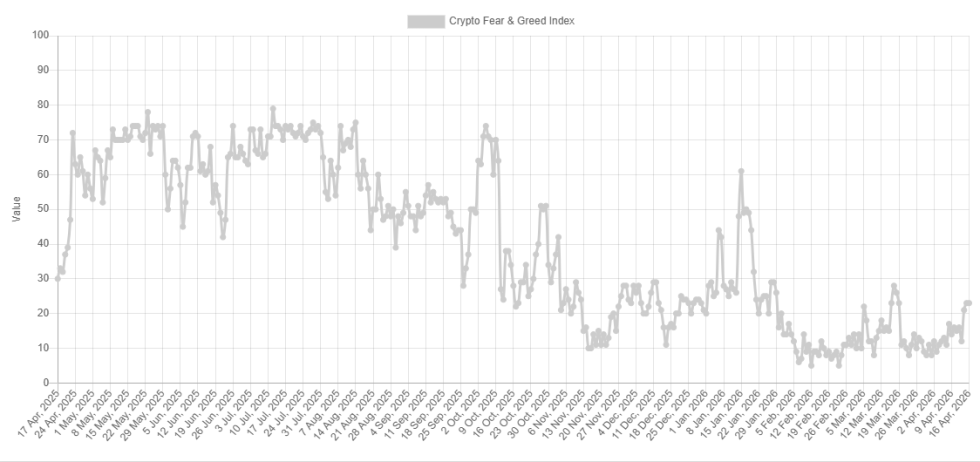

Recently, the crypto sector has been stuck in the latter of the two, as the below chart shows.

How the Fear & Greed Index has changed over the past year | Source: Alternative

The long stay in the extreme fear zone has been a consequence of the bearish action that Bitcoin and other assets have faced since Q4 2025. In mid-March, BTC’s recovery to $75,000 meant that the market saw a temporary respite from rock-bottom sentiment, with the Fear & Greed Index surging to a peak of 28. After the BTC rally fizzled out, however, the sentiment also cooled back deep into the extreme fear zone again.

From the above chart, it’s apparent that in the last few days, the metric has again made some recovery. The uplift in sentiment is due to BTC’s rally toward the $76,000 mark. Unlike the surge from mid-March, though, this one hasn’t yet been able to take the Fear & Greed Index out of the extreme fear region.

As is visible in the meter, the indicator is sitting at a value of 23 right now, which is just inside the extreme fear boundary.

The latest value of the Fear & Greed Index | Source: Alternative

It’s possible that if bull momentum continues in the coming days, the Fear & Greed Index will escape the extreme fear zone. But for now, it seems that the market isn’t convinced about the price rally.

BTC Price

At the time of writing, Bitcoin is floating around $74,800, up nearly 5% in the last seven days.

The price of the coin seems to have been moving sideways since its upward move earlier in the week | Source: BTCUSDT on TradingView