Bitcoin demand is taking a crucial turn in a market hampered by ongoing negative macroeconomic and political events across the globe. A recent report has outlined an increasing interest and demand for the leading cryptocurrency asset among large companies, which has now significantly exceeded those produced by miners in the market.

More Bitcoin Is Absorbed Than Being Mined

While price direction has been uncertain and unstable for the past few weeks, a growing imbalance is starting to take shape in the Bitcoin market. This imbalance focuses on institutions’ interests in BTC compared to new coins being mined.

On the X platform, a crypto investor known as AltCryptoGems has shared that institutional demand for BTC is rising at a substantial rate despite current unfavorable market conditions. Currently, public companies are scooping up more BTC faster than the rate at which miners are producing new coins.

As it continues to expand, this dynamic is strengthening the scarcity narrative of the flagship asset and reducing the amount of liquidity that is available. Such an imbalance could play a crucial role or act as a catalyst for the asset’s next price move. When large institutions accumulate, it is typically a clear sign of conviction in the asset’s long-term prospects.

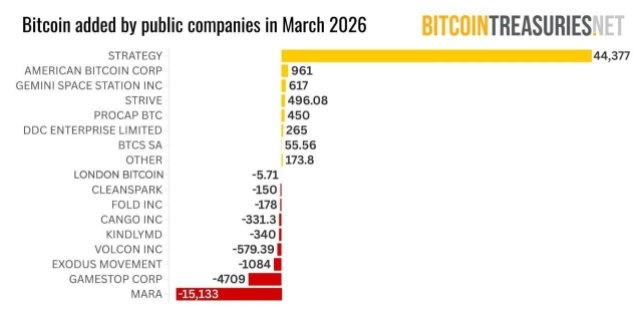

The recently concluded month of March saw a wave of accumulation from these big public firms. In the month alone, the expert revealed that these companies collectively added over 47,000 BTC valued at approximately $3.14 billion at current price levels, to their balance sheets. Leading the charge is Michael Saylor’s Strategy, amassing over 44,377 BTC out of the net acquisition.

When compared to the prior month, this is significantly higher, as it saw over 29,590 BTC being scooped up by public institutions. This shows that institutional interest and demand in BTC nearly doubled within a monthly period. As for Bitcoin mining, only 13,950 BTC were mined during the same period, indicating that demand is currently clouding new supply into the market.

BTC Exchange Balance Is Drying Up Pretty Fast

Despite persistent sideways price action and ongoing volatility, the underlying sentiment toward Bitcoin is turning quite bullish. Investors on cryptocurrency exchanges are steadily taking out their BTC from these platforms. Market expert Leon Waidmann reported that BTC balance on cryptocurrency exchanges is not sitting at its lowest level since 2018.

After a period of steady withdrawals, the total supply of BTC left on exchanges is only 14.6%. From 2019 to 2022, the balance dropped to the 16% to 18% range, and then gradually continued bleeding throughout 2022. Now, 8 years later, the percentage has dropped to 14.6% as of April 2026.

Ethereum, the second-largest cryptocurrency asset, has also witnessed a similar trend, with balances on exchanges now sitting at 11%, its lowest level in years. Both leading assets are at historic lows at the same time, making this period a crucial one for the market as it could notably shift sentiment.