This week in global markets, the main themes are Japan's interest rate hike and the Federal Reserve meeting. For risk assets, this week is destined to be anything but mild.

Three months ago, Wall Street was still discussing when rate cuts would come. Markets were willing to give the new Chairman some leeway, inflation was coming down, employment was loosening up, and rate cuts seemed only a matter of time. But the financial world is fickle; the script everyone imagined did not come to pass.

May CPI rose 4.2% year-on-year, 0.5% month-on-month. Energy prices rose 3.9% month-on-month, while core CPI remained around 2.9% year-on-year. Employment also gave the Fed no reason to turn dovish immediately. Non-farm payrolls added 172,000 in May, with the unemployment rate holding at 4.3%. This means the Fed now faces an awkward combination: inflation is reaccelerating, employment shows no significant weakness, and AI-related investment continues to support economic resilience. The case for rate cuts has weakened, while the conditions for rate hikes are gradually building.

Meanwhile, the Bank of Japan's policy meeting on June 15-16 is widely expected to deliver a 25 basis point hike as the base case. Polymarket's 'Bank of Japan Decision in June' contract shows a ~98.3% probability of a 25bp hike, ~1.45% for no change, and ~0.55% for a 50bp or more hike.

Many likely remember that Japan's previous interest rate hikes had significant impacts on the broader financial markets. This time, the market faces Japan's hike on Tuesday and the Fed's FOMC meeting on Thursday. Will the market fall?

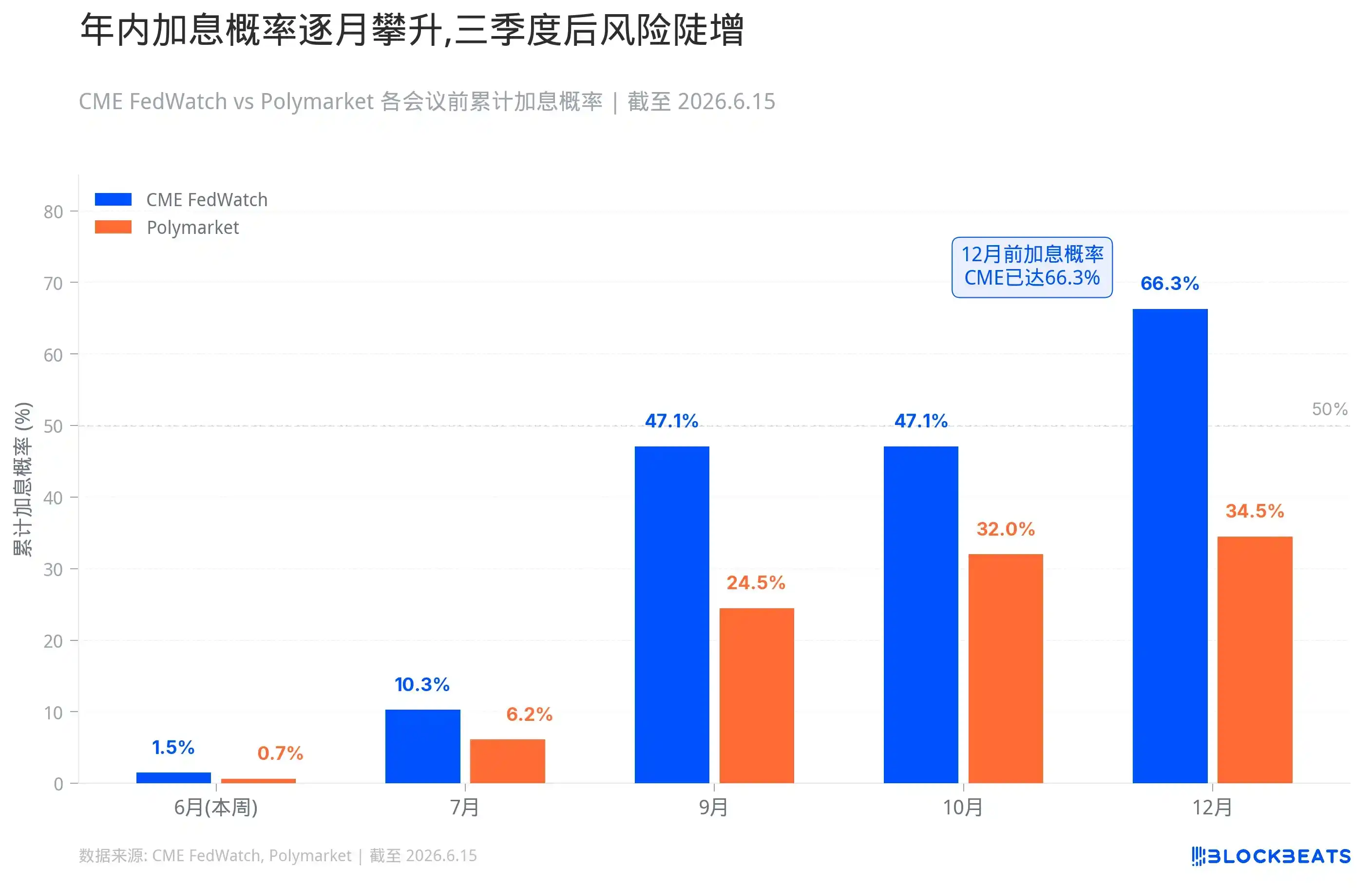

Warsh's 'Debut': Fed Rate Hike Probability Rises

First, let's look at the Fed side.

The possibility of rate cuts seems to have been almost shut off. Polymarket shows 'No rate cut in 2026' at ~70.35%, 'Rate cut before July' at ~2.35%, and 'Rate cut before December' at only ~23%. Seven out of ten people are betting on not a single cut this year. For the year-end rate range, maintaining a 3.75% upper bound is ~37%, 4.00% ~32.5%, 4.25% ~11.25%, and 4.50% and above ~3.35%. Above 4.00% combined is ~47%.

The market's judgment of Warsh is largely a consensus that in his debut, this week's FOMC meeting, he is highly unlikely to act on a hike. Hike risks are mainly concentrated after the third quarter. Several Polymarket contracts illustrate this consensus:

'Fed rate hike in 2026?' shows a ~34.5% probability of a hike at any time in 2026; 'Fed rate hike by...?' shows ~0.65% probability by June, ~6.15% by July, ~24.5% by September, ~32% by October; 'Fed Decision in July' shows ~3.15% for a 25bp hike in July, ~0.3% for 50bp or more, ~93.5% for no change; 'What will the Fed rate be at the end of 2026?' shows ~37% probability of the year-end upper bound at 3.75%, ~32.5% at 4.00%, ~11.25% at 4.25%, and ~3.35% at 4.50% or above.

Looking at more specific probabilities and data. Probability of a hike before July 29 is ~10.3%, before October 28 ~47.1%, before December 9 ~66.3%. Polymarket is more conservative, with 'Fed rate hike in 2026?' at 34.5%, before September ~24.5%, before October ~32%. This month's probability: CME FedWatch shows 98.5% for no change, Polymarket shows 99.55%.

The US is highly likely to stand pat this week, but 'not acting' is different from 'not tightening'.

If Warsh acknowledges in the press conference that inflation risks are reasserting themselves over growth concerns, if the dot plot shifts the 2026 rate median from a cutting bias to flat or even upward revisions, if the statement removes dovish 'rate cut inclination' phrasing, then the market will do the tightening for the Fed.

The first to react will be the front end of the US Treasury curve. The 2-year and 1-year yields move directly with the Fed's path. Once the market shifts from 'rate cuts later' to 'possible rate hikes later', short-end yields will rise. The US dollar will also be supported; a strong dollar itself is a form of global tightening.

Within US stocks, high-multiple growth stocks and AI/long-duration assets are most sensitive. Higher rates make future cash flows less valuable in discounted terms, financing more expensive, and the market less willing to pay premiums for unproven stories. The logic for small-caps, micro-caps, and unprofitable tech stocks is even more fragile; these companies thrive on cheap money. Once money isn't cheap, valuations are the first to collapse.

If a true tail risk event occurs—a direct Fed hike amid 98.5% 'no change' pricing—the shock would be severe. Front-end rates would jump, the dollar would surge, leveraged positions would be forced to derisk. It's not saying it will definitely happen, but the meaning of such a low probability is that if it does happen, no one would have time to react.

After all, the market has magnified the importance of Warsh's 'debut' partly because he may change the Fed's communication style. Long-time Fed watchers like Timiraos have clearly articulated the issue: for Warsh, symbolic adjustments like the dot plot, statement wording, and press conference tempo can be made quickly, but truly changing the Fed's communication framework requires long-term persuasion and internal coordination. This week's meeting could be the first step.

Across the Pacific: The 'Curse' of Japan's Rate Hikes

Now, looking at Japan. The BOJ meets June 15-16, with Polymarket pricing a 25bp hike at 98.3%. If implemented, the policy rate would rise from 0.75% to 1%, the highest since 1995.

The logic pushing Japan to this point is straightforward. Middle East conflicts push up oil prices; Japan is a typical energy importer, and a weak yen amplifies import costs. Wages are rising, service prices are rising, inflation expectations are shifting. Maintaining low rates would raise doubts about whether the BOJ still cares about controlling inflation.

The hike itself is no surprise, but a crucial concern is: over the past few years, massive global funds borrowed cheap yen, converted to US dollars or other high-yielding assets, buying US Treasuries, stocks, credit—some indirectly flowing into high-volatility risk assets. This structure is built on one premise: Japanese interest rates are low enough, yen funding is cheap enough, and the central bank is slow enough. In other words, if the market believes Japan's interest rate normalization is continuous, the carry trade becomes fragile, yen shorts get squeezed, and global leveraged funds begin to contract.

The market's fear of a BOJ hike is not unfounded. Over the past two decades, almost every time the BOJ tried to lift rates from near zero, global markets ran into trouble.

The first was August 2000. The BOJ raised rates from zero to 0.25%, coinciding perfectly with the peak of the US dot-com bubble. Within three months of the hike, the Nasdaq fell 35%. Japan's own economy couldn't withstand it, quickly sliding back into recession, forcing the BOJ to cut rates back to zero in 2001.

The second was 2006 to 2007. The BOJ raised rates to 0.5% in two steps: first in July 2006, then in February 2007. The timeline almost perfectly matches the incubation period of the US subprime crisis. In the summer of 2007, US subprime mortgages began to implode; in 2008, Lehman Brothers collapsed, triggering the global financial crisis. The BOJ was forced to cut rates back to zero once again.

The third was July 31, 2024. The BOJ raised rates from 0% to 0.25%, a small move, but the market reaction was extreme. On August 5, the Nikkei 225 plunged 12.4% in a single day, its biggest drop since Black Monday in 1987. South Korea's KOSPI triggered circuit breakers; the Nasdaq and S&P 500 fell 3.4% and 3% respectively. The VIX fear index surged above 65. The transmission mechanism of that crash was clear: the BOJ hike triggered a sharp yen rally, forcing unwinding of carry trades that borrowed yen to buy foreign assets—selling stocks to repay yen, leading to collective selling and a stampede. To meet margin calls, fund managers even sold 'safe-haven assets' like gold and BTC. In the liquidity crisis, correlations among all assets approached 1. I still vividly remember the market carnage that day.

Therefore, what's more important is what signals the Japanese government will provide at tomorrow's press conference: how high will rates ultimately go?

US Stocks, US Treasuries, Bitcoin: Which is Most at Risk This Week?

As mentioned earlier, global markets mostly declined during the BOJ's past three hiking cycles.

But the BOJ hike itself doesn't necessarily crash the market; crashes usually occur when other fragile leverage exists. For instance, 2000 and 2007 coincided with larger bubbles elsewhere. August 2024 was due to a surprise move and overly heavy market positioning leaving no time to react. Subsequent hikes, with preparation, passed without incident.

This time, a 25bp move is priced at 98.3%, leaving almost no room for surprise. Based on the experience of December 2024 and January 2025, the hike itself will likely be digested smoothly. But this time, there are two additional variables.

First, Governor Ueda was hospitalized with an infectious liver cyst and is expected to miss this meeting and the post-meeting press conference. According to public reports, Deputy Governor Himino Ryo will serve as acting chair for the meeting, and Deputy Governor Uchida Shinichi will host the post-meeting press conference. This arrangement is unlikely to change the hiking direction. However, the market is less familiar with Uchida's communication style than Ueda's, potentially amplifying volatility in interpreting his wording. Phrases like 'will judge future moves based on data' versus 'there is still room for normalization' may seem similar but send completely different signals to traders.

Second, the US meets in the same week. The BOJ meeting and the FOMC are only one day apart. If the market reacts mildly to the BOJ hike but Warsh turns hawkish in his press conference the next day, the two layers of pressure could compound. Conversely, if the market is already tense after the BOJ move and Warsh adds fuel to the fire, short-term sentiment could overreact. Having two central banks deliver results back-to-back, this scheduling itself amplifies volatility.

Let's analyze asset by asset:

US Treasuries will likely react first this week. Front-end yields move directly with the Fed's path, with the 2-year and 1-year being most sensitive. If Warsh's press conference is hawkish or the dot plot is revised upward, front-end yields will rise, reflecting the market's repricing of 'later cuts' or even 'a hike this year'. The long end is more complex; the 10-year yield may not rise in sync. If the market begins to worry high rates will hurt the economy, the yield curve could flatten further or deepen its inversion. On the Japan side, if Uchida hints at further hikes, Japanese government bond yields will also be pushed up. Marginal adjustments to Japan's $1.13 trillion US Treasury holdings could, in turn, impact supply and demand in the US Treasury market.

The US dollar will likely find support. A hawkish Fed tilt boosts expectations for US dollar asset yields, strengthening the DXY. A BOJ hike is theoretically positive for the yen and negative for the dollar, but the actual direction depends on the tone: if the BOJ follows the hike with dovish signals, the yen may not rise but could fall, making the dollar index even stronger. With two central banks meeting in the same week, the relative movement of the USD/JPY will be highly sensitive, and forex market volatility will likely increase. Asian and emerging market currencies will face pressure; a strong dollar itself is a form of global tightening, sucking dollar liquidity from abroad.

US stocks will show clear divergence. High-multiple growth stocks, AI/long-duration assets, small-caps, micro-caps, and unprofitable tech stocks are most vulnerable. Higher rates make distant cash flows less valuable, financing more expensive, reducing willingness to pay premiums for unproven stories. The Russell 2000 and companies reliant on cheap money will be the first hit. Bank stocks will have a complex reaction; short-term net interest margins may benefit, but if the curve inverts further and credit risks rise, it may not be positive. Defensive stocks may hold up relatively better, but 'bond-like assets' like utilities and REITs will also see valuation pressure from higher rates. The S&P 500 closed near 7382 last Friday, and the Nikkei 225 was around 66078. If both central banks lean hawkish this week, both US and Japanese stocks will face pressure, especially indices heavy with tech.

Japanese stocks are in a special position. A BOJ hike itself is negative for Japanese exporters, as a stronger yen erodes overseas profits. But if the hike magnitude and pace are within expectations, Japanese stocks may not fall sharply, as shown by the experiences of December 2024 and January 2025. The real risk lies in the post-meeting communication; if Uchida hints at further normalization, the Nikkei may fall first and then reassess.

Gold will be pulled by two forces. Rising real rates and a stronger dollar are typically negative for gold. But if the hikes are driven by energy shocks, geopolitical risks, and runaway inflation, safe-haven demand will support prices. Gold will likely trade in a high range this week, with direction depending on what the market fears more: higher rates or uncontrolled inflation. Crude oil depends more on supply/demand and geopolitics; Iran tensions persist. If hikes are due to oil-driven inflation, oil may not fall immediately. But if the market starts pricing in demand slowdown expectations, industrial metals and oil will face pressure later.

Credit and real estate are slower-moving but the direction is clear. High-yield bond spreads will widen, financing costs will rise, and commercial real estate, REITs, and mortgage-sensitive assets will face pressure. Emerging markets with high US dollar debt will also suffer more, with increased capital outflow pressure.

Crypto markets also face pressure in this macro backdrop. BTC is currently around $65,000. In early June, it was at $72,000, then fell to around $61,500 after the CPI report, rebounding only in recent days. This level is inherently unstable. When it broke below $62,000 on June 5, over $1.5 billion in long positions were liquidated on-chain, and Bitcoin spot ETFs saw $2.7 billion in net outflows over a single week. Although the price has recovered somewhat, the positioning structure is not healthy. BTC has some macro asset attributes; it may not necessarily crash with rising rates, but it's also unlikely to rally independently. ETH, SOL, altcoins, memecoins, and small-cap coins are more vulnerable. These assets feed on liquidity spillovers and risk appetite. Once the market starts comparing the appeal of cash, short-term bonds, and money market fund yields again, high-beta assets are the first to be cut. Contract funding rates have declined, and on-chain risk appetite has cooled, as seen in early June.