Original Author: Four Pillars

Original Compilation: AididiaoJP, Foresight News

Key Points

Completed a $328 million buyback in eight months using 99.5% of daily protocol revenue. Two independent data aggregators, despite not being interconnected, reached the same conclusion. To manipulate the data, one would need to simultaneously deceive DeFiLlama, maintain a stable 68-69% ratio with Adam_tech's Dune data (which only indexes Solana), and have 105.17 billion PUMP tokens in verifiable wallets as support.

The "dilution curve" in August 2026 is actually a supply replacement rather than an addition. At current revenue levels, the buyback can absorb twice the new supply. Community emissions will cease when team and investor unlocks begin. Monthly emissions will drop from 10 billion tokens to 9.2 billion tokens.

The real reasons for the current suppressed valuation multiples are: industry classification (the nature of "original sin stocks"), trust foundation (anonymous team, discretionary buybacks), and capital flow (insiders allegedly using buybacks to sell).

1. Proof of the $328 Million Buyback

Rumors of Pump.fun's fabricated revenue have been circulating on Twitter. The following analysis shows these rumors are false.

As of March 15, 2026, data from fees.pump.fun shows a cumulative buyback amount of $328 million. This means 2,283,518 SOL was used to purchase 104.5 billion PUMP, accounting for 10.45% of the total supply and offsetting 29.52% of the circulating supply. Over eight months, the daily buyback amount remained between 99.5% and 100.5% of protocol revenue, averaging $1.25 million per day as of February 2026. Fabricating revenue would require massive capital support: for every dollar bought back, one dollar of SOL flows out from a verifiable wallet to purchase tokens stored in an auditable address. To fake $328 million in revenue, one would need to actually spend $328 million.

The relevant tokens are stored on-chain and can be verified (as of March 17, wallet G8CcfRff holds 103.96 billion PUMP, 8PSmqJy6 holds 1.21 billion PUMP, totaling 105.17 billion). The initial execution wallet 3vkpy5Y (marked as "Pump Buy Back" on Solscan) completed transfers to the holding wallets and was rotated in August 2025, now with a zero balance.

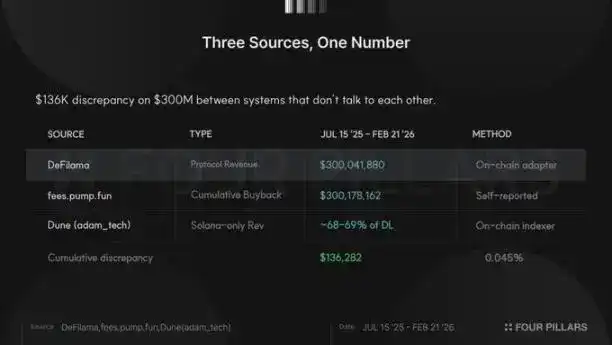

DeFiLlama recorded total protocol revenue from July 15, 2025, to February 21, 2026, as $300,041,880. During the same period, the cumulative buyback amount on fees.pump.fun was $300,178,162. The match is 100.05%, with only a $136,000 difference between two independent systems on a total of $300 million.

Adam_tech's Dune dashboard provides a third layer of verification. This platform only tracks Solana chain revenue, consistently representing 68-69% of DeFiLlama's multi-chain data, as it does not index Padre revenue launched on Base, Ethereum, and BNB Chain in October 2025. This ratio remains stable daily, indicating both are independently reading the same on-chain events.

Before the launch of PumpSwap in March 2025, the error margin between the three data sources was within 1-5%. After PumpSwap launched, the data differentiated into three layers: total fees, protocol revenue, and Solana-only revenue. If someone were to fabricate revenue data, they would need to simultaneously deceive two independent on-chain indexers, maintain stable cross-correlation ratios through three product changes, keep a multi-chain revenue split ratio consistent with actual business expansion, and support it with token purchases in verifiable wallets.

2. Four Statistical Tests

In addition to on-chain evidence, 747 days of fee data can be subjected to four standard tests to verify the authenticity of the financial data. While a single test is not conclusive, when four tests point to the same conclusion, credibility increases significantly.

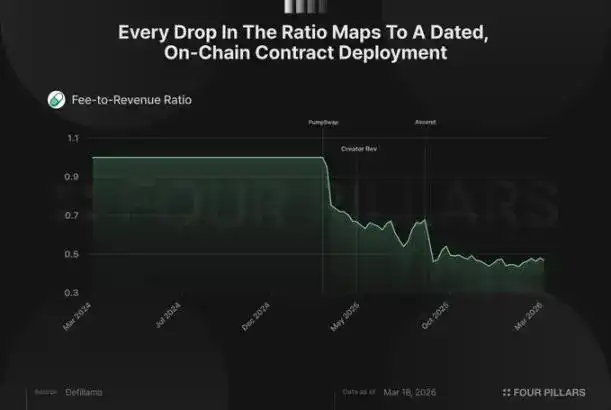

The first test is the fee-to-revenue ratio, the hardest indicator to fake. Pump.fun collects fees from each bonding curve transaction, but not all count as protocol revenue; some go to LPs, creators, and referral rewards. In the dataset, the total fee to net revenue ratio dropped from 1.0 to about 0.48, but not gradually. It dropped sharply in three stages, each corresponding to a documented on-chain product change:

- March 20, 2025: PumpSwap launched with an LP fee split mechanism, ratio dropped from 1.00 to 0.70 in two days.

- May 13, 2025: Creator revenue sharing mechanism launched, ratio dropped from 0.69 to 0.56.

- September 2-3, 2025: The Ascend project introduced a dynamic fee mechanism, layered pricing allowing creators to get up to 0.95% fees on low-market-cap tokens, with the protocol keeping only 0.05%, ratio dropped from 0.68 to 0.46.

Faking this data would require simulating fee and revenue series undergoing three structural adjustments simultaneously, with the daily ratio fluctuating between 0.40 and 0.55 based on token tier composition. This complexity makes fabrication difficult. The reality is that product iterations naturally caused the changes, not artificial construction aligning with contract deployment times.

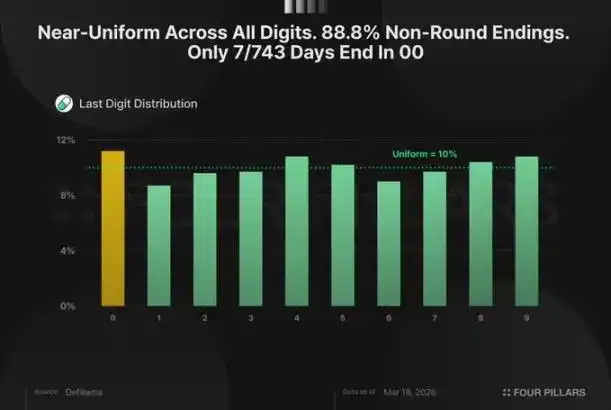

The second test examines continuity and digit distribution, aiming to determine if the data shows signs of manual entry. Humans struggle to generate truly random sequences, tend to avoid long streaks, prefer integers, and have unconscious biases toward specific digits. Pump.fun data lacks these characteristics:

The longest consecutive rise or fall is 6 days, with an average streak length of 1.92 days, consistent with expectations for a natural process with moderate momentum. Streak length decreases geometrically: 185 one-day streaks, 111 two-day streaks, 52 three-day streaks, down to 7 six-day streaks.

The last digit of daily fees is nearly uniformly distributed between 0-9, with each digit accounting for 8.7%-11.2%. 88.8% of days do not end with an integer; only 7 out of 743 non-zero days end with 00 or 000.

The third test examines the weekend effect. Pump.fun is a retail platform; users issue tokens more on weekdays than weekends. Average daily fees are $2.14 million on weekdays and $1.81 million on weekends, a consistent ~18% drop, appearing week after week in the two-year data. A Mann-Whitney test shows a p-value of 0.003, statistically significant. If data were fabricated, one would need to deliberately keep weekends consistently lower, increasing the complexity and risk of detection.

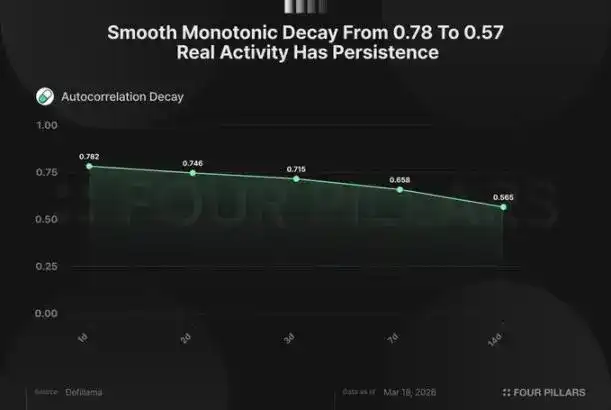

The final test examines autocorrelation, measuring the relationship between today's revenue and tomorrow's. Pump.fun's first-order lag autocorrelation is 0.78, meaning today's fees are 78% correlated with yesterday's; it remains 0.65 after one week (lag 7 days); and 0.57 after two weeks (lag 14 days). This slow, smooth decay reflects the momentum characteristic of organic platform activity: active periods cluster, and downturns persist. If daily revenue were generated randomly, correlation between adjacent days would be near zero, and the data would jump like noise rather than flow like a market. Faking high autocorrelation for a single lag is not difficult, but faking the entire decay structure (monotonically decreasing step by step for each lag), while maintaining the weekend effect, streak characteristics, and realistic digit distribution, is nearly impossible.

Four independent tests, four consistent conclusions, three data sources corroborating each other. The revenue data is authentic and reliable.

3. Analysis of Remaining Valuation Discount Factors

Rumors of fabricated revenue are one reason for PUMP's current suppressed valuation. The previous analysis has clarified this. But the token still trades at a discount; other suppressing factors and their validity need exploration.

First, analyze the August team unlock. Community emissions are 10 billion tokens monthly, will reach 240 billion tokens by July and then stop, coinciding with the start of team and investor unlocks, totaling 9.2 billion tokens monthly. Monthly emissions will drop from 10 billion to 9.2 billion tokens, an 8% decrease in inflation rate. At the current average daily revenue of $1.25 million, the monthly average buyback is $38 million. At a price of $0.0021 per token, this can absorb about twice the $19 million worth of new monthly supply. After August, emissions decrease while buybacks continue, further improving this ratio.

Revenue shows no sign of decline either. Over fourteen months, monthly average fees fluctuated between $2.3 million and $4.8 million daily: down 49% in July 2025, rebounded 94% in August, surged 72% in September, and jumped 45% in January 2026. Overall, it mean-reverts around a daily average of $2.5-3 million, with weekly trading volume stable at $640-700 million. The so-called "Q3 to Q1 decline" is a one-sided conclusion drawn by selectively picking September peak data.

The remaining suppressing factors are as follows:

The "original sin stock" discount is the most persistent. Solidus Labs found that 98.6% of tokens on the platform have "rug pull" characteristics. This finding had the intended effect: regardless of revenue, institutional allocators will not include a "meme coin casino" in their portfolios. This is a persistent structural factor, completely unrelated to revenue quality.

Source: Solidus Labs

Alleged insider selling constitutes tangible recent pressure. Wallet 77DsB received 3.75 billion PUMP in July 2025 from an address marked "Token Custody Wallet" on Solscan, allegedly liquidated its position for 8.02 million USDC between February 16 and 22, 2026. Wallet GpCfm transferred 1.21 billion PUMP ($2.57 million) to Bitget during the same period. A third wallet deposited 1.757 billion PUMP ($3.54 million) into Bitget on March 6. Although no source confirms actual ownership, at least $14 million flowed to exchanges at a market price of $0.002 within thirty days while the protocol was buying back, compared to a private round price of $0.004. This situation raises questions, regardless of the wallet owners' identities.

The trust aspect is the hardest to price. The founders are anonymous (co-founder Dylan has a "rug pull" record from 2017); buybacks are explicitly "discretionary" ("pump.fun may modify or中止 the plan at any time"); Bubblemaps once alleged Hayden Davis was associated with a $50 million private placement, but later deleted the claim after co-founder Alon called it "defamation." On-chain associations exist, but attribution is disputed and unverified.

None of these factors relate to business fundamentals. The revenue is real, supported by data, and the unlock arrangement is favorable to holders. The "original sin stock" label, anonymous founders, and insider fund flows are all trust discounts applied to a protocol with $1.25 million in daily verifiable on-chain revenue, whose buybacks can absorb twice the new supply. The trust discount will eventually narrow; revenue of this scale will not be mispriced forever.