Author: Deep Tide TechFlow

On May 24, a tweet about Hyperliquid Strategies(NASDAQ: PURR) sparked considerable discussion in the English Crypto Twitter (CT) space:

This company used approximately $220 million to buy HYPE, and its current unrealized profit has neared $1 billion, even surpassing the profit efficiency of Michael Saylor's Strategy (formerly MicroStrategy) on BTC.

This topic is now gradually spreading to the Chinese-speaking community. HYPE recently hit a new all-time high above $62, with a year-to-date increase of over 150%, making it one of the strongest-performing mainstream crypto assets this year.

As the only listed company proxy for HYPE, PURR has also risen over 100% year-to-date, naturally becoming a target of FOMO during US stock research.

However, before following the trend, several questions need to be clarified:

1. What exactly is this company?

2. What's the difference between investing in it and directly buying HYPE?

3. Does the claim that its "capital efficiency exceeds MicroStrategy" hold up under scrutiny?

$PURR, a Pure DAT

First, the conclusion: PURR is not a company with actual operations; it's essentially a pure stock-wrapped product for $HYPE.

Its business model can be summarized in one sentence: buy HYPE, stake HYPE, hold HYPE. As of April 2026, public information shows the company holds approximately 20.8 million HYPE tokens, with about $114 million in cash and zero debt.

This means the entire value of this stock depends on one thing: the price of HYPE.

Since there is no business to analyze, evaluating such a company comes down to two dimensions: the underlying asset itself, and who is operating this shell.

The latter determines capital operation capabilities—such as when to issue shares to buy more tokens, when to buy back shares to support the price, how to manage the premium/discount between the stock price and net asset value... This also influences whether institutional capital is willing to enter through this vehicle.

Historically, PURR's predecessor was Sonnet BioTherapeutics, a small biotech company listed on NASDAQ. In July 2025, it announced a merger with Rorschach I, completed the transaction in December of the same year, with an overall valuation of $888 million, renamed Hyperliquid Strategies, and ticker changed to PURR.

Notably, the initiators of this transaction were Paradigm and Atlas Merchant Capital.

Paradigm is one of the top-tier venture capital firms in the crypto industry, having invested in projects like Uniswap, Blur, Friend.tech, and has deep involvement in the Hyperliquid ecosystem, directly participating in the formation of this SPAC.

Atlas Merchant Capital is a financial services investment firm based in New York and London. Its two founders took key positions at PURR: Chairman Bob Diamond is the former CEO of Barclays, and CEO David Schamis is a former partner at JC Flowers.

The board also includes former Boston Fed President Eric Rosengren and former NYSE COO Larry Leibowitz. Other participants include Galaxy, D1, and Pantera, all leading institutions in crypto and macro fields.

While most DAT company management teams come from the crypto-native circle, PURR's team is almost entirely composed of traditional finance veterans.

$HYPE's Strength Propels $PURR Skyward

The reason PURR caught the attention of the Chinese-speaking community is directly tied to HYPE's own strength.

HYPE has surged from around $25 at the beginning of the year, breaking through $62 in May to set a new all-time high, with a year-to-date increase exceeding 150%. Against the backdrop of BTC's sideways movement and ETH and SOL's relatively flat performance this year, HYPE stands out as the most impressive mainstream crypto asset.

Our previous articles have deconstructed Hyperliquid's fundamental flywheel: a perp DEX with about 70% market share, weekly fee revenue exceeding ten million dollars, and 97% of protocol fees used for HYPE buyback and burn. This flywheel continues to accelerate.

(Reference reading: "Market Watch: From HYPE to ZEC, Grasping the 4 Narrative Threads Behind Recent Altcoin Hype")

When HYPE rises, PURR naturally follows suit.

As the only HYPE proxy listed on US stock exchanges, PURR has gained over 100% year-to-date, rising from the $3 range to a recent high of $8.79.

For investors with only US stock accounts who do not directly access the crypto market, PURR is almost the only choice to gain HYPE exposure. However, what propelled PURR from a "niche asset" to a "social media topic" were several concentrated institutional signals materializing since May.

Goldman Sachs disclosed in its Q1 13F filing the purchase of approximately 650,000 PURR shares. While the amount isn't huge (around $3.3 million), the Goldman Sachs name itself serves as endorsement. Concurrently, 21Shares and Bitwise's HYPE spot ETFs were listed on NASDAQ and NYSE respectively, and Cantor Fitzgerald raised its PURR price target from $6 to $8.

These events, superimposed on the timing of HYPE's new high, pushed PURR into more people's field of vision.

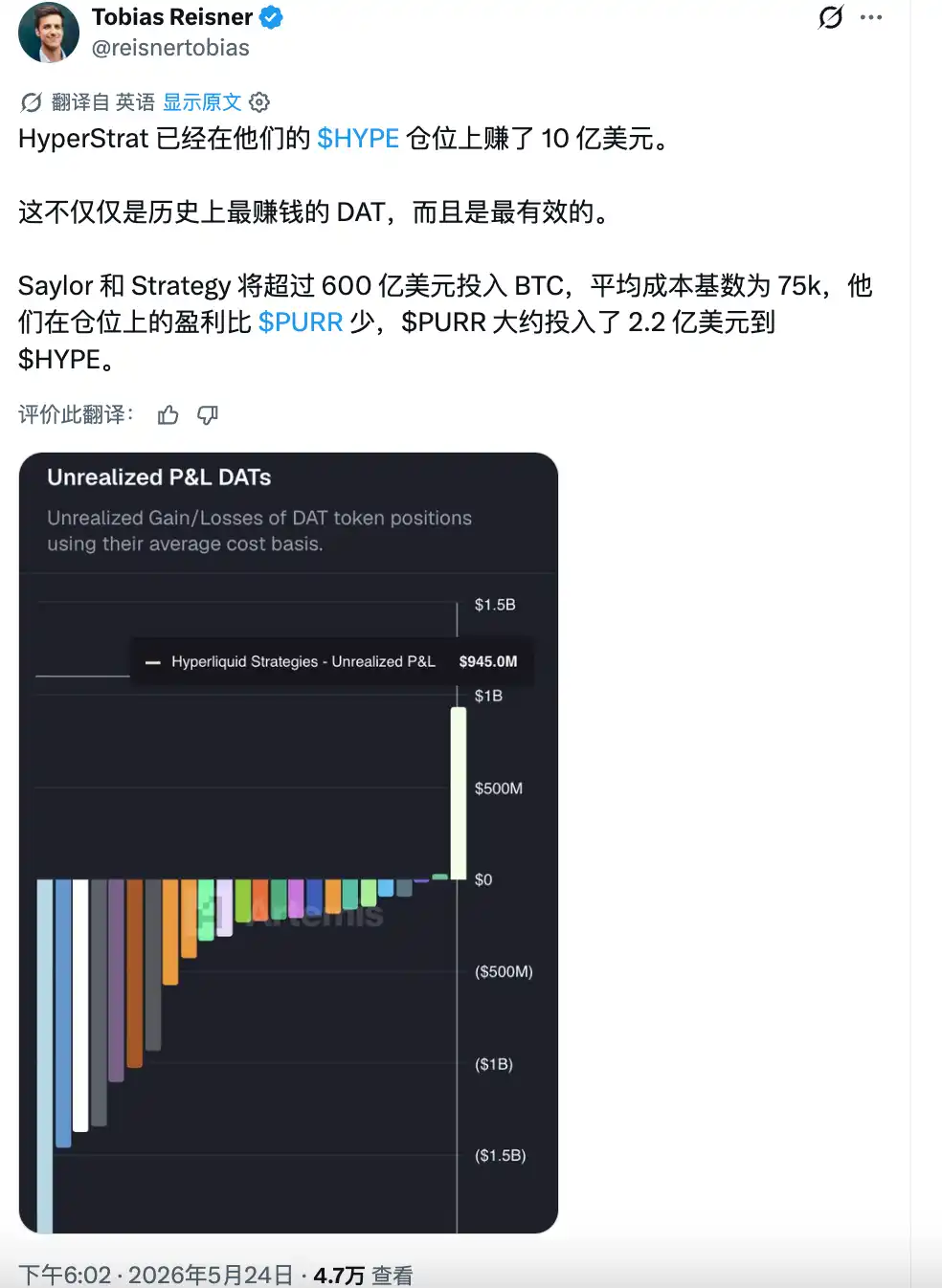

Then came the tweet mentioned at the beginning of the article: PURR used $220 million principal to buy HYPE, and its current unrealized profit is nearly $1 billion. Calculated in the short term, its capital efficiency definitely surpasses MicroStrategy's.

Under such a sharp rally, it's bound to attract significant attention. However, if you're considering trading this stock, caution is still advised.

The DAT with the Highest Capital Efficiency, Really?

Strategy (formerly MicroStrategy) invested over $60 billion to buy BTC at an average cost of around $75,000; PURR only used about $220 million to buy HYPE, yet its unrealized profit is close to or even exceeds the former's. The conclusion is that PURR's "capital efficiency" far surpasses MicroStrategy's?

This comparison holds up numerically but is logically misleading.

PURR's early HYPE holdings have an average cost of around $7, with the current price at $62, a nearly 9x increase. Strategy's BTC average cost is around $75,000, and BTC is currently hovering around that level, having barely moved.

Therefore, PURR's higher unrealized profit isn't due to any smarter operations by the company; it's simply because the underlying asset's appreciation is on a completely different scale. Anyone, at the same time, directly buying HYPE spot with the same amount of money could have achieved the same return rate, without bearing the risk of equity dilution.

In other words, it's a victory of "picking the right coin." If PURR's establishment date were pushed back half a year, entering when HYPE was at $40, this "capital efficiency" story wouldn't exist at all.

For US stock investors only noticing PURR today, a more practical question is: At the current price for PURR, are you paying a premium or a discount relative to the value of HYPE held by the company?

This involves the core valuation metric for DAT companies—mNAV (modified Net Asset Value per share).

We pulled data from PURR's official dashboard and SEC filings for a quick mNAV calculation.

The company currently holds 20.8 million HYPE tokens (worth approximately $1.296 billion at the current price), plus $114 million in cash. After deducting deferred tax liabilities and other liabilities, the net asset value is around $1.34 billion.

Based solely on the 134.6 million shares issued, the NAV per share is about $9.98. With the current stock price at $7.67, this represents a discount of about 23%. If we include the approximately 29.8 million existing warrants, fully diluted to about 155 million shares, the NAV per share becomes about $8.66, a discount of about 11%. However, the company just registered an additional 35.16 million shares for issuance. If all these are executed, expanding the denominator to about 190 million shares, the NAV per share drops to $7.07, and the stock price would instead represent a slight premium of 1.08x.

Therefore, whether PURR is "cheap" or "expensive" depends on how much future dilution you anticipate.

Issuance itself isn't necessarily bad. If management issues shares at a high premium and uses the raised capital to buy more HYPE, the HYPE holdings per share could actually increase. But if they issue shares when market sentiment cools and the stock price falls below NAV, that dilutes existing shareholders.

This company has only been operating for half a year and hasn't experienced a full downcycle. There is no historical record to reference how management will operate under extreme market conditions.

Also note that the deferred tax liability used in the above calculation is $60.5 million from the Q3财报 cutoff date (March 31). However, HYPE has risen significantly since the end of March, so the tax liability corresponding to unrealized gains has likely increased further. The actual NAV might be slightly lower than our calculation.

What's the Difference Between Buying PURR and Directly Buying HYPE

This is the most practical question. Since PURR's entire value derives from HYPE, why not skip the middle layer and buy HYPE directly?

The answer is simple: for some investors, they can't. US retirement accounts (IRA, 401k), traditional brokerage accounts, and some institutionally-managed funds with strict compliance requirements cannot directly hold crypto assets.

Moreover, the Hyperliquid platform explicitly restricts access for US residents.

Therefore, PURR provides a NASDAQ-listed stock wrapper, allowing such capital to gain HYPE exposure through standard stock trading. The shell built by Paradigm essentially sells this compliant access channel.

If you belong to this category of investors, PURR is indeed currently almost the only option. Although 21Shares and Bitwise's HYPE spot ETFs were listed in mid-May, these products have been live for a very short time, and their liquidity and tracking error remain to be observed.

But if you have the ability to buy HYPE directly, then PURR's stock wrapper layer becomes purely a friction cost with negative effects; it cannot be considered a source of extra alpha on top of HYPE's beta.

This cost manifests on several levels:

First, dilution risk. By directly holding HYPE, your share cannot be diluted by others. But by holding PURR stock, the company can issue new shares at any time to buy more HYPE.

Second, incomplete profit transmission. Direct HYPE holders can stake themselves to earn staking rewards, and future airdrops/ecosystem incentives go directly to them. Through PURR, staking rewards go to the company's accounts first, and only indirectly reflect in the net asset value per share after deducting operational expenses and taxes.

Third, trading time and pricing friction. HYPE trades 24/7, while PURR trades only during US stock market hours. If HYPE experiences significant volatility over the weekend or after-hours, PURR holders must wait for the market to open to react.

Fourth, counterparty risk. SEC filings disclose that PURR's entire HYPE holdings are custodied with a single custodian. By holding PURR, your asset safety relies on this custodian's performance capability and the company's operational continuity.

The author's judgment is that PURR is more of a "channel product" than an "investment product." Its value lies in bridging the channel from traditional financial accounts to HYPE, nothing more. If you don't need this channel, then every additional risk brought by the middle layer is unnecessary.

Therefore, for crypto and US stock investors in the Chinese-speaking community, the conclusion is relatively straightforward:

The judgment you need to make is whether you are bullish on HYPE, not whether you are bullish on the PURR shell itself.