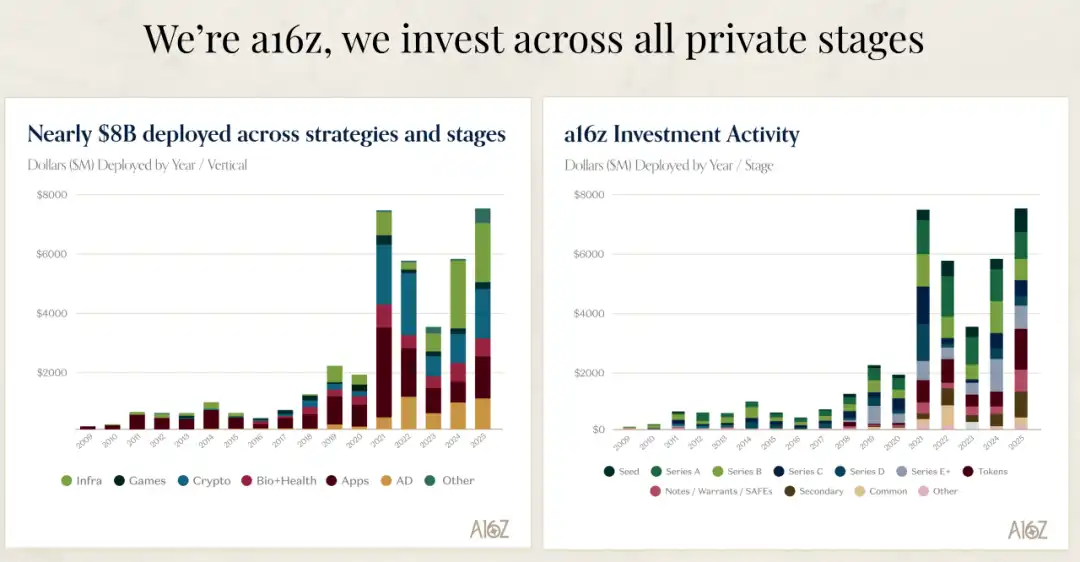

Author: Thought Circle

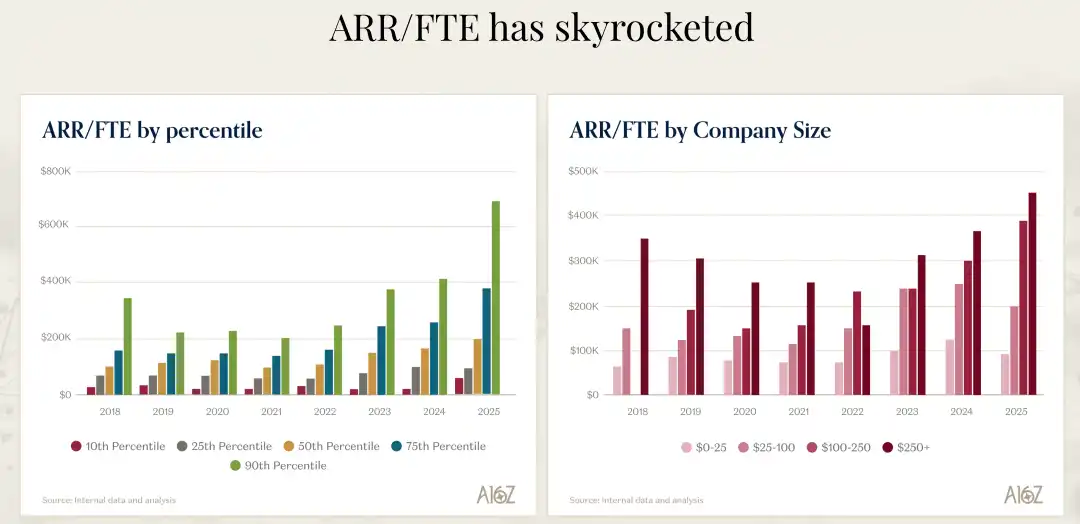

Have you ever thought that the software industry might be undergoing a transformation more dramatic than the shift from command line to graphical interface? Recently, I listened to a16z's David George's in-depth analysis of the AI market, and I was stunned by one set of data: the fastest-growing AI companies are expanding at an annual growth rate of 693%, while their spending on sales and marketing is significantly lower than that of traditional software companies. This is not an isolated case; the entire group of AI companies is growing more than 2.5 times faster than non-AI companies. What I find even more incredible is that these companies' ARR per FTE (Annual Recurring Revenue per Full-Time Employee) reaches $500,000 to $1 million, while the standard for the previous generation of software companies was $400,000.

What does this mean? It means we are witnessing the birth of a completely new business model, an era of creating greater value with fewer people and lower costs. D

avid George mentioned in his talk that this is not a minor adjustment, but a complete paradigm shift. Those core concepts—version control, templates, documentation, even the concept of a user—are being redefined by AI agent-driven workflows. I firmly believe that within the next five years, companies that cannot adapt to this change will be completely eliminated.

The Astonishing Truth About AI Company Growth

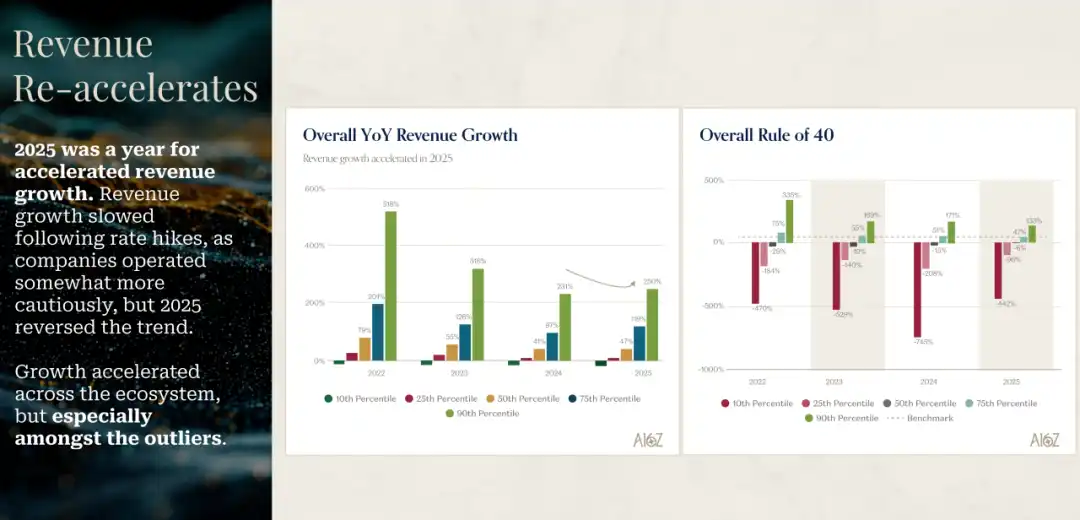

The data David George presented made me rethink what true growth really is. 2025 has been a year of accelerated growth for AI companies. After the growth deceleration in 2022, 2023, and 2024 due to rising interest rates and tech sector contraction, 2025 completely reversed this trend. Most astonishingly, among companies ranked by different tiers, the true outlier companies are growing at an almost unbelievable pace.

My first reaction upon seeing this data was: are these numbers correct? The top-performing group of AI companies is growing at 693% year-over-year. David said their team also triple-checked before believing this number. But it completely aligns with the actual situations and cases they see from their portfolio companies. This is not an isolated phenomenon, but a systemic change happening across the entire AI field.

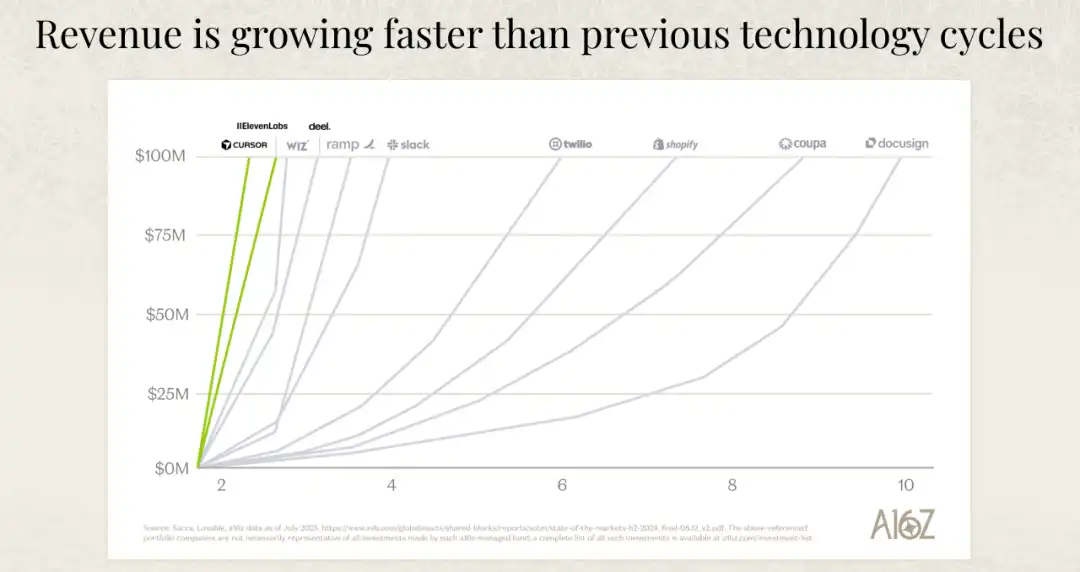

More importantly is the quality of growth. Traditional software companies usually take a long time to reach $100 million in annual revenue, while the fastest-growing AI companies reach this milestone much quicker. David emphasized a very important point: this is not because they are spending more on sales and marketing; on the contrary, the fastest-growing AI companies actually spend less on sales and marketing than traditional SaaS (Software as a Service) companies. They are growing faster while spending less. What's the reason? It's because end-customer demand is extremely strong, and the products themselves are highly compelling.

I think this reveals a profound shift in business logic. In the past era of software, growth often relied on strong sales teams and huge marketing budgets. You needed to educate the market, persuade customers, and overcome adoption barriers. But in the AI era, truly excellent products can speak for themselves. When a product can immediately create value for users, allowing them to feel an efficiency boost the first time they use it, market demand automatically arises. This product-driven growth model is much healthier and more sustainable than the traditional sales-driven model.

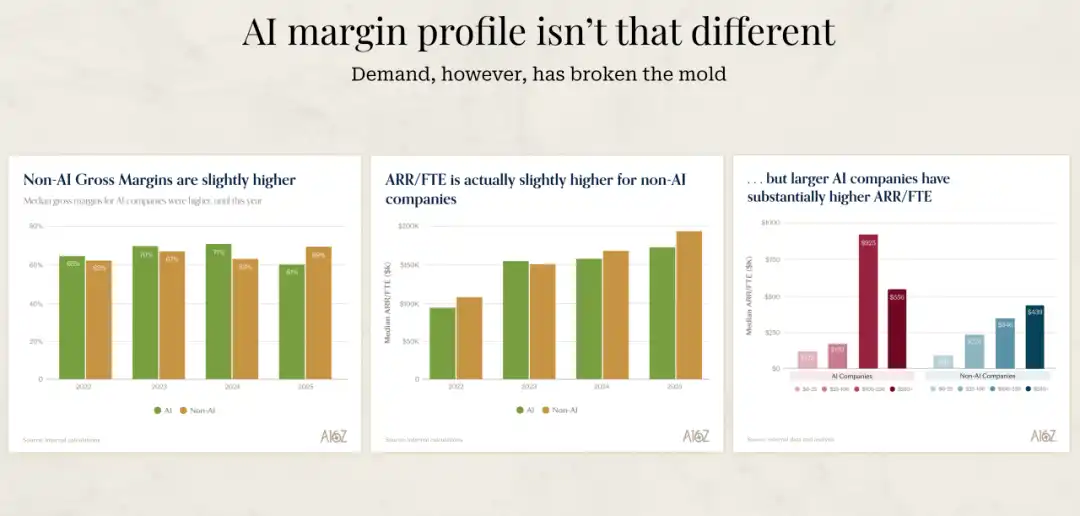

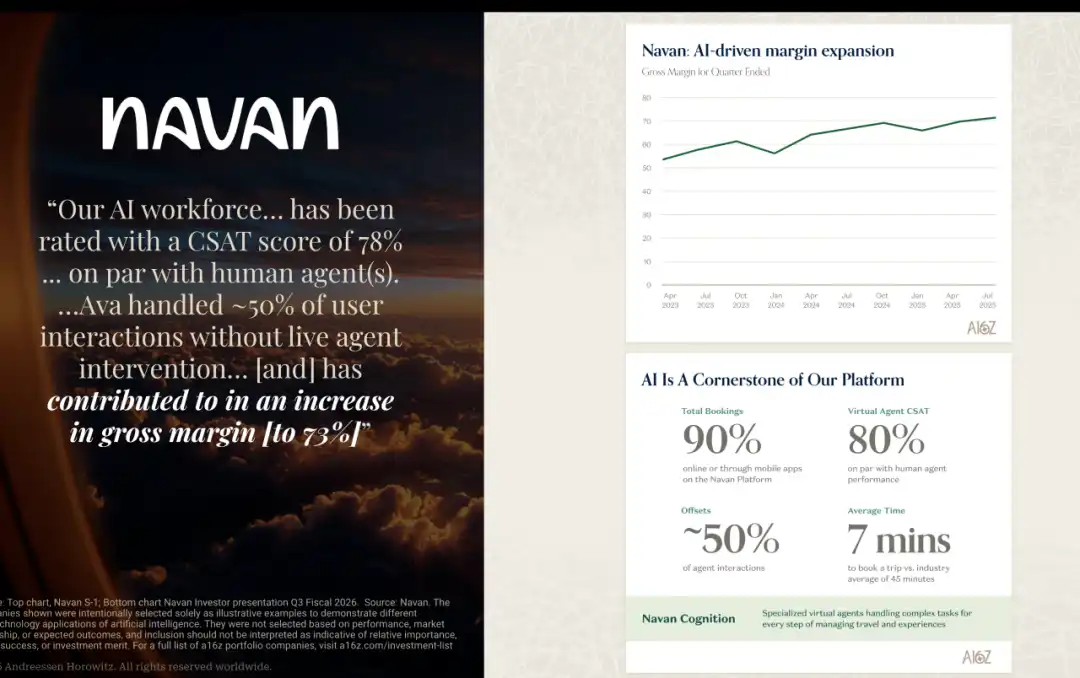

Another set of data David showed is also interesting. The gross margins of AI companies are actually slightly lower than those of traditional software companies. Their team has a unique perspective: for AI companies, low gross margin is somewhat a badge of honor. Because if the low gross margin is caused by high inference costs, it indicates two things: First, people are really using the AI features; Second, over time, these inference costs will decrease. So, in a way, if they see an AI company with particularly high gross margins, they might be a bit suspicious, as it could mean the AI features are not what customers are actually buying or using.

Why AI Companies Can Be More Efficient

I've been thinking about a question: Why can AI companies, also being software companies, create more revenue with fewer people? David focused on the ARR per FTE metric in his talk, which is the Annual Recurring Revenue per Full-Time Employee. This metric is actually a comprehensive indicator of a company's overall operational efficiency, encompassing not only sales and marketing efficiency but also management costs and R&D costs.

The ARR per FTE of the best AI companies reaches $500,000 to $1 million, while the standard for the previous generation of software companies was about $400,000. This might seem like just a numerical difference, but it reflects completely different business models and operational methods. David believes the main reason for this difference is that the market demand for these products is very strong, so they need fewer resources to bring the product to market.

But I think this is only the surface reason. The deeper reason is that AI companies are forced from the start to think differently about how to operate. They have no choice but to use AI to redesign their internal processes, product development methods, and customer support systems. This forced innovation反而 allows them to find a more efficient business model.

David shared a particularly vivid example. He said he recently chatted with a founder of a company who was dissatisfied with the progress of one of their products. So, he directly assigned two engineers who were deeply involved in AI to rebuild this product from scratch using the latest programming tools like Claude Code and Cursor, and gave them an unlimited budget for programming tools. The result? The founder said he believed the progress was 10 to 20 times faster than before. And the bills generated by these tools were so high that it made him start rethinking what the entire organization should look like.

What impressed me about this example is that this is not an incremental improvement, but an order-of-magnitude leap. What does a 10 to 20 times speed increase mean? It means a project that originally took a year might now be completed in one or two months. This speed difference will have a decisive impact in competition. This founder's conclusion was: I need the entire product and engineering team to work in this way, and I think this will happen within the next 12 months. But this also means the team's organizational structure will undergo fundamental changes. Where are the boundaries between product, engineering, and design? These questions all need to be redefined.

I believe December 2024 was a turning point in the field of programming. David feels the same. He said it felt like at that point in time, programming tools made a qualitative leap. In the next 12 months, this change will either truly take root in companies, or those that don't adopt it will be much slower than their peers. This is not alarmist; it's reality.

Adapt to AI or Be Eliminated

David mentioned a very stark view in his talk: For companies founded before the AI era, it's either adapt to the AI era or die. This sounds extreme, but I completely agree. And this adaptation needs to happen simultaneously on two fronts: the front end and the back end.

On the front end, companies need to think about how to natively integrate AI into the product, not just add a chatbot to existing workflows. This requires reimagining what the product can do with AI and being radically disruptive to themselves, making changes. David shared several interesting examples. There is a pre-AI era software company whose CEO has been completely converted by the AI concept, saying: We are going to become an AI product. We want the product to be able to say, your employees are now your AI agents. How many agents do you have? These are the topics he discusses now.

There is an even more extreme example. A CEO said, for every task we need to complete now, I ask one question: Can I do this with electricity, or must I do it with blood? This is an extreme mindset shift. Using electricity refers to using AI and automation; using blood refers to using human labor. This shift in thinking is very profound; it forces you to re-examine every process and every task in the company.

On the back end, companies need to fully adopt the latest programming models and tools. All developers should use the latest programming assistance tools, and every functional department should use the latest tools. So far, adoption rates are highest in the programming field, which is also where the biggest leaps are seen. But this change is spreading to other functional areas.

David mentioned that for those pre-AI companies, the good news is that the evolution of the business model is still in its early stages. The most disruptive scenario is when both technology/product and business model shift. Right now, technology and product are indeed undergoing dramatic changes, but the business model shift hasn't fully unfolded yet.

He sees the business model as a spectrum. On the far left is the license model (licenses), the pre-SaaS era license and maintenance model. Then comes SaaS and subscription models, usually based on seat pricing, which was a major innovation and very disruptive. You can look at what happened to Adobe during this transition. Then comes the consumption-based model, which is usage-based pricing, the way cloud services charge. Many usage-based businesses have moved from seat-based to consumption-based.

The next stage will be the outcome-based model. When you complete a task, ideally successfully complete a task, you charge based on the successful completion of the task. Currently, the only area where this might be truly feasible is customer support and customer success, because you can objectively measure problem resolution. But as model capabilities improve, if other functions beyond customer support can also measure such outcomes, that will be hugely disruptive to existing companies.

I find this evolution path very insightful. From license to subscription, from subscription to consumption, from consumption to outcome—each transition is a disruption of the previous generation's business model. And we are now on the eve of the transition from consumption to outcome. Once AI agents can reliably complete tasks and be objectively evaluated, outcome-based pricing will become mainstream. By then, companies still charging by seat will find themselves completely uncompetitive.

The AI Adoption Dilemma of Large Companies

Regarding Fortune 500 companies adopting AI, David's observations are very interesting. He said there is a huge gap between what he hears from the CEOs of these large companies and what is actually happening. The CEOs are all saying: We must adapt, we are desperate to understand what AI tools we need, we are ready to change, our business will roll out these tools across the board, we are going to be AI companies.

But the reality is completely different. The biggest disconnect between this mindset and actual business change is: change management is too difficult. Even just getting people to use AI assistants to help them do their jobs better is hard enough. As for actual business management, changing business processes, change management—these are extremely difficult.

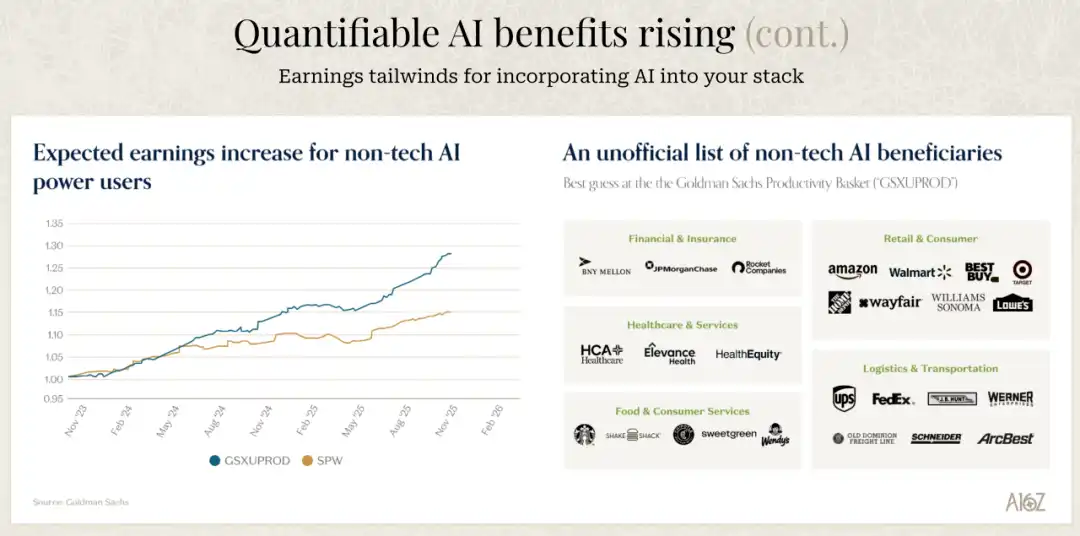

David said he isn't surprised by market chatter that things are moving slower than expected. But for the best companies that are truly fully embracing AI and know what to do, there has been a huge business impact. He gave a few specific examples: Chime said they reduced support costs by 60%; Rocket Mortgage said they saved 1.1 million hours in underwriting, a 6x year-over-year increase, equivalent to $40 million in annual operational savings.

I think this reveals a key problem: the gap between intention and capability. Large company CEOs have the intention to embrace AI, but whether they have the ability to implement it is another matter. The difficulty of change management is often underestimated. This is not just about buying some tools or hiring some AI engineers; it requires fundamentally changing the company's processes, culture, and organizational structure.

And many large companies need to first adjust their own business to make it ready for AI. Using a chatbot is one thing; how much productivity gain you might get is probably not much. But if you have to completely overhaul your systems, information, and backend to accommodate AI, a lot of work is potentially in the works, accumulating, and we haven't seen the related results yet.

David predicts the next 12 months will be very interesting. He thinks we will see more case studies, but there will be companies that figure it out and companies that don't. Those that figure it out will gain massive productivity advantages, and those that don't will be at a huge disadvantage. I believe this divergence will come faster and more sharply than people imagine.

Model Busters and the Future of the Market

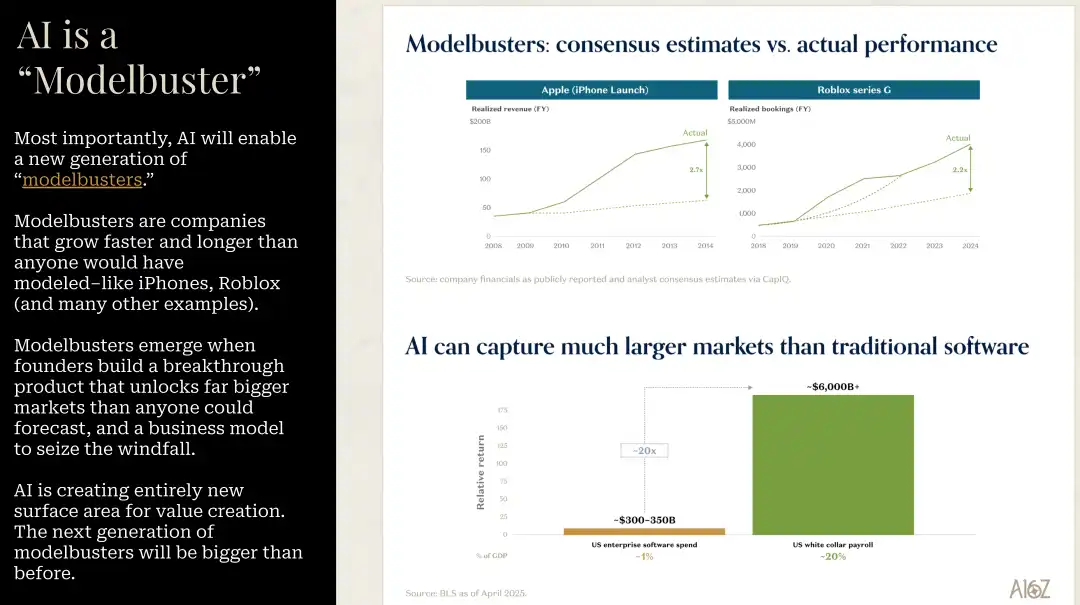

David mentioned a concept I find particularly insightful: Model Busters. These are companies whose growth speed and duration far exceed anything anyone could predict in any scenario. The iPhone is the classic case of this concept. If you look at the consensus forecast before the iPhone launch and the actual performance 4-5 years later, the consensus forecast was off by 3x. And this is the most watched company in the world.

David believes AI will be the biggest Model Buster he has seen in his career. The performance of many companies in the AI space will significantly exceed any expectations in any spreadsheet. I strongly agree with this view. When a technology platform brings not incremental improvement but order-of-magnitude leaps, traditional prediction models fail.

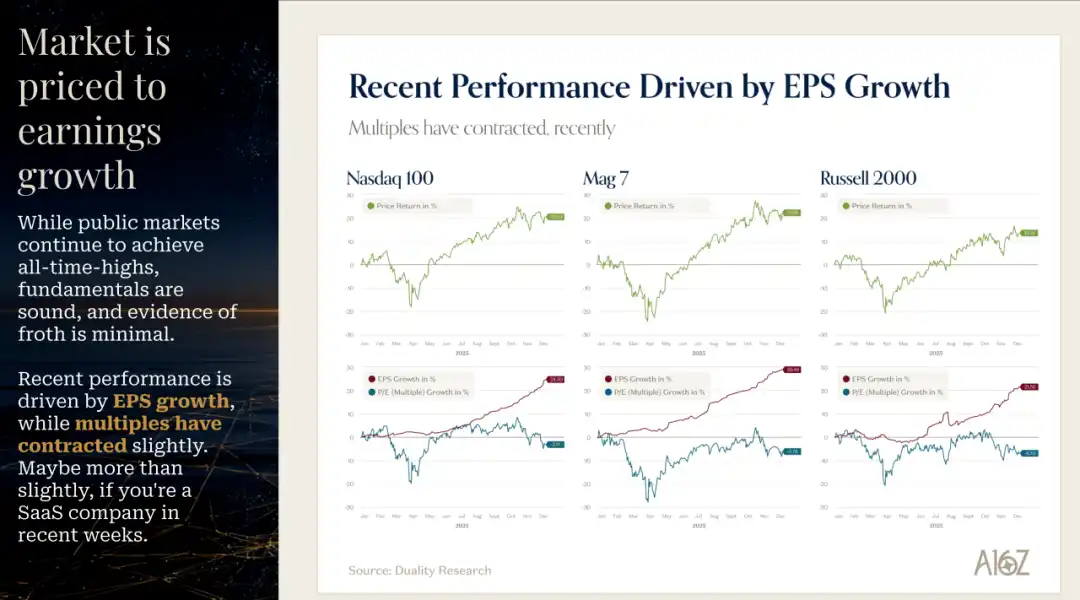

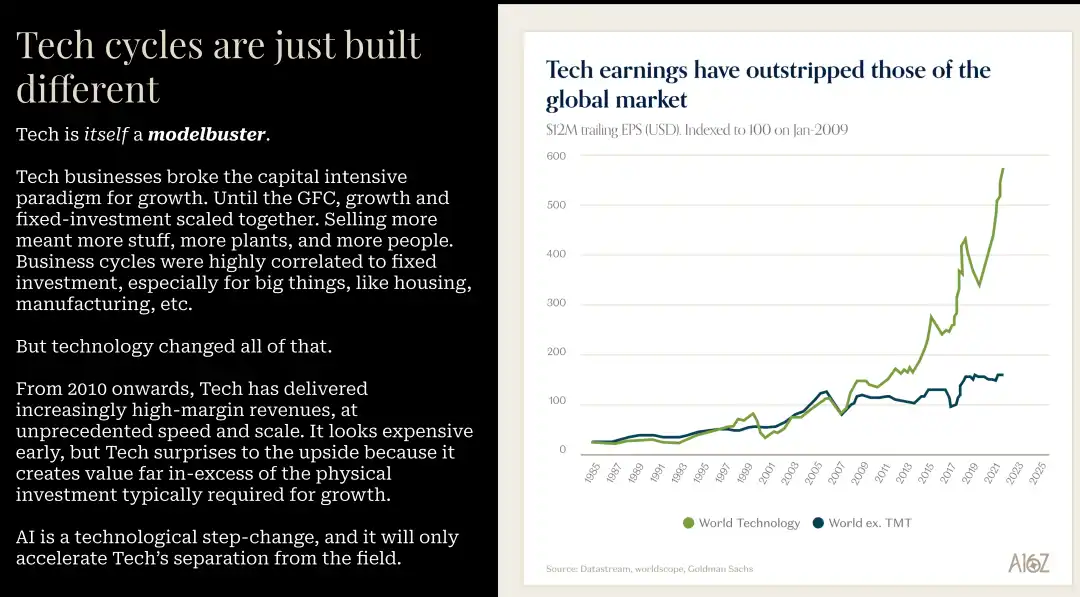

He mentioned that technology itself is a Model Buster. But since 2010, tech has delivered high-margin revenue at unprecedented speed and scale. So it always looks expensive early on, but it repeatedly outperforms expectations, creating value far in excess of the capital required. He sees no reason why this time should be any different.

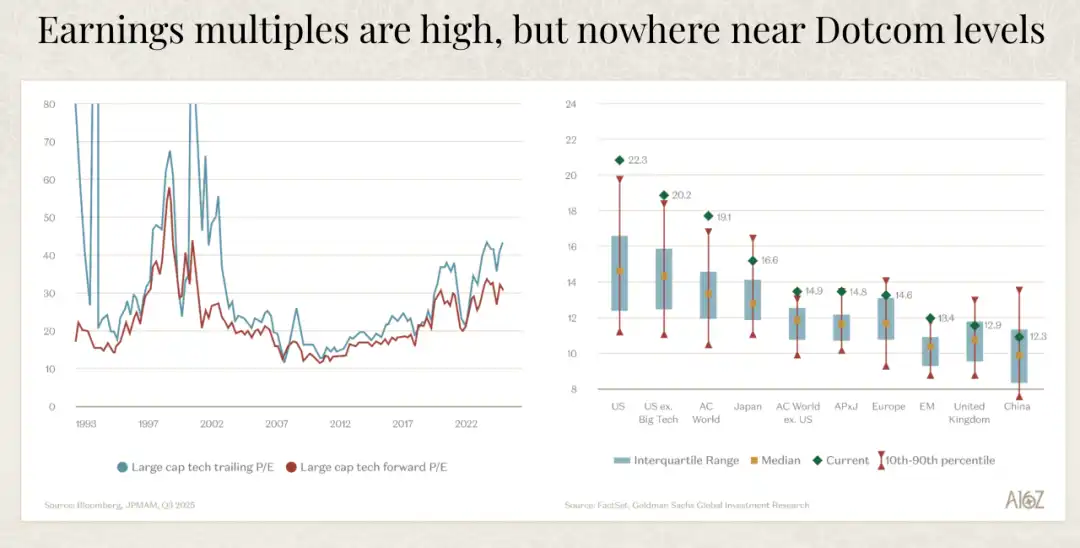

In terms of capital expenditure (capex), the data David showed is also interesting. Compared to the dot-com bubble era, current capex is actually supported by cash flow, and capex as a percentage of revenue is much lower. The hyperscale cloud providers bear the brunt of the capex burden, and these are some of the best business companies ever.

David specifically mentioned that, as a portfolio company, they very much welcome this capex. He said: Building as much capacity as possible, providing as much supply for training and inference as possible, is a very good thing. And the ones bearing most of the burden are some of the best business companies ever.

A phenomenon they are starting to watch is debt entering the equation. You can't fund all the forecasted future capex with just cash flow, and the market is starting to see some debt. But overall, they feel comfortable with companies funding with cash flow, continuing to generate cash flow, and using debt, as long as the counterparties are companies like Meta, Microsoft, AWS, Nvidia.

David mentioned a case worth watching: Oracle. Oracle has always been profitable, always buying back stock, but the scale of capex they've committed to is massive; it's a huge bet. They will have negative cash flow for many years to come. The market has started to notice this; Oracle's credit default swap (CDS) costs have risen to about 2% over the past three months. This is a signal to watch.

I think this capital-intensive building phase is necessary but not without risk. The key is to ensure these investments ultimately generate corresponding returns. Currently, demand far exceeds supply. All hyperscale cloud providers report demand far outstripping supply. Gavin Baker, whom David interviewed, had a great analogy: In the internet era, a lot of fiber was laid, and then that fiber sat idle, unused; this was called dark fiber. But in the AI era, there is no such thing as a dark GPU. If you install a GPU in a data center, it will be immediately fully utilized.

The Astonishing Speed of Revenue Growth

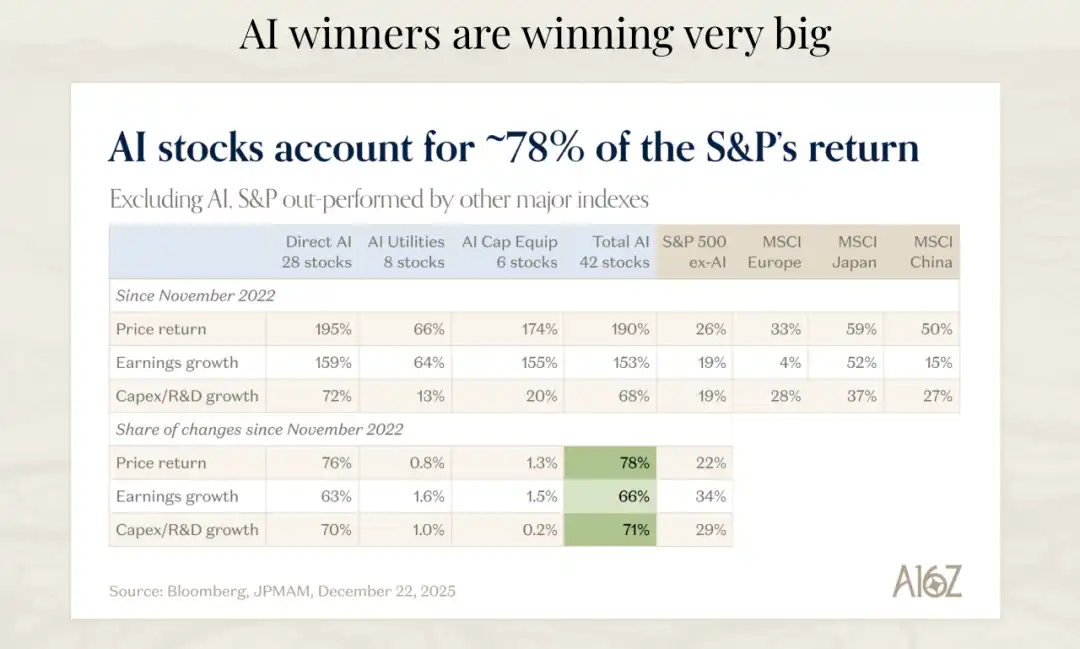

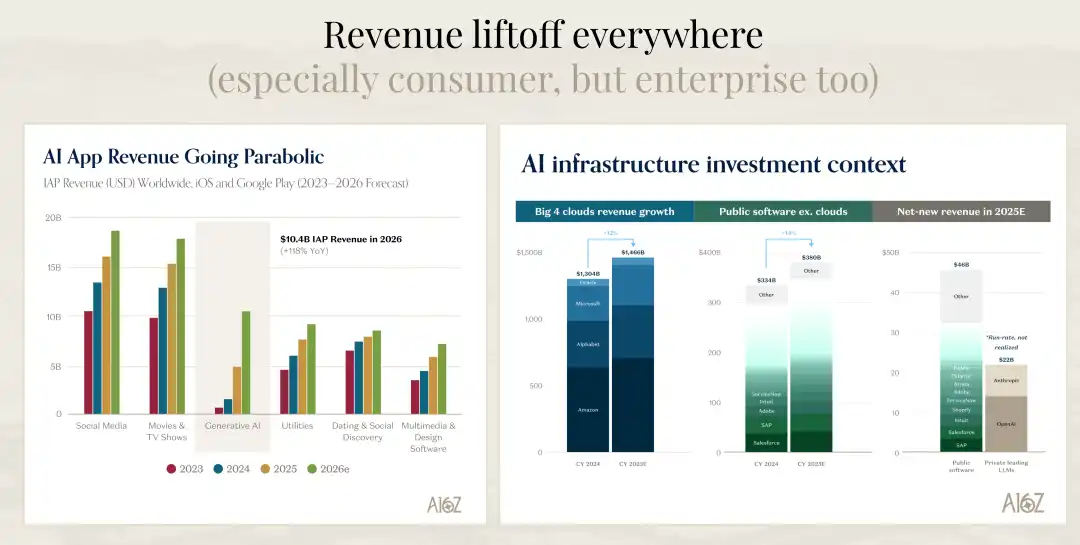

One set of data David showed was particularly震撼. He compared cloud services, public software companies, and the net new revenue added in 2025. Public software companies added a total of $46 billion in new revenue in 2025. If you look just at OpenAI and Anthropic, on an operating revenue basis, the new revenue they added is almost half of that number.

And David believes that if you do the same comparison for 2026, the new revenue added by AI companies (model companies) could reach 75% to 80% of the entire public software industry (including SAP and legacy software companies, not just SaaS). This speed is simply unbelievable. This means that within just a few years, the new value created by AI companies will surpass that of the entire traditional software industry.

Goldman Sachs estimates that AI build-out will generate $9 trillion in revenue. Assuming a 20% profit margin and a 22x P/E ratio, this would translate into $35 trillion in new market capitalization. About $24 trillion has already been提前 priced in. While we can argue whether this is all due to AI or large tech performance, there is still a lot of market cap up for grabs, and significant upside potential if these assumptions are correct.

David also did some simple arithmetic. Based on current estimates, by 2030, the cumulative capex of hyperscale cloud providers will be just under $5 trillion. To achieve a 10% hurdle rate on this $4.8 trillion or nearly $5 trillion investment, AI annual revenue needs to reach about $1 trillion by 2030. To put that number in context, $1 trillion is roughly 1% of global GDP, just to generate a 10% return.

Is this achievable? It might also fall slightly short. But David thinks looking仅仅 at 2030 is limiting. The returns on these investments will likely materialize over a longer period, say between 2030 and 2040. And if we are at roughly $50 billion in AI revenue now (his rough estimate), and this has mainly been generated in the past year and a half or so, then the path from $50 billion to $1 trillion is not unimaginable.

My Thoughts on the Future

After listening to David's talk, my biggest feeling is: we are at the beginning of a historic inflection point, not the middle or the end. This is a product cycle that could last 10 to 15 years, and we are just getting started. This makes me both excited and anxious.

Excited because the opportunities brought by this transformation are enormous. For companies that can adapt quickly and fully embrace AI, they will not only gain competitive advantages but are more likely to become the companies that define the next era. We will see new unicorns born, new business models emerge, and completely different ways of organizing companies.

Anxious because the speed of this change may be much faster than most people expect. The data David mentioned is particularly telling: the average time a S&P 500 company stays in the index has decreased by 40% over the past 50 years. This means the speed at which companies are being disrupted is accelerating. In the AI era, this speed is likely to accelerate further.

I believe a clear divergence will emerge next. Some companies will truly understand the potential of AI and fundamentally rethink their products, processes, and organizational structures. These companies will gain order-of-magnitude efficiency improvements and competitive advantages. Other companies, even if they have the intention to change, will progress slowly due to the difficulties of change management, organizational inertia, and technical debt. This divergence will become increasingly apparent in the coming years.

For entrepreneurs, now might be the best of times. Market demand is extremely strong, technological capabilities are advancing rapidly, and capital markets are still willing to support truly promising companies. And compared to the previous generation of software companies, it's now possible to reach the same scale with fewer resources and faster speed. This lowers the barrier to entry but also increases the requirements for product quality and market fit.

For investors, the key is to identify the true Model Busters. The growth speed and duration of these companies will far exceed any predictions from traditional models. But this also requires investors to have sufficient vision and patience, willing to believe growth curves that seem unreasonable.

For practitioners, whether you are an engineer, product manager, designer, or any other role, you need to quickly learn and adapt to new tools and ways of working. The example David mentioned—two engineers using the latest programming tools being 10 to 20 times faster than before—is not an isolated case but a trend. Those who can master these new tools and methods will gain huge career advantages.

Finally, I want to say that this transformation is not just technical, but also a shift in mindset. From "how should we do it" to "what outcome do we want to achieve", from "adding more people" to "how to solve this problem with AI", from "following established processes" to "reimagining possibilities". That question of "electricity or blood", although it sounds extreme, captures the essence of this shift.

We are witnessing the software world being rewritten. This is not an incremental upgrade, but a complete重构. Those who can understand this, embrace this, will define the next era.

Трендові криптовалюти

Пов'язані питання

QWhat is the key difference in growth and efficiency between the fastest-growing AI companies and traditional software companies according to the a16z analysis?![]()

AThe fastest-growing AI companies are expanding at an annual growth rate of 693%, which is 2.5 times faster than non-AI companies. They achieve this with significantly lower sales and marketing expenditures. Additionally, their ARR per FTE (Annual Recurring Revenue per Full-Time Employee) is $500,000 to $1 million, compared to the previous standard of $400,000 for traditional software companies, indicating a more efficient and scalable business model driven by strong product-market fit rather than heavy sales investment.

QHow does the article explain the lower gross margins of AI companies compared to traditional software firms?![]()

AThe article suggests that lower gross margins for AI companies can be a 'badge of honor' because they are often caused by high inference costs. This indicates two things: first, that customers are actually using the AI features extensively, and second, that these inference costs are expected to decrease over time. A very high gross margin might conversely raise suspicions that the AI functionality is not a core part of the product that customers value and use.

QWhat fundamental shift in business model evolution does the article predict is on the horizon due to AI?![]()

AThe article predicts a shift towards an 'outcome-based' business model. This model moves beyond current consumption-based pricing (paying for usage) to charging customers based on the successful completion of a specific task or the achievement of a desired result. This is seen as a potentially massive disruption, as it aligns pricing directly with the value delivered, unlike traditional seat-based SaaS subscriptions or even usage-based cloud models.

QWhat major challenge do large Fortune 500 companies face in adopting AI, despite their CEOs' enthusiasm?![]()

AThe primary challenge is the 'change management gap.' There is a significant disconnect between the CEOs' strategic desire to adopt AI and the practical difficulty of implementing it. Transforming business processes, retraining or restructuring teams, and integrating AI natively into complex existing systems is extremely difficult. This often leads to much slower actual implementation and business transformation than the initial ambitious statements from leadership would suggest.

QWhat is the concept of a 'Model Buster' as described in the article, and why is AI considered one?![]()

AA 'Model Buster' is a company whose growth speed and duration far exceed any reasonable consensus prediction made by traditional financial or business models. The iPhone is given as a classic example. AI is considered the ultimate Model Buster of this era because the technology delivers not just incremental improvements but order-of-magnitude leaps in capability and efficiency. This fundamental shift makes historical data and conventional forecasting models largely ineffective for predicting the growth and impact of leading AI companies.

Пов'язані матеріали

Торгівля

Популярні статті

Що таке $S$

Розуміння SPERO: Комплексний огляд Вступ до SPERO Оскільки ландшафт інновацій продовжує еволюціонувати, виникнення технологій web3 та криптовалютних проектів відіграє ключову роль у формуванні цифрового майбутнього. Один з проектів, який привернув увагу в цій динамічній сфері, — це SPERO, позначений як SPERO,$$s$. Ця стаття має на меті зібрати та представити детальну інформацію про SPERO, щоб допомогти ентузіастам та інвесторам зрозуміти його основи, цілі та інновації в рамках web3 та крипто-сектору. Що таке SPERO,$$s$? SPERO,$$s$ — це унікальний проект у криптопросторі, який прагне використати принципи децентралізації та технології блокчейн для створення екосистеми, що сприяє залученню, корисності та фінансовій інклюзії. Проект розроблений для полегшення взаємодії між користувачами новими способами, надаючи їм інноваційні фінансові рішення та послуги. У своїй основі SPERO,$$s$ прагне надати можливості індивідам, забезпечуючи інструменти та платформи, які покращують користувацький досвід у криптовалютному просторі. Це включає в себе можливість більш гнучких методів транзакцій, сприяння ініціативам, що підтримуються спільнотою, та створення шляхів для фінансових можливостей через децентралізовані додатки (dApps). Основна концепція SPERO,$$s$ обертається навколо інклюзивності, прагнучи зменшити розриви в традиційній фінансовій системі, використовуючи переваги технології блокчейн. Хто є творцем SPERO,$$s$? Особистість творця SPERO,$$s$ залишається дещо невідомою, оскільки є обмежені публічно доступні ресурси, що надають детальну інформацію про його засновників. Ця відсутність прозорості може бути наслідком зобов'язання проекту до децентралізації — етики, яку багато проектів web3 поділяють, ставлячи колективні внески вище за індивідуальне визнання. Зосереджуючи обговорення навколо спільноти та її колективних цілей, SPERO,$$s$ втілює суть наділення без виділення конкретних осіб. Таким чином, розуміння етики та місії SPERO є більш важливим, ніж ідентифікація єдиного творця. Хто є інвесторами SPERO,$$s$? SPERO,$$s$ підтримується різноманітними інвесторами, починаючи від венчурних капіталістів до ангельських інвесторів, які прагнуть сприяти інноваціям у крипто-секторі. Зосередження цих інвесторів зазвичай узгоджується з місією SPERO — пріоритет надається проектам, які обіцяють технологічний прогрес у суспільстві, фінансову інклюзію та децентралізоване управління. Ці інвесторські фонди зазвичай зацікавлені в проектах, які не лише пропонують інноваційні продукти, але й позитивно впливають на спільноту блокчейн та її екосистеми. Підтримка з боку цих інвесторів підкріплює SPERO,$$s$ як значного конкурента в швидко змінюваній сфері крипто-проектів. Як працює SPERO,$$s$? SPERO,$$s$ використовує багатогранну структуру, яка відрізняє його від традиційних криптовалютних проектів. Ось деякі ключові особливості, які підкреслюють його унікальність та інноваційність: Децентралізоване управління: SPERO,$$s$ інтегрує моделі децентралізованого управління, надаючи користувачам можливість активно брати участь у процесах прийняття рішень щодо майбутнього проекту. Цей підхід сприяє відчуттю власності та відповідальності серед членів спільноти. Корисність токена: SPERO,$$s$ використовує свій власний криптовалютний токен, розроблений для виконання різних функцій в екосистемі. Ці токени дозволяють здійснювати транзакції, отримувати винагороди та полегшувати послуги, що пропонуються на платформі, підвищуючи загальну залученість та корисність. Шарова архітектура: Технічна архітектура SPERO,$$s$ підтримує модульність та масштабованість, що дозволяє безперешкодно інтегрувати додаткові функції та додатки в міру розвитку проекту. Ця адаптивність є надзвичайно важливою для збереження актуальності в постійно змінюваному крипто-ландшафті. Залучення спільноти: Проект підкреслює ініціативи, що підтримуються спільнотою, використовуючи механізми, які стимулюють співпрацю та зворотний зв'язок. Підтримуючи сильну спільноту, SPERO,$$s$ може краще задовольняти потреби користувачів та адаптуватися до ринкових тенденцій. Фокус на інклюзію: Пропонуючи низькі комісії за транзакції та зручні інтерфейси, SPERO,$$s$ прагне залучити різноманітну базу користувачів, включаючи осіб, які раніше не брали участі в крипто-просторі. Це зобов'язання до інклюзії узгоджується з його загальною місією наділення через доступність. Хронологія SPERO,$$s$ Розуміння історії проекту надає важливі уявлення про його розвиток та етапи. Нижче наведено пропоновану хронологію, що відображає значні події в еволюції SPERO,$$s$: Етап концептуалізації та ідеації: Початкові ідеї, що стали основою SPERO,$$s$, були сформовані, тісно пов'язані з принципами децентралізації та фокусом на спільноті в індустрії блокчейн. Запуск білого паперу проекту: Після концептуального етапу був випущений комплексний білий папір, що детально описує бачення, цілі та технологічну інфраструктуру SPERO,$$s$, щоб залучити інтерес та зворотний зв'язок від спільноти. Створення спільноти та ранні залучення: Активні зусилля були спрямовані на створення спільноти ранніх прихильників та потенційних інвесторів, що полегшило обговорення цілей проекту та отримання підтримки. Подія генерації токенів: SPERO,$$s$ провів подію генерації токенів (TGE) для розподілу своїх рідних токенів серед ранніх прихильників та встановлення початкової ліквідності в екосистемі. Запуск початкового dApp: Перший децентралізований додаток (dApp), пов'язаний з SPERO,$$s$, став доступним, дозволяючи користувачам взаємодіяти з основними функціями платформи. Постійний розвиток та партнерства: Безперервні оновлення та вдосконалення пропозицій проекту, включаючи стратегічні партнерства з іншими учасниками блокчейн-простору, сформували SPERO,$$s$ у конкурентоспроможного та еволюціонуючого гравця на крипто-ринку. Висновок SPERO,$$s$ є свідченням потенціалу web3 та криптовалют для революціонізації фінансових систем та наділення індивідів. Завдяки зобов'язанню до децентралізованого управління, залучення спільноти та інноваційно спроектованих функцій, він прокладає шлях до більш інклюзивного фінансового ландшафту. Як і з будь-якими інвестиціями в швидко змінюваному крипто-просторі, потенційним інвесторам та користувачам рекомендується ретельно досліджувати та обдумано взаємодіяти з поточними подіями в SPERO,$$s$. Проект демонструє інноваційний дух крипто-індустрії, запрошуючи до подальшого дослідження його численних можливостей. Хоча подорож SPERO,$$s$ ще триває, його основні принципи можуть справді вплинути на майбутнє того, як ми взаємодіємо з технологією, фінансами та один з одним у взаємопов'язаних цифрових екосистемах.

221 переглядів усьогоОпубліковано 2024.12.17Оновлено 2024.12.17

Що таке AGENT S

Агент S: Майбутнє автономної взаємодії в Web3 Вступ У постійно змінюваному ландшафті Web3 та криптовалюти інновації постійно переосмислюють, як люди взаємодіють з цифровими платформами. Один з таких новаторських проектів, Агент S, обіцяє революціонізувати взаємодію людини з комп'ютером через свою відкриту агентну структуру. Прокладаючи шлях для автономних взаємодій, Агент S прагне спростити складні завдання, пропонуючи трансформаційні застосування в штучному інтелекті (ШІ). Це детальне дослідження заглиблюється в складності проекту, його унікальні особливості та наслідки для сфери криптовалюти. Що таке Агент S? Агент S є революційною відкритою агентною структурою, спеціально розробленою для вирішення трьох основних викликів в автоматизації комп'ютерних завдань: Набуття специфічних знань у галузі: Структура інтелектуально навчається з різних зовнішніх джерел знань та внутрішнього досвіду. Цей подвійний підхід дозволяє їй створити багатий репозиторій специфічних знань у галузі, покращуючи її продуктивність у виконанні завдань. Планування на довгих горизонтах завдань: Агент S використовує планування з підкріпленням досвіду, стратегічний підхід, який полегшує ефективний розподіл та виконання складних завдань. Ця функція значно підвищує її здатність ефективно та результативно управляти кількома підзавданнями. Обробка динамічних, неоднорідних інтерфейсів: Проект представляє Інтерфейс Агент-Комп'ютер (ACI), інноваційне рішення, яке покращує взаємодію між агентами та користувачами. Використовуючи багатомодальні великі мовні моделі (MLLMs), Агент S може безперешкодно орієнтуватися та маніпулювати різноманітними графічними інтерфейсами користувача. Завдяки цим новаторським функціям Агент S надає надійну структуру, яка вирішує складнощі, пов'язані з автоматизацією людської взаємодії з машинами, прокладаючи шлях для численних застосувань у ШІ та за його межами. Хто є творцем Агент S? Хоча концепція Агент S є фундаментально новаторською, конкретна інформація про його творця залишається невідомою. Творець наразі невідомий, що підкреслює або початкову стадію проекту, або стратегічний вибір зберегти засновників у таємниці. Незважаючи на анонімність, акцент залишається на можливостях та потенціалі структури. Хто є інвесторами Агент S? Оскільки Агент S є відносно новим у криптографічній екосистемі, детальна інформація про його інвесторів та фінансових спонсорів не задокументована. Відсутність публічно доступних відомостей про інвестиційні фонди або організації, що підтримують проект, викликає питання щодо його фінансової структури та дорожньої карти розвитку. Розуміння підтримки є критично важливим для оцінки стійкості проекту та потенційного впливу на ринок. Як працює Агент S? В основі Агент S лежить передова технологія, яка дозволяє йому ефективно функціонувати в різних умовах. Його операційна модель побудована навколо кількох ключових функцій: Взаємодія з комп'ютером, подібна до людської: Структура пропонує розширене планування ШІ, прагнучи зробити взаємодії з комп'ютерами більш інтуїтивними. Імітуючи людську поведінку при виконанні завдань, вона обіцяє підвищити досвід користувачів. Наративна пам'ять: Використовується для використання високорівневого досвіду, Агент S використовує наративну пам'ять для відстеження історій завдань, тим самим покращуючи свої процеси прийняття рішень. Епізодична пам'ять: Ця функція надає користувачам покрокові інструкції, дозволяючи структурі пропонувати контекстуальну підтримку в міру виконання завдань. Підтримка OpenACI: Завдяки можливості працювати локально, Агент S дозволяє користувачам зберігати контроль над своїми взаємодіями та робочими процесами, узгоджуючи з децентралізованою етикою Web3. Легка інтеграція з зовнішніми API: Його універсальність і сумісність з різними платформами ШІ забезпечують те, що Агент S може безперешкодно вписатися в існуючі технологічні екосистеми, роблячи його привабливим вибором для розробників та організацій. Ці функціональні можливості колективно сприяють унікальному положенню Агент S у крипто-просторі, оскільки він автоматизує складні, багатоступеневі завдання з мінімальним втручанням людини. У міру розвитку проекту його потенційні застосування в Web3 можуть переосмислити, як відбуваються цифрові взаємодії. Хронологія Агент S Розробка та етапи Агент S можуть бути узагальнені в хронології, яка підкреслює його значні події: 27 вересня 2024 року: Концепція Агент S була представлена в комплексній науковій статті під назвою “Відкрита агентна структура, яка використовує комп'ютери як людина”, що демонструє основи проекту. 10 жовтня 2024 року: Наукова стаття була опублікована на arXiv, пропонуючи детальне дослідження структури та її оцінки продуктивності на основі бенчмарку OSWorld. 12 жовтня 2024 року: Було випущено відеопрезентацію, що надає візуальне уявлення про можливості та особливості Агент S, ще більше залучаючи потенційних користувачів та інвесторів. Ці маркери в хронології не лише ілюструють прогрес Агент S, але й вказують на його прихильність до прозорості та залучення громади. Ключові моменти про Агент S У міру розвитку структури Агент S кілька ключових характеристик виділяються, підкреслюючи її новаторський характер та потенціал: Інноваційна структура: Розроблена для забезпечення інтуїтивного використання комп'ютерів, подібного до людської взаємодії, Агент S пропонує новий підхід до автоматизації завдань. Автономна взаємодія: Здатність автономно взаємодіяти з комп'ютерами через GUI означає стрибок до більш інтелектуальних та ефективних обчислювальних рішень. Автоматизація складних завдань: Завдяки своїй надійній методології він може автоматизувати складні, багатоступеневі завдання, роблячи процеси швидшими та менш схильними до помилок. Безперервне вдосконалення: Механізми навчання дозволяють Агенту S покращуватися на основі минулого досвіду, постійно підвищуючи свою продуктивність та ефективність. Універсальність: Його адаптивність до різних операційних середовищ, таких як OSWorld та WindowsAgentArena, забезпечує його здатність служити широкому спектру застосувань. Оскільки Агент S займає своє місце в ландшафті Web3 та криптовалюти, його потенціал покращити можливості взаємодії та автоматизувати процеси означає значний прогрес у технологіях ШІ. Завдяки своїй інноваційній структурі Агент S є прикладом майбутнього цифрових взаємодій, обіцяючи більш безперешкодний та ефективний досвід для користувачів у різних галузях. Висновок Агент S представляє собою сміливий крок вперед у поєднанні ШІ та Web3, з можливістю переосмислити, як ми взаємодіємо з технологією. Хоча проект все ще на ранніх стадіях, можливості для його застосування є величезними та переконливими. Завдяки своїй комплексній структурі, що вирішує критичні виклики, Агент S прагне вивести автономні взаємодії на передній план цифрового досвіду. У міру того, як ми заглиблюємося в сфери криптовалюти та децентралізації, проекти, подібні до Агент S, безсумнівно, відіграватимуть ключову роль у формуванні майбутнього технологій та співпраці людини з комп'ютером.

843 переглядів усьогоОпубліковано 2025.01.14Оновлено 2025.01.14

Як купити S

Ласкаво просимо до HTX.com! Ми зробили покупку Sonic (S) простою та зручною. Дотримуйтесь нашої покрокової інструкції, щоб розпочати свою криптовалютну подорож.Крок 1: Створіть обліковий запис на HTXВикористовуйте свою електронну пошту або номер телефону, щоб зареєструвати обліковий запис на HTX безплатно. Пройдіть безпроблемну реєстрацію й отримайте доступ до всіх функцій.ЗареєструватисьКрок 2: Перейдіть до розділу Купити крипту і виберіть спосіб оплатиКредитна/дебетова картка: використовуйте вашу картку Visa або Mastercard, щоб миттєво купити Sonic (S).Баланс: використовуйте кошти з балансу вашого рахунку HTX для безперешкодної торгівлі.Треті особи: ми додали популярні способи оплати, такі як Google Pay та Apple Pay, щоб підвищити зручність.P2P: Торгуйте безпосередньо з іншими користувачами на HTX.Позабіржова торгівля (OTC): ми пропонуємо індивідуальні послуги та конкурентні обмінні курси для трейдерів.Крок 3: Зберігайте свої Sonic (S)Після придбання Sonic (S) збережіть його у своєму обліковому записі на HTX. Крім того, ви можете відправити його в інше місце за допомогою блокчейн-переказу або використовувати його для торгівлі іншими криптовалютами.Крок 4: Торгівля Sonic (S)Легко торгуйте Sonic (S) на спотовому ринку HTX. Просто увійдіть до свого облікового запису, виберіть торгову пару, укладайте угоди та спостерігайте за ними в режимі реального часу. Ми пропонуємо зручний досвід як для початківців, так і для досвідчених трейдерів.

1.8k переглядів усьогоОпубліковано 2025.01.15Оновлено 2026.06.02