Charles Hoskinson has urged Cardano DReps to back a research funding proposal, warning that a failure to do so could damage one of the network’s core value propositions: its identity as a research-led blockchain.

Speaking in a May 21 livestream from England, Hoskinson said Cardano is in “treasury season” and facing a tougher funding environment than last year. According to him, the ecosystem is asking for about $52 million in funding this year, down from roughly $98 million last year, after cuts that have already affected engineers and community teams.

“Many people have had to make profound sacrifices,” Hoskinson said. “Good people have had to go. Engineers have been let go. Community teams liquidating familiar faces and new faces alike.”

But the proposal that drew his strongest concern was research. Hoskinson said he had seen a “disturbing trend” of some DReps voting against funding Cardano’s research group, despite what he described as its foundational role in the network’s development.

Hoskinson Defends Cardano’s Research Core

Hoskinson framed the debate as larger than a budget dispute. In his view, Cardano’s long-running research program is the “spine and backbone” of the ecosystem and a key reason the project has differentiated itself from other major blockchains.

“The spine and backbone of what makes Cardano Cardano has always been and will always be the fact that we’re the science coin,” he said. “We’re the research coin. Over the last 10 years, hundreds of millions of dollars has been spent, and countless hundreds of researchers have been involved in the production of the largest research group in the world for cryptocurrencies.”

He pointed to Cardano’s work on proof-of-stake research, extended UTXO, Plutus, sidechains and Bitcoin-related DeFi research as examples of the group’s output. He also argued that the network’s academic ties, spanning institutions such as Stanford, the University of Edinburgh, the University of Wyoming and others, are not easily replaceable.

Hoskinson said critics of the proposal have argued that research funding should be broken apart, allowing the ecosystem to “pick and choose” which areas or people to keep. He rejected that framing, saying it would force the ecosystem into decisions it is not equipped to make without damaging the research operation as a whole.

“So then I asked the DReps, which scientists would you like me to fire?” he said, before naming several researchers associated with Cardano’s technical development. “And if not people, perhaps institutions. Which institutions would you like to shut down? And because you’re so qualified, which research agendas do you so feel are unnecessary?”

Warning Over Talent Flight

A major part of Hoskinson’s argument was that Cardano’s researchers could be recruited by better-funded rival ecosystems if the project signals that their work is no longer valued. He said other blockchains with large treasuries would likely be interested in the same cryptographers, programming language experts and distributed systems researchers.

“If you treat these people like commodities, they will leave,” Hoskinson said. “They’ll leave to other ecosystems that have a lot more money and are willing to pay a lot more with better stability and certainty.”

He warned that the loss would not be easily reversible. Academic and technical talent, he argued, depends on long-term stability, and once researchers move on to other ecosystems, Cardano may not be able to bring them back. “We can’t recover this. It’s a one-way door. If you lose your best and brightest, we won’t get them back. We don’t get to say we’re sorry.”

Hoskinson also tied the issue to market perception. He asked what Cardano’s investment case would look like over the next three to five years if the ecosystem signaled it was no longer willing to support research. Without that layer, he suggested, Cardano would have to lean more heavily on metrics such as monthly active users, TVL or transaction volume.

The livestream ended as a direct appeal to DReps who have not yet voted and to those who have voted against the proposal. Hoskinson asked them to reconsider, saying research funding is not a discretionary line item but part of Cardano’s long-term competitive position.

“You can’t walk without a spine,” he said. “Please vote for science. Please vote for the research proposal for IOG. It’s a necessary foundational proposal, and we can’t afford to lose it.”

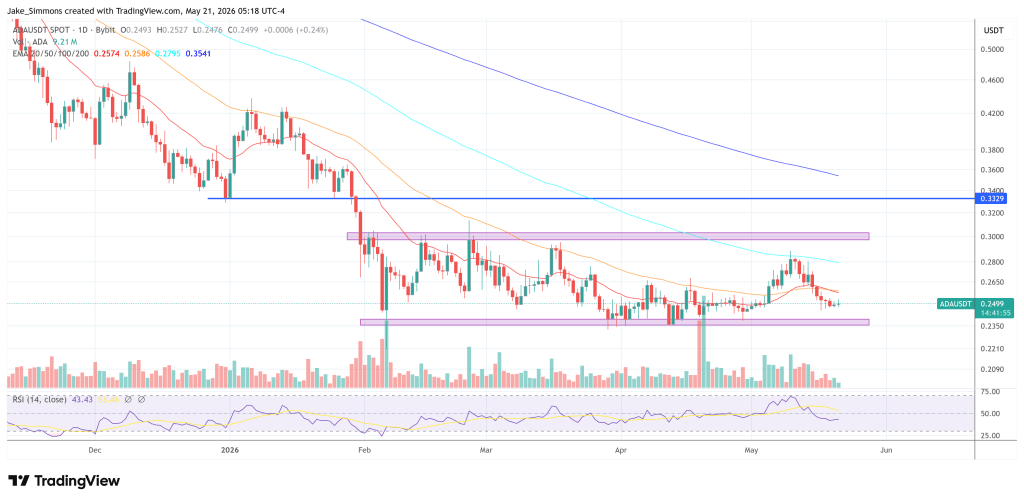

At press time, ADA traded at $0.2499.