Editor's Note: For a long time, prediction markets have been viewed as a kind of "fringe product": first as academic experiments, later as tools for election season discourse, and then again as an extension of sports betting. They always seemed to attach themselves to some high-attention scenario but were rarely truly understood as financial infrastructure.

However, in the author's view, prediction markets are gradually evolving from a marginal, election-and-sports-focused "event trading tool" into a financial infrastructure capable of pricing uncertainty.

The author points out that key industry changes are evident on three levels: first, application scenarios are expanding—while sports remain the traffic entry point, long-tail markets like entertainment, macroeconomics, and CPI are growing faster and beginning to carry institutional demand; second, prediction markets for the first time provide a tradable price benchmark for the "event itself," enabling institutions to directly hedge political or macro risks instead of making "secondary bets" through correlated assets; third, the path to institutional adoption is advancing, from data reference (checking odds) to system integration, and then to actual trading participation, with the current stage still being early.

Prediction markets are undergoing a process similar to the early days of the options market: "professionalization — institutionalization — infrastructuralization." Once liquidity, leverage, and regulation are gradually perfected in the future, they could become a core market tool connecting retail and institutional investors for hedging and pricing real-world uncertainty.

Finance is a highly "vertically stratified" world, where almost every niche has its own公认的 "annual mecca." Leaders from healthcare providers, payers, and biotech companies gather annually in San Francisco for the J.P. Morgan Healthcare Conference. Heavyweights in global macro and political figures from various countries go to the Swiss Alps for the World Economic Forum Annual Meeting (Davos). TMT, real estate, industrial, financial services, and almost every industry you can think of also have their own most representative flagship summits.

At the end of March this year, Kalshi's academic and institutional research department, Kalshi Research, held its first research conference in New York, bringing together academics, Wall Street executives, former political figures, and the traders who truly drive the markets. The composition of the attendees clearly indicated a trend: this industry is "maturing."

The day's events opened with a conversation between Kalshi co-founders Tarek Mansour and Luana Lopes Lara and Katherine Doherty. Below are some industry observations distilled from that dialogue and the subsequent roundtable discussions:

Markets and Life: More Than Just Elections and Sports.

During major news cycles, a fixed pattern often emerges: a major event (like the 2024 election, the Super Bowl, or more recently, March Madness college basketball) dominates the vast majority of media headlines and consequently dominates the trading volume in prediction markets. This easily creates the impression that "the value of prediction markets is only evident in these events."

However, although early narratives often framed prediction markets as tools "only meaningful during election cycles," Kalshi's growth in other areas has been equally significant.

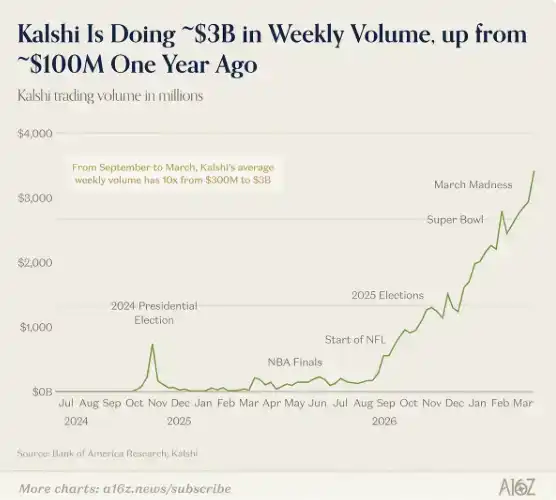

At the time of the research conference, weekly trading volume for sports contracts had just approached $3 billion, accounting for about 80% of Kalshi's total volume, largely driven by "March Madness." Tarek and Luana viewed this high concentration as a phased phenomenon.

A more explanatory data point: despite the absolute size of sports trading hitting a record high, its share of total trading volume was at a historical low. This means that all other categories were growing faster.

The two founders pointed out that categories like entertainment, crypto, politics, and culture are showing stronger user growth and better trading retention structures than sports. Sports are more like a "trigger" for the mass market—they are highly familiar, have clear temporal rhythms, and strong emotional engagement, making them a typical entry product.

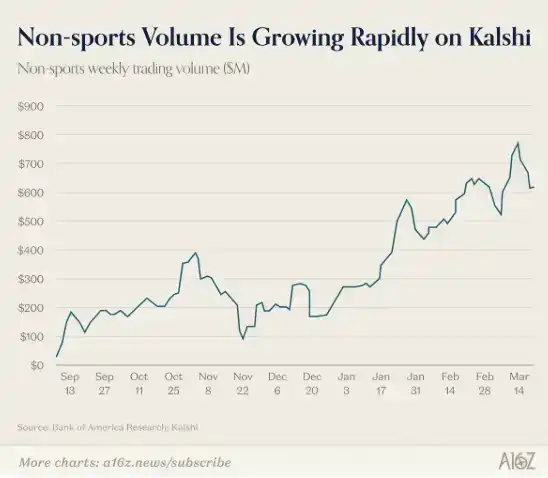

Meanwhile, the company has also observed significant growth in longer-tail markets. These markets currently constitute over 20% of Kalshi's trading volume and will play a more critical role in future institutional hedging and information markets.

A subsequent institutional roundtable confirmed this assessment from the demand side.

Cyril Goddeeris, Co-Head of Global Equities Business at Goldman Sachs, stated that predictions related to macro events and CPI data are the categories Wall Street is most focused on currently. Sally Shin, Executive Vice President of Growth Business at CNBC, mentioned that she already uses prediction markets like "Fed Chair's tenure" and "Non-Farm Payrolls data" as narrative tools for content. Tradeweb's Global Markets Co-Head, Troy Dixon, went further to描绘 a future picture: large investment banks will establish dedicated prediction market trading desks, with financial contracts as core products.

Why Kalshi Attracts Wall Street's Attention

An important reason traditional financial markets can function is that each core asset class has a公认的 benchmark: the S&P 500 index represents the overall performance of 500 stocks, crude oil has benchmark price systems like ICE.

But for political and macroeconomic events (e.g., who wins an election, whether tariffs pass, the outcome of a Supreme Court case), there has long been a lack of widely accepted, dynamically updated "pricing benchmarks." Prediction markets change this—now, the future of almost any event can have a real-time, liquid "price anchor."

Once an event (e.g., "Will a 30% tariff pass?") has a credible price, institutions can trade directly around that price. This allows for both trading the event itself and hedging risks in other parts of a portfolio. As Tradeweb's Troy Dixon said: "Go back to Trump's first election. There was a lot of hedging in the equity market then, the logic being to short the S&P because if Trump wins, the market will definitely fall. But that trade failed. The question was: how do you price these events? Where is the benchmark?"

Tarek also mentioned this was one of his motivations for founding Kalshi. During his tenure at Goldman Sachs, his trading desk had recommended trades based on the 2024 election and Brexit. Without prediction markets, institutions hedging political or macro events through correlated assets were actually betting on two things simultaneously: first, whether the event itself would happen, and second, the correlation between that event and the traded asset. And the second judgment could be wrong on its own.

When the event itself has a direct price benchmark, these two layers of risk are compressed into one. As Tarek said: "Now, this market is starting to price everything."

The Three Stages of True Institutional Adoption of Prediction Markets

It is clearly still too early to say that major Wall Street institutions are trading on Kalshi on a large scale. Currently, most institutions' usage remains at the "data source" level, not the "trading platform" level.

However, Luana pointed out that the path to institutional adoption of this market is clear and can be divided into three stages:

The first stage is data access: getting prediction prices into the daily workflow of institutions. For example, getting Goldman Sachs portfolio managers to habitually check Kalshi's odds data just like they check the VIX index. This stage is already happening to some extent. John Hopkins University professor and former Fed official Jonathan Wright stated: "In areas like Fed decisions, unemployment, GDP, Kalshi is almost the only reference source."

The second stage is system integration: including compliance and legal approval, technical integration, and internal education—essentially the process of introducing a new financial instrument.

The third stage is actual trading: institutions begin to directly hedge risks on the platform, trading volume and market depth gradually accumulate. At this point, more hedging demand attracts speculators, tighter spreads attract more hedgers, and the benchmark price forms a self-reinforcing positive feedback loop.

Currently, most institutions are still in the first stage, some are entering the second stage, and very few have truly entered the third stage. A major obstacle is that current market trading requires full margin. For example, a $100 position requires a $100 margin deposit. This is acceptable for individual investors but too costly for hedge funds or banks that rely on leverage and capital efficiency.

As Tarek said: "If you want to do a $100 hedge, you have to put $100 in the clearinghouse. That's too expensive for institutions. Firms like Citadel or Millennium won't do that." Kalshi has already obtained a license from the National Futures Association (NFA) and is working with the Commodity Futures Trading Commission (CFTC) to introduce margin trading mechanisms.

What Happens Next?

Michael McDonough, Head of Market Innovation at Bloomberg, summarized it most directly: "The sign of success is when these things become boring." He compared prediction markets to the options market in the 1970s, which was同样 full of controversy over manipulation and regulatory uncertainty but eventually evolved into an infrastructure, so much so that today almost no one thinks twice about it.

AQR partner Toby Moskowitz said he "would bet real money" that prediction markets will become a viable institutional tool within five years, possibly even sooner.

Vote Hub's Garrett Herren described the end state: "The question is no longer whether to use prediction markets, but how to use them. Once the question becomes that, it means they have become indispensable."

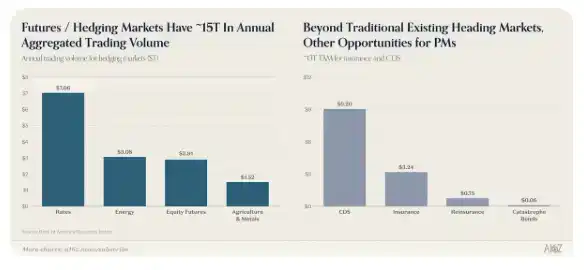

In fact, although the current scale of prediction markets is still limited, the hedging market itself is a massive field.

In fact, the "normalization" of prediction markets is already happening.

In the politics-themed roundtable, former Congressman Mondaire Jones mentioned that senior figures in both parties—including President Trump, House Minority Leader Jeffries, and Senate Minority Leader Schumer—have begun citing Kalshi's odds data in public. DDHQ's Scott Tranter also confirmed that prediction market data has now become a standard input within party committees. Meanwhile, Vote Hub announced it has directly integrated Kalshi data into its midterm election forecasting models.

And all of this did not exist at all two years ago. Back then, the most successful traders on Kalshi were still predominantly "amateurs." Now, that term isn't even accurate anymore.

In Kalshi's "The People Behind the Markets" roundtable, four traders shared their career paths—these paths sounded no different from traditional professional traders: one spent 11 years studying the Billboard music charts, another has been refining his skills in prediction markets since 2006, when it was still a "somewhat geeky hobby that barely made money." Notably, none of these four guests came from traditional finance; they came from music, politics, and poker respectively. But they unanimously agreed that the platform truly rewards deep domain knowledge, not glossy resumes.

Prediction markets have come a long way. Initially seen as academic experiments, then as "novelty tools" during elections, later categorized as "sports-betting-like products," their positioning has constantly changed. The clear signal from this conference is: prediction markets are evolving into an infrastructure—for pricing uncertainty, serving a wide range of participants from retail traders to large institutions and diverse application scenarios.