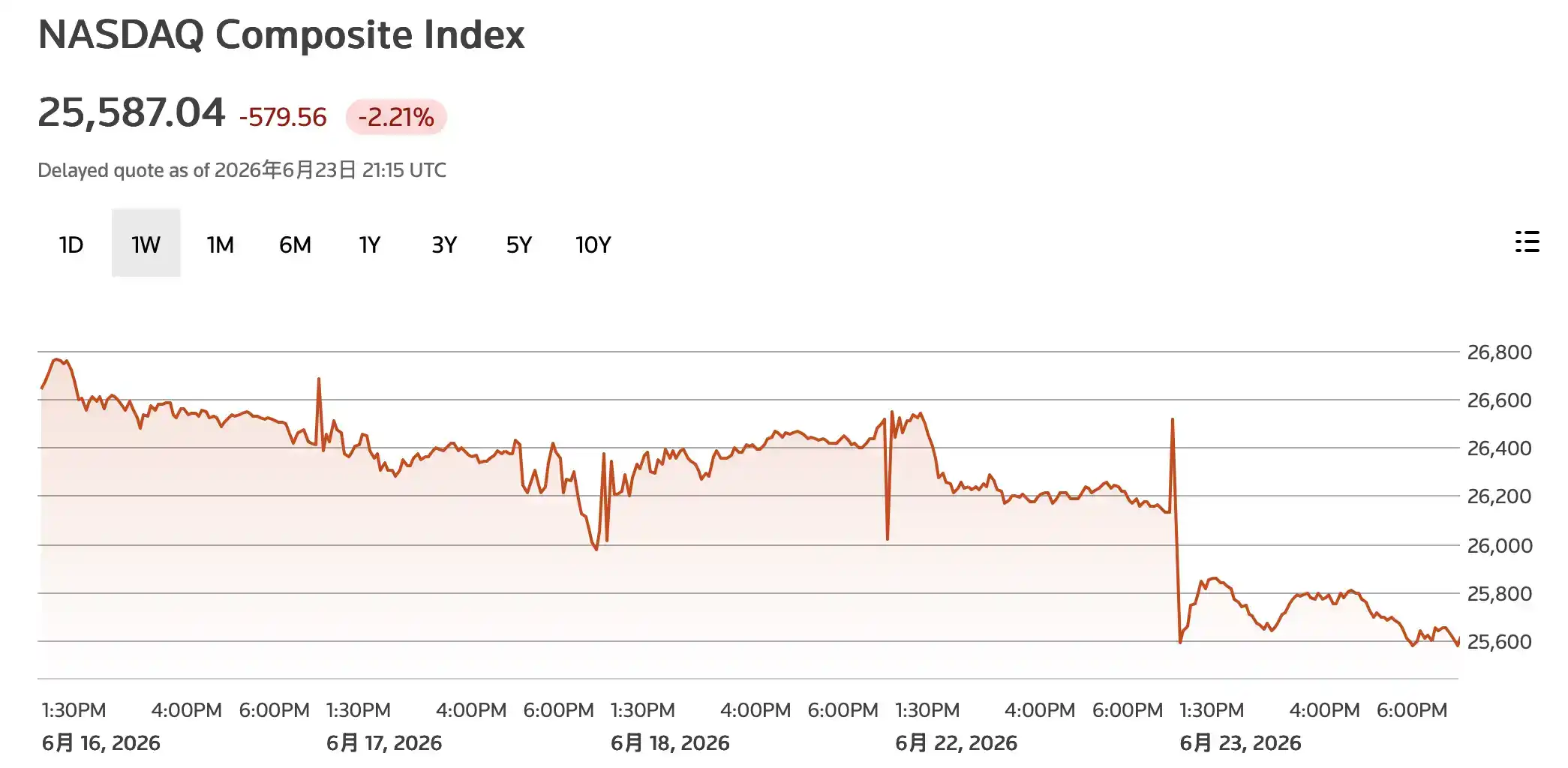

According to an AP report, on June 23rd, U.S. tech stocks and the AI supply chain collectively fell, with the Nasdaq closing down 2.2% and the S&P 500 dropping 1.4%. This pullback was not due to an isolated problem at a single chip company, but rather the simultaneous pressure on two fronts affecting the most crowded AI hardware trades of the past year. The first is a sudden intensification of expectations for Federal Reserve rate hikes, and the second is investors beginning to question when the sustained increase in AI capital expenditures by cloud providers will translate into sufficiently clear profits.

The most direct pressure fell on the hardware supply chain. Market data showed that NVIDIA (NVDA) fell about 4% on Tuesday, with its market cap dropping below $5 trillion. Micron plummeted 13.2%, Qualcomm fell about 8%, and SanDisk and Western Digital also saw significant declines. Weakness in memory, storage, AI chips, and mobile chips together indicates the selling was not confined to a specific subsector.

Asian markets also faced simultaneous pressure. South Korea's KOSPI index fell nearly 10% on June 23rd, with SK Hynix and Samsung Electronics both recording double-digit percentage drops. In recent months, tight supply of HBM and memory chips had been supporting Korean tech stocks, but this time, the market chose to cash in profits first.

AI Hardware Chain Was the First to Be Sold

The sequence of this decline is significant. Investors did not retreat first from software or internet platforms but instead sold off the chip and memory stocks that had benefited most from the AI capital expenditure boom in the past.

NVIDIA remains the core stock of the AI boom. Its GPUs have almost defined this data center expansion cycle and have also become the most concentrated outlet for market risk appetite. Falling below a $5 trillion market cap itself does not change the company's industry position, but from a trading perspective, it is a conspicuous price signal. When both the interest rate and return cycles are being questioned simultaneously, assets with the largest gains and most crowded holdings are often sold first.

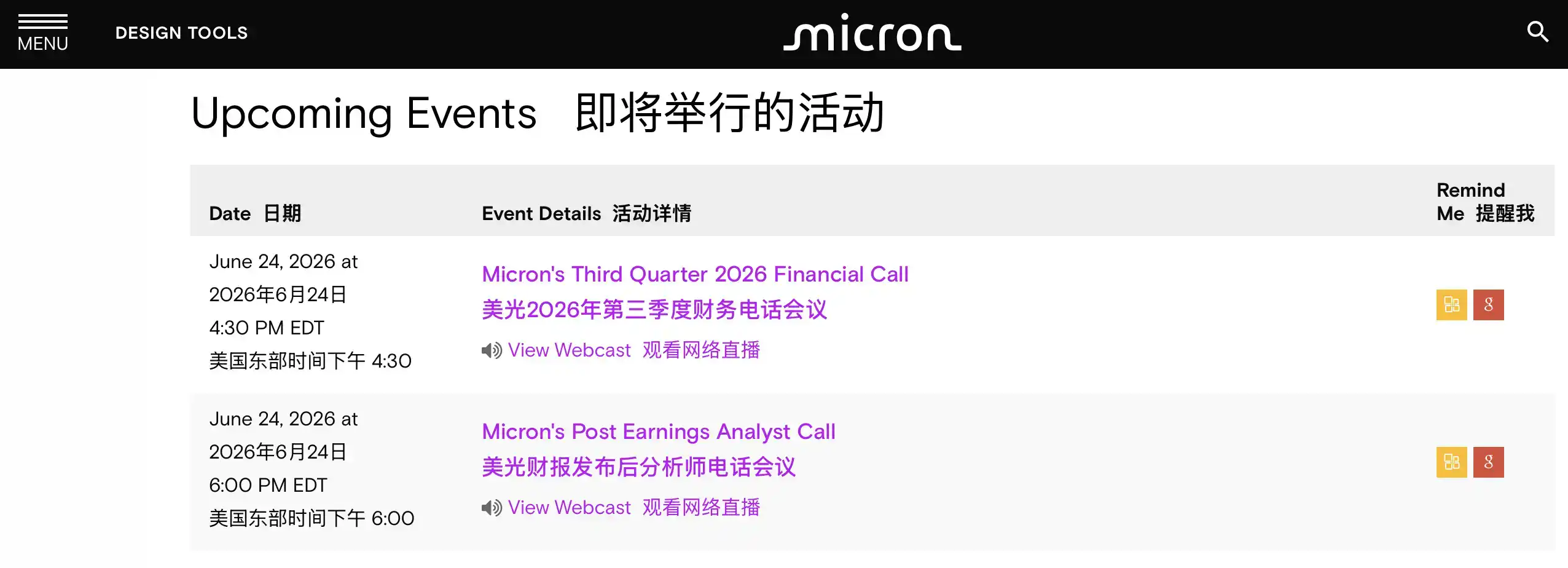

Micron's sharper decline is partly due to its approaching earnings report. The company announced it will report its fiscal 2026 third-quarter results and hold an earnings call on June 24th. The market had previously bet on continued tight demand for high-bandwidth memory driven by AI servers. If the guidance is not strong enough, investors worry the earlier gains lack new earnings catalysts; even if the guidance is strong, it needs to prove that high memory prices and AI demand are not just short-term stockpiling.

The reaction in the South Korean market further amplified these concerns. SK Hynix and Samsung are key companies in the global memory and HBM supply chain. Their double-digit declines indicate this adjustment has spread from U.S. market leaders to the global AI hardware supply chain.

Previously, Broadcom's AI revenue guidance failing to meet the most optimistic expectations had already triggered a round of selling in chip stocks. Tuesday's action was more like a concentrated release of such worries. AI demand still exists, but the market is no longer willing to pay increasingly high prices just for a "huge future."

Turning Hawkish on Rate Hike Expectations, High-Valuation Tech Stocks Under Pressure

The macro trigger came from a shift in Federal Reserve policy expectations.

The Federal Reserve announced that Kevin Warsh was sworn in as its new Chairman on May 22nd. Reuters cited Bank of America forecasts suggesting the Fed could raise rates by 25 basis points each in September, October, and December of 2026, for a cumulative 75 basis points for the year. The reasoning includes labor market resilience and inflation pressures not fully subsiding.

This is particularly unfriendly to tech stocks. Valuations of AI leaders rely on long-term growth expectations. Rising interest rates increase the discounting pressure on future cash flows and make lower-risk assets like U.S. Treasuries attractive again. Recent high U.S. Treasury yields and a noticeable increase in futures market bets on rate hikes this year indicate the market is quickly adjusting its expectations for the policy path.

The market is not suddenly doubting the existence of AI, but is recalculating a more realistic question: If the cost of capital is higher and future profit realization is farther away, what price is one willing to pay for AI assets now?

This is also why the adjustment in chips, memory, and high-growth tech stocks has been so synchronized. They previously benefited together from the combination of "sustained explosion in AI demand" and "interest rates eventually falling." Once one of these pillars loosens, the parts with the biggest gains and highest valuations come under pressure first.

Cloud Providers Are Still Spending, Investors Start Questioning Returns

The other pressure comes from AI capital expenditure itself.

Hyperscale cloud and AI investors like Alphabet, Amazon, and Meta are still maintaining high-intensity data center construction. Over the past year, such spending has been seen by the market as a guarantee of demand for NVIDIA, memory chips, power equipment, and data center assets. As long as cloud providers kept spending, the hardware chain had revenue.

But now the question has become: Can this money ultimately be earned back?

AI model training and inference require massive computing power, electricity, and server investment. Cloud providers can monetize through enterprise customers, advertising tools, developer platforms, and consumer subscriptions, but whether service pricing can cover capital expenditures has not been fully proven. The market is beginning to scrutinize AI product pricing, customer usage intensity, and whether enterprises are willing to pay high fees for generative AI long-term with a more critical eye.

This is also why the "sell the heavy spenders" trade is starting to gain traction. Investors are not just selling chip stocks; they are also becoming more cautious about internet and cloud computing giants that keep increasing their AI budgets. The more aggressive the spending was before, the more likely they are to be questioned about profit margins and free cash flow.

Volatility in high-valuation assets is also amplifying this sentiment. According to an Axios report, SpaceX fell over 16% on Monday after its IPO, losing about $400 billion in market value. It is not the main cause of this chip stock decline, but it shows that strong-narrative, high-valuation assets are facing stricter market scrutiny.

Too Early to Talk About a Bubble Burst, Micron and Inflation Data to Provide Answers

A more accurate description of this adjustment is that after substantial gains, the AI trade is experiencing a concentrated pullback, not that a bubble has definitively burst.

AI hardware demand still exists, and cloud provider capital expenditures have not stopped. The fundamentals of companies like NVIDIA, Micron, and SK Hynix are still closely tied to data center construction, HBM supply, and AI server shipments. The real question is whether current stock prices have already priced in too much good news.

The first validation point is Micron's earnings report. The market will watch three things: whether memory demand driven by AI servers remains strong, whether price increases can be sustained, and whether management's guidance for subsequent quarters is sufficient to support the prior gains. If the report is strong, the chip chain may get a breather; if guidance falls short, selling could continue to spread to more AI supply chain companies.

The second validation point is interest rates. Whether the Fed under Warsh's leadership actually starts hiking in September will depend on inflation, employment, and energy prices. If inflation pressures remain stubborn, growth stock valuations will continue to face pressure; if data cools, the market may again bet on a policy pivot, giving tech stocks room to recover.

The current market divergence is whether this is just a normal profit-taking episode within an AI bull market or the beginning of a shift from "just buy growth" to "must see returns." At the very least, Tuesday's decline shows that while the AI narrative remains powerful, it can no longer alone offset the pressure brought by higher interest rates and a longer profit realization horizon.