By | Chanyejia

Musk once made a judgment: in the future, Tokens will be consumed like data traffic.

Looking at this statement today, it is not just an imagination of AI usage methods, but a prediction of a new industry measurement logic. Shifting focus from the operators' "self-reconstruction" to the broader market, a new industry landscape driven by Tokens is unfolding.

AI cloud is reaching a milestone turning point.

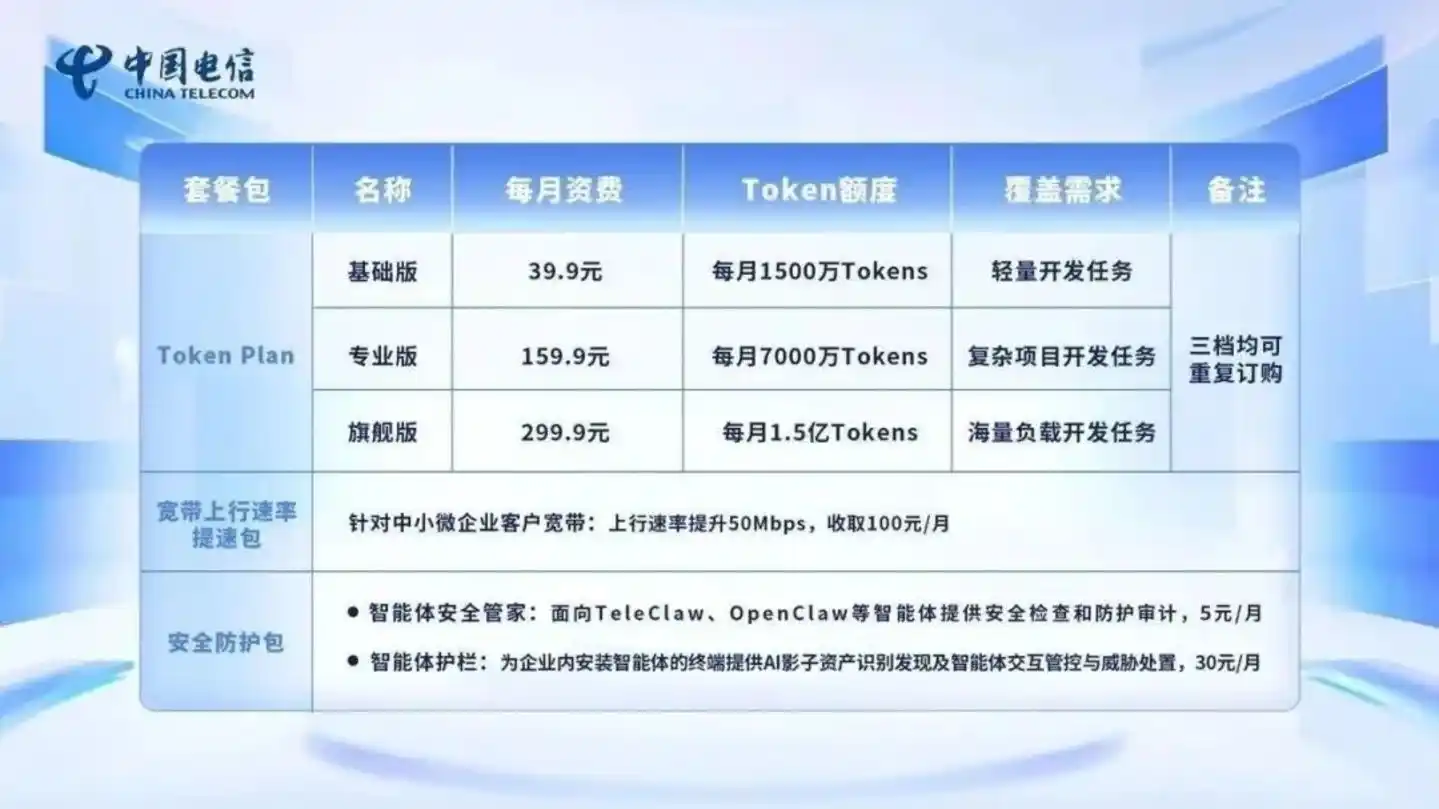

On May 17, China Telecom announced the nationwide trial launch of commercial Token packages. For individuals and families, the lowest tier is 9.9 RMB/month containing 10 million tokens; for developers and SMEs, three tiers are set at 39.9 RMB, 159.9 RMB, and 299.9 RMB, corresponding to monthly allocations from 15 million to 150 million tokens.

This means that Tokens are taking over from voice, SMS, and data traffic, becoming the fourth basic communication service measurement unit for the three major telecom operators. From "selling traffic" to "selling Tokens," operators are striving to reshape themselves into the "National Grid" of the AI era.

Behind this change lies the operators' second identity reconstruction in thirty years. The first leap occurred in the cloud computing era, where operators squeezed into the top tier of government and enterprise cloud services by relying on "controllability + security + state-owned enterprise status"; the second leap is happening right now, as they are transforming themselves from "government and enterprise cloud suppliers" into "total integrators of AI access services."

As the curtain rises, a series of ultimate questions concerning the fate of the industry follow: What kind of chess game are the operators really playing? What is the underlying logic forcing this self-revolution? What changes are required to shift from "selling cloud" to "selling Token"? How will these changes happen? And where will this thirty-year foundation-shaking role reconstruction ultimately lead the operators?

I. Telecom Operators: Collectively Renovating the "AI Gateway"

For the past thirty years, operators' trump card has been integrating communication resources. Facing the AI era, this logic is being upgraded to integrating AI resources and selling Tokens. To truly implement complex AI capabilities, the traditional communication gateway is no longer sufficient; it must be renovated into a brand new entry point: the Token package.

It can be seen that the three operators have all entered the arena, beginning to reorganize their AI service entry points around Token packages.

China Telecom bundles Tokens, connectivity, and security together. Packages for individuals and families start from 9.9 RMB/month, while independent tiers are set for developers and SMEs. User access is no longer limited to traditional cloud platforms; they can be used via the eCloud website, the China Telecom App, or accessed through the Tianyi AI Cloud Computer with built-in intelligent agents.

China Mobile is advancing simultaneously at both local branch and group levels. Beijing Mobile has launched a 5.99 RMB one-time package and a 24.99 RMB/10 million Tokens monthly package; Shanghai Mobile, in collaboration with Tencent, launched the WorkBuddy intelligent agent workspace, where 1 RMB can buy 400,000 Tokens, and payment can be made directly through phone credit. At the group level, China Mobile launched MoMA, accessing over 300 models, and by utilizing intelligent routing, caching, and Token compression, has reduced unit Token costs by approximately 30%.

China Telecom has further upgraded the Token Plan into a combination of "MaaS + Tools + Computing Power." eCloud and Yuanjing (Vision) provide access to models like DeepSeek and MiniMax for individual users, adopt flexible Credits-based billing for team editions, and serve R&D teams, government/enterprise office work, and industry solutions.

What is the reason behind this great migration from integrating "connectivity resources" to "computing power and model resources"?

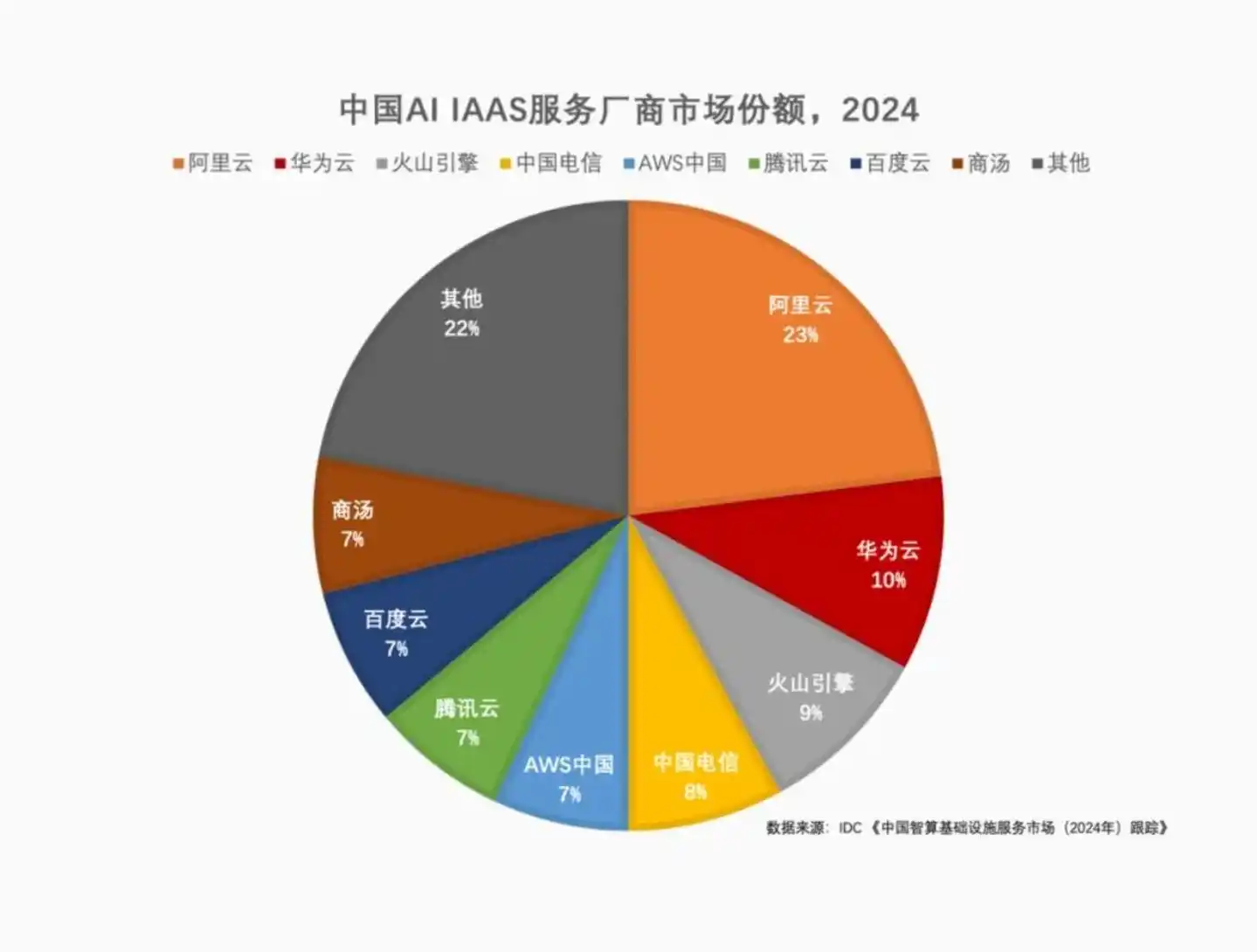

First, look at the market position. IDC's 2024 China AI IaaS market share shows Alibaba Cloud at 23%, Huawei Cloud 10%, Volcano Engine 9%, China Telecom 8%, with Tencent, Baidu, AWS China, and Sensetime all at 7%. While operators have entered the Top 5, there remains a clear gap from the top tier.

According to data from Omdia's "China AI Cloud Market, 1H25," by the first half of 2025, market share further concentrated towards leading cloud vendors. Alibaba Cloud held 35.8%, Volcano Engine 14.8%, Huawei Cloud 13.1%, Tencent Cloud 7%, Baidu AI Cloud 6.1%. Operators had dropped out of the Top 5. This means that if operators cannot demonstrate capabilities in a "telecom-specific track," their share in the AI cloud market will continue to be diluted.

More critically, internet giants have already turned model services into packages that users can understand and purchase more easily. For example, Alibaba Cloud's Bailian launched Token Plans, using Credits to deduct multi-model consumption uniformly; Tencent Cloud's Large Model Token Plan offers Lite, Standard, Pro, and Max tiers, with 39 RMB/month buying 35 million Tokens; Baidu's Qianfan Coding Plan comes in two subscription tiers: 40 RMB and 200 RMB.

This shows that the packaging of Tokens is no longer just a billing method in the developer market, but is becoming the universal packaging for AI services moving towards the mass market.

Beyond external pressures, the operators themselves have reached a point where a gear change is imperative.

Data shows that in 2025, China Mobile's revenue was 1050.2 billion RMB, a year-on-year increase of 0.9%; China Telecom's operating revenue was 529.6 billion RMB, basically flat; China Unicom's revenue was 392.2 billion RMB, a year-on-year increase of 0.7%. The three operators' core businesses remain massive, but growth elasticity is diminishing.

Meanwhile, computing power and intelligent business are becoming new growth engines. China Mobile's intelligent computing service revenue grew by 279%, China Unicom's AI business revenue grew over 140%, and all three operators have increased their computing power investment ratio to over 30% for 2026. The growth focus is shifting from traditional communication services to computing power, models, and intelligent applications.

The problem is that competing in AI cloud is no longer just about data centers, dedicated lines, and GPUs. It's about model capabilities, computing power scheduling, inference costs, developer ecosystems, industry applications, and service response speed. If operators remain in the stage of "selling resources," they will be squeezed by internet cloud vendors, model companies, and industry software providers simultaneously.

Therefore, operators must build a new gateway: supporting large models from above, mobilizing computing power resources from below, and using Token packages to connect users, developers, and enterprises in the middle.

II. From Cloud to AI: What Are Operators Changing?

So, what exactly does the blueprint behind this "new gateway" look like? For operators, what complex industry elements need to be integrated to leap from "selling traffic" to "selling Tokens"?

The answer depends on the changing demands of customers.

In the past, when enterprises migrated to the cloud, they bought servers, storage, and networks from operators; today, for AI implementation, what enterprises want is definitely not an isolated model API, but a complete system covering model invocation, computing power scheduling, application access, and unified billing. This forces operators to upgrade from being mere "cloud product shelf sellers" to becoming "total integrators building the AI gateway."

Therefore, the first thing to integrate is models. Connect multiple general-purpose models, industry-specific models, self-developed models, and third-party models into a unified entry point, allowing enterprises to complete model invocation, switching, and management through a single API or platform.

Secondly, computing power must be integrated. AI computing power is more complex than cloud computing resources, involving AI computing centers, domestic chips, GPU resources, heterogeneous scheduling, cross-regional networks, and inference cost control. Operators need to turn dispersed computing power across different regions, chips, and platforms into a schedulable, billable, and guaranteed computing power network.

Thirdly, applications and intelligent agents must be integrated. Enterprises buy AI ultimately not to call models, but to transform business processes. Customer service, marketing, R&D, production, operations and maintenance, approvals, risk control, knowledge management—these are the real implementation points. Models themselves are just underlying capabilities; only when packaged into industry-specific intelligent agents, toolchains, and Skills packages can they enter an enterprise's daily systems. Therefore, operators cannot just provide model APIs; they must also build the large model capabilities into application foundations for industries like government affairs, central state-owned enterprises, energy, transportation, finance, healthcare, and education. They need to help enterprises solve the problem of "how AI truly enters the business."

Fourthly, billing and operations must be integrated. This is where Token packages truly add value.

It's important to understand that different models, different computing power, and different intelligent agent tasks were originally difficult to fit into a single pricing system. One Q&A session, one code generation, one document processing, one intelligent agent execution—each consumes different models and computing power behind the scenes. For enterprises, if each item needs to be purchased, settled, and managed separately, the barrier to use becomes very high. Operators need to package these complex resources into simple packages. Based on this, users don't need to understand the complex chain behind each call; they only need to know how many credits they've bought, which scenarios they can be used for, and how usage beyond the quota will be billed. This helps enterprises solve the problem of "whether AI can be managed at scale."

In summary, this "renovation" is essentially a way for operators to reconstruct AI services: using models to open the capability gateway, using computing power to support the underlying supply, using intelligent agents to handle business scenarios, using packages to complete the commercial loop, and using security and compliance to uphold the trust of government and enterprise customers.

III. Operators: Positioning as the "Scaffolding" of the AI Era

Deconstructing the top-level logic is just the first step. When ideals are reflected in reality, more challenging implementation dilemmas emerge for the industry: faced with such a complex ecosystem of computing power, models, and applications, how exactly should operators proceed?

What can be seen is that operators are building an end-to-end "five-layer scaffolding" consisting of a model layer, computing power layer, application layer, billing layer, and security & compliance layer.

Looking at the specifics, the core of the model layer is controlling the entry point.

Operators are well aware that relying solely on self-developed models is unlikely to comprehensively catch up with top internet giants, and it's not necessary. Therefore, they have adopted a strategy of "self-developed base models for security + external model aggregation." China Telecom's Xingchen, China Mobile's Jiutian, and China Unicom's Yuanjing are responsible for securing the basic needs of industry adaptation and autonomous controllability; meanwhile, mainstream models like DeepSeek, Tencent's Hunyuan, Alibaba's Tongyi Qianwen, ByteDance's Doubao, Zhipu GLM, and Kimi are also being integrated into unified platforms.

Taking China Mobile's MoMA as an example, "Model Federation + Intelligent Routing" allows users on the front end not to perceive which model is being called in the background; the system automatically distributes tasks based on requirements, cost, and effect. Essentially, the goal is for all models to be distributed through the operators' entry point.

For models to flow, they must be supported by underlying computing power. The computing power layer is also where operators have the greatest opportunity to build a moat.

It's important to know that operators hold assets like East-West Computing hubs, backbone networks, dedicated line resources, government/enterprise networks, and long-term capabilities in building computing power networks—capabilities that cannot be replicated short-term. This gives them a significant advantage in unified scheduling across hubs and different chip architectures. It can be seen that operators are connecting domestic chips, existing NVIDIA inventory, and heterogeneous resources from multiple computing power companies into a single network, forming a barrier that is difficult to breach. Examples include China Telecom's "One Cloud" and China Mobile's "Xingluo" computing network brain.

Above computing power lies applications and intelligent agents.

To truly get processes like customer service, office work, marketing, R&D, O&M, approvals, and risk control running, operators are beginning to promote the standardization of intelligent agent frameworks, such as MobileClaw, TeleClaw, Uniclaw, etc., paired with industry Skills packages. This is equivalent to creating an "AI App Store" for central state-owned enterprises and government clients, allowing AI capabilities to be quickly assembled into existing office and production systems, thereby helping enterprises solve the problem of "how AI enters the business."

To get applications flowing and to accurately account for high-frequency, complex invocations, operators are leveraging their critical innovations stemming from three decades of billing (Billing) and CRM systems. They are introducing mechanisms similar to "Tianyi Token Coins," abstracting the consumption of different models and computing power into a unified billing unit, directly and seamlessly translating the old logic of "data packages" into the logic of "Token packages." This is the underlying reason why Token packages can be rolled out nationwide almost overnight.

The final step in the commercial loop is trust.

Leveraging their "state-owned enterprise" status, operators naturally dominate the central state-owned enterprise computing power pools. Through layers of reinforcement like Multi-Level Protection Scheme (MLPS), IT Application Innovation (信创), and trusted data spaces, they have built a "government and enterprise reserved track" that internet vendors find difficult to penetrate.

Now, based on this "scaffolding," operators have already spread their capabilities quite widely on the capability side.

For example, by the end of 2025, China Telecom already possessed 43 EFLOPS of its own intelligent computing power, accumulated over 110 industry-specific large models and over 350 intelligent agents, served 37,000 clients, and achieved an AI penetration rate as high as 85% among central state-owned enterprises; China Mobile's intelligent computing scale reached 61.3 EFLOPS, its MoMA platform aggregated over 300 models, and reduced unit Token costs by approximately 30%; China Unicom is also moving towards its goal of 45 EFLOPS of intelligent computing, with data showing its AI revenue year-on-year growth soaring to 147%.

IV. Under Token Economics, Operators Go All-In on AI

Musk once made a judgment: in the future, Tokens will be consumed like data traffic.

Looking at this statement today, it is not just an imagination of AI usage methods, but a prediction of a new industry measurement logic. Shifting focus from the operators' "self-reconstruction" to the broader market, a new industry landscape driven by Tokens is unfolding.

Over the past two years, the main theme in the AI industry has been the model competition. Whoever had more parameters, stronger inference capabilities, more complete multimodal abilities, was more likely to gain market attention. However, as we enter the industry implementation phase, the focus of competition is changing. What enterprises truly care about is no longer just how smart a particular model is, but whether it can integrate into existing systems, handle business stably, have clear costs, and be audited and managed.

The bottleneck becomes how to turn models into production capabilities that are usable daily, continuously purchasable, and risk-controllable for enterprises. Low-barrier, purchasable, quantifiable intelligent capabilities will become a necessity.

The gateway renovated by operators happens to place models, computing power, networks, security, and billing into the same entry point, allowing enterprises to purchase intelligent capabilities like they purchase communication services and cloud resources, without having to re-understand a whole complex AI technology stack. This is the true industrial value of Token packages. On the surface, they are credits; but behind them, they may become the measurement unit, settlement unit, and operational unit for AI services.

It is foreseeable that today's Tokens are still like a general-purpose package; in the future, they will likely continue to differentiate into office packages for employee efficiency, developer packages for R&D teams, dedicated model packages for central state-owned enterprises and government scenarios, and industry-specific intelligent agent packages for finance, energy, transportation, healthcare, and education.

However, although the prospect of "buying Tokens as easily as topping up phone credit" is enticing, there is still a long way to go before it truly works smoothly. Operators still face several hard problems, such as whether model performance is good enough, whether intelligent agents can stably complete tasks, whether inference costs can continue to decline, whether customers are willing to pay for long-term use, and whether these investments can ultimately translate into substantial revenue.

Therefore, the decisive factor for operators does not lie in who launches a Token package first, nor in how low the package price is, but in whether they can turn "AI access" into a measurable, billable, operable, and guaranteed telecom-grade service. If this step succeeds, the operators' role in the AI industry will no longer be just selling cloud resources, dedicated lines, or computing power pools; they will become the trusted infrastructure providers in the process of industrial AI implementation.

By then, for enterprises, AI might no longer be a new technology requiring repeated justification, but rather become a producible factor of production that can be accessed, billed for, and continuously used, just like water, electricity, and the network.