Since 2017, large-scale ambushes have emerged and the fittest have been eliminated in the wheel of the times. Until this year, the public chain has ushered in a collective outbreak, from Polkadot, a cross chain network of slot auction, to many emerging public chains such as Solana, avalanche and Cardano. Ethereum has created a public chain with great competition demand, giving birth to greater market opportunities.

More than 100 public chain projects are common and cross chain, which is a new trend

At present, there are more than 100 active public chains, which can be divided into single chain and cross chain according to the attributes of the chain, and the cross chain is represented by Boca and has become the mainstream trend of this era. Overall, the number of public chains has formed a certain scale, and the competition is quite fierce.

1、Solana

Solana started the upsurge of public chain. What's the difference between them?

Solana's fire has directly stirred the upsurge of the public chain camp, including avalanche, fantom, near and so on. The market pays more attention to the public chain, and both capital, project parties and developers are full of interest in this track. So, what are the differences between them?

In terms of technical architecture:

Solana: poh clock scheme

Different from most pieces + eth2 0 scheme, Solana created a unique and innovative poh clock mechanism in the public chain circle The scheme decouples the block out time and state. In terms of global consensus, it is not limited by the hard requirements of block size and block out time. Through the global clock, a globally available time chain is generated for all nodes. The state update can be carried out asynchronously. The verifier can send state updates to other nodes in real time. The poh clock gives the participants of Solana ecology more expandable space, Further improve and expand the overall throughput capacity.

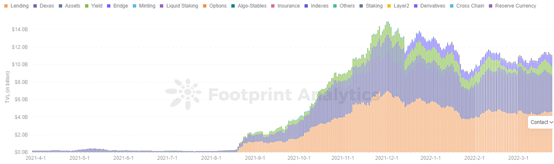

Lock data

Sol's lock up scale has been pulled back from a high level, with a peak of US $15 billion in 2021. On March 24, the scale of lock up reached US $7.34 billion, and there is a large space for data callback of lock up volume.

In terms of the proportion of lock up on the sol chain, the proportion of loan lock up and decentralized exchange lock up is relatively large, while the scale of loan, pledge and mining lock up is small. According to the latest data on March 24, the decentralized exchange locked positions of US $2.76 billion, while loans, pledges and mining were US $1.17 billion, US $1.65 billion and US $1.4 billion.

Token price

The linkage effect between slol price and lock volume is good, and the sol price has dropped from a high of more than $240 to a minimum of $80. The current price on March 24 is $102. In the later stage, we can pay attention to the ecological development, as well as the trading opportunities of the upward lock up volume and price recovery.

2. Avalanche: three chain structure

Avalanche agreement entered the public view by means of incentives, and realized the sharp rise of currency price and lock up volume. Similarly, as a smart contract platform, avalanche is very novel in architecture design and adopts the three chain structure of X chain, C chain and P chain. X chain is a transaction chain, which mainly deals with point-to-point asset creation and transaction transactions between individuals; C-chain is a smart contract chain compatible with EVM, and the basic defi projects are built on C-chain; P chain is a platform chain, which is mainly responsible for token pledge, coordinating network verifiers, creating user-defined subnets and other affairs. The three chains perform their respective functions, but complement each other, further liberating avalanche's network performance.

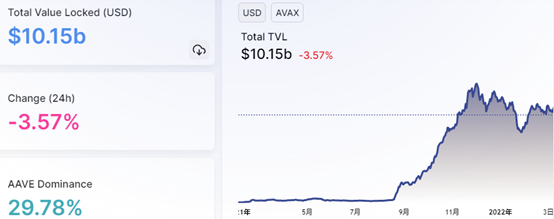

Lock data

Avax lock up data increased by leaps and bounds in 2021. The data rebounded from a low of $2 billion to a maximum of more than $14 billion, with a growth space of more than six times. The current TVL value is US $10.15 billion.

In terms of the proportion of avax chain lock, the proportion of lending, lock and decentralized exchange lock is relatively large, while the scale of mining and cross chain lock is small. On March 24, the loan lockup reached its peak. The scale of loan lockup was US $4.6 billion, that of decentralized exchange lockup was US $4 billion, and that of mining and cross chain lockup was US $900 million and US $1.1 billion.

Token price

Avax experienced great growth in 2021, rising from $15 in August 2021 to a high of $135. From the second half of 2021 to the beginning of 2022, the price of avax remained around $85. Compared with the vicinity of TVL's decline, there is more room for price correction. Next, we can focus on low absorption opportunities.