当 FTX 帝国轰然崩塌之前,99.9%的人都觉得:也许他存在很多关联交易,也许他扩张过快,但崩溃“不是那么可能吧”?

毕竟它的形象是如此光鲜,是加密世界与监管沟通的领头人,是许多机构用户的第一选择,是当下大量知名项目的领投者。而就在崩溃之前的几天,SBF 还慷慨花费600万美金,补偿几个因为API KEY泄露受到损失的散户,尽管责任可能并非FTX,而是第三方软件。

当 CZ 与 SBF 互相宣布币安收购 FTX 的消息时,大家才反应过来:我的天,原来他真的出事了。

当随后 CZ 表示 FTX 财务状况过于糟糕而放弃收购时,大家才终于明白,FTX 完了。

FTX 帝国崩溃的原因究竟是什么?

随着更多信息的揭露,我们发现答案竟然如此简单,和三箭资本并无二异:借了太多钱,在 Luna 事件中崩溃,无法偿还,只能挪用用户资金。

据华尔街日报报道,在加密对冲基金 Three Arrows Capital 三箭资本于 6 月倒闭后,Alameda 面临贷方的一连串要求。

在香港时间周三晚些时候与 Alameda 员工的视频会议中,Alameda 首席执行官 Caroline Ellison 表示,她、Bankman-Fried 先生以及另外两名 FTX 高管 Nishad Singh 和 Gary Wang 都知道将客户资金发送给 Alameda 的决定。Singh 是 FTX 的工程总监和前 Facebook 员工。曾在谷歌工作的 Wang 先生是 FTX 的首席技术官,并与 Bankman-Fried 先生共同创立了该交易所。

Caroline Ellison 表示,FTX 使用客户资金帮助 Alameda 偿还债务。大约在今年春天加密货币市场崩溃的时候,贷方开始收回这些贷款。但 Alameda 花掉的资金不再容易获得,因此该公司使用 FTX 客户资金进行支付。

SBF 对纽约时报的解释则是,Alameda 在 FTX 上积累了大量“保证金头寸”,这实际上意味着它从交易所借了资金。“它比我想象的要大得多,”他说。“事实上,下行风险非常大。” 他表示,该头寸规模达数十亿美元,但拒绝提供更多细节。

那么问题来了,为什么在出现漏洞后,没有收缩、弥补,而是继续进行大规模的投放、投资甚至救助所谓的破产企业?对于这一点,目前没有媒体进行详细的解释。

纽约时报报道,当 SBF 今年开始疯狂收购,投资陷入困境的加密货币公司时,他并没有与关键员工分享信息。当他被告知他过度扩张并被鼓励雇用更多员工时,他拒绝了这些建议。

一种可能的判断是,SBF 希望继续构建表面上的扩张,完成融资,以获得更多的资金。

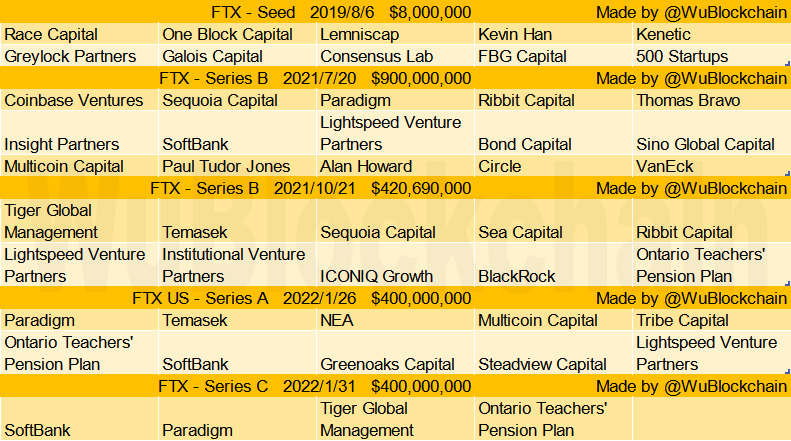

我们可以看到,尽管2022年初就以 320 亿美金的巨额估值完成了4亿美金融资,FTX US 也完成了 4 亿美金融资。但奇怪的是,FTX 仍然继续通过媒体放风,表示正在融资。当时也令外界难以理解。毕竟常规来看,交易所是非常赚钱的业务,为什么需要继续进行融资?

另一种可能的解释则是,SBF 并没有将 Alameda 几十亿美金的漏洞放在心上,他可能并不担心交易所出现挤兑。无论从任何角度来看,他都没有将这一风险放在心上,直到 CZ 开始了攻击。

大家才发现 FTX 竟然如此不堪一击。

FTX 的内部管理问题也是目前普遍认为崩溃的一个原因。正如我们经常批评的一点:FTX 强调他们只有200-300人,甚至在崩溃的前几天,还在吹嘘他们创造了最高的人均收入/利润。但以它一度不逊于币安的生态来说,币安有7000人的员工。显然200-300人是无法妥善管理一个如此巨大的公司。

FTX 决策的不透明与 SBF 的小圈子文化也被认为可能存在问题。内部员工说:“我个人怀疑除了 Sam、Nishad、Gary 和 Caroline 之外的任何人都真正了解正在发生的事情的全貌”。当出现信息茧房的时候,SBF 可能很容易做出错误甚至疯狂的决定。

总结看来:利用借贷进行无序疯狂扩张,内部管理失序,在市场下行时无法偿还,挪用用户资金遭到“吹哨”暴露。FTX 帝国暴雷,其实就是如此简单的原因。

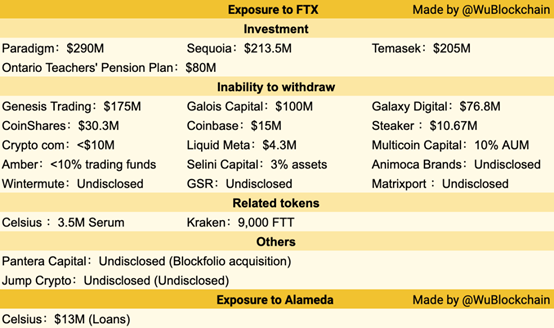

据彭博社,SBF 在申请破产前一天与投资者分享的资料显示,它有近 90 亿美元的负债和 9 亿美元的流动资产,55 亿美元的“流动性较差”资产,以及 32 亿美元的流动资产。其中“流动性较差”资产包括 Serum、Solana 和 FTT。SBF 此前表示兑付了 60 亿美金的资产,还有数十亿美金的缺口。

早在2021年我们描述 SBF 的文章中,就曾以此作为结尾:

“SBF的神奇就在于产业布局之广,执行力之强,超乎寻常人,因此,仅用3年就走完了福布斯榜上大部分人用几十年走完的路。不过,SBF也曾提到,他持有的资产大多缺乏流动性。不知在熊市来临时,SBF能否做到全身而退,亦或只是本轮牛市周期中,昙花一现的“传奇”?”