在很长一段时间内 SBF 都是众人的偶像,因其三个成就而闻名加密圈:

”“

1. 套利交易

2. 创建 FTX 和 Alameda

3. 带来了巨大回报的成功投资(例如$SOL)

”“

在其最高峰时,Sam 的个人净资产曾一度高达 100 到145 亿美元。

”“

在近期,FTX 频繁出手领投包括 Aptos(1.5亿美元)和Sui(3亿美元)在内的多个巨额融资项目。

”“

Sam 曾站在不败之地,即便是 Luna 崩盘带来整个加密货币圈一地鸡毛时,他也能利用当下的市场环境快速扩张:

”“

>注资救活破产边缘的 BlockFi(获得以2.4亿美元价格收购的权利)

>出价买下破产的 Voyager 的所有资产

>尝试注资给破产边缘的 Celsius

”“

然而,在幕后似乎发生了一些不为人知的事情。Alameda 的前 CEO Sam Trabucco突然辞职引起了人们的警觉。一个月之后,FTX 的前总裁 Brett Harrison也递交了辞呈。

”“

事后大家才发现,两位机构的领导者都是在FTX陷入监管机构法律问题泥潭之前匆忙离职。

”“

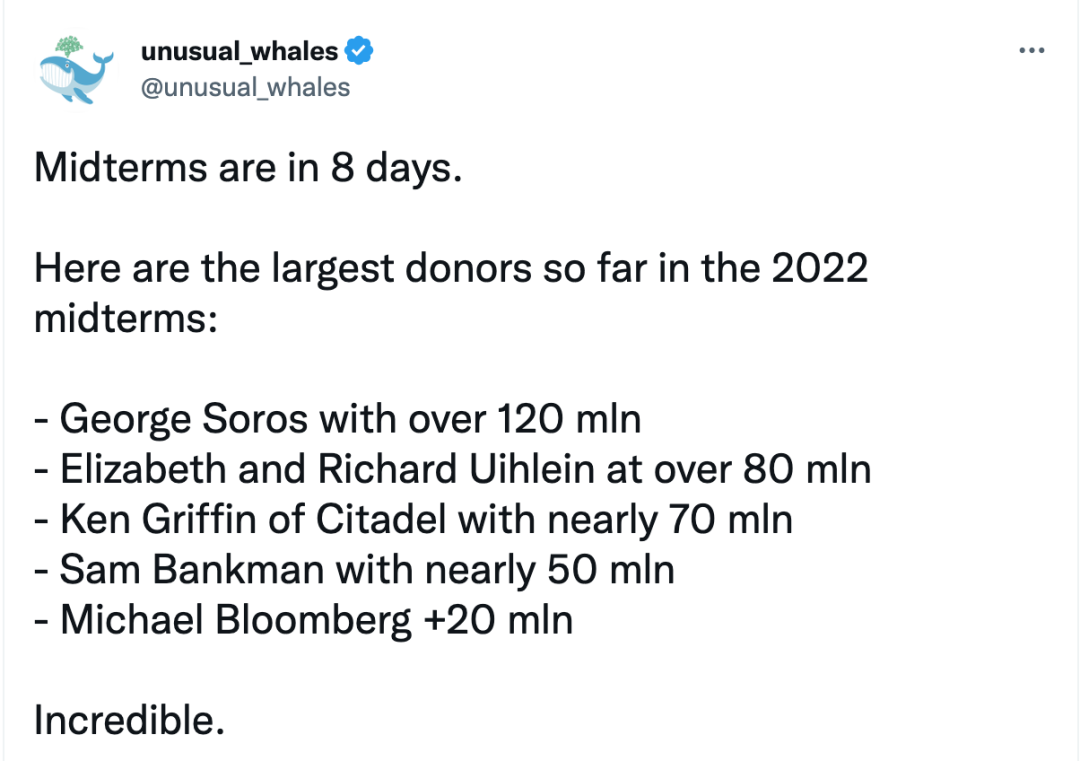

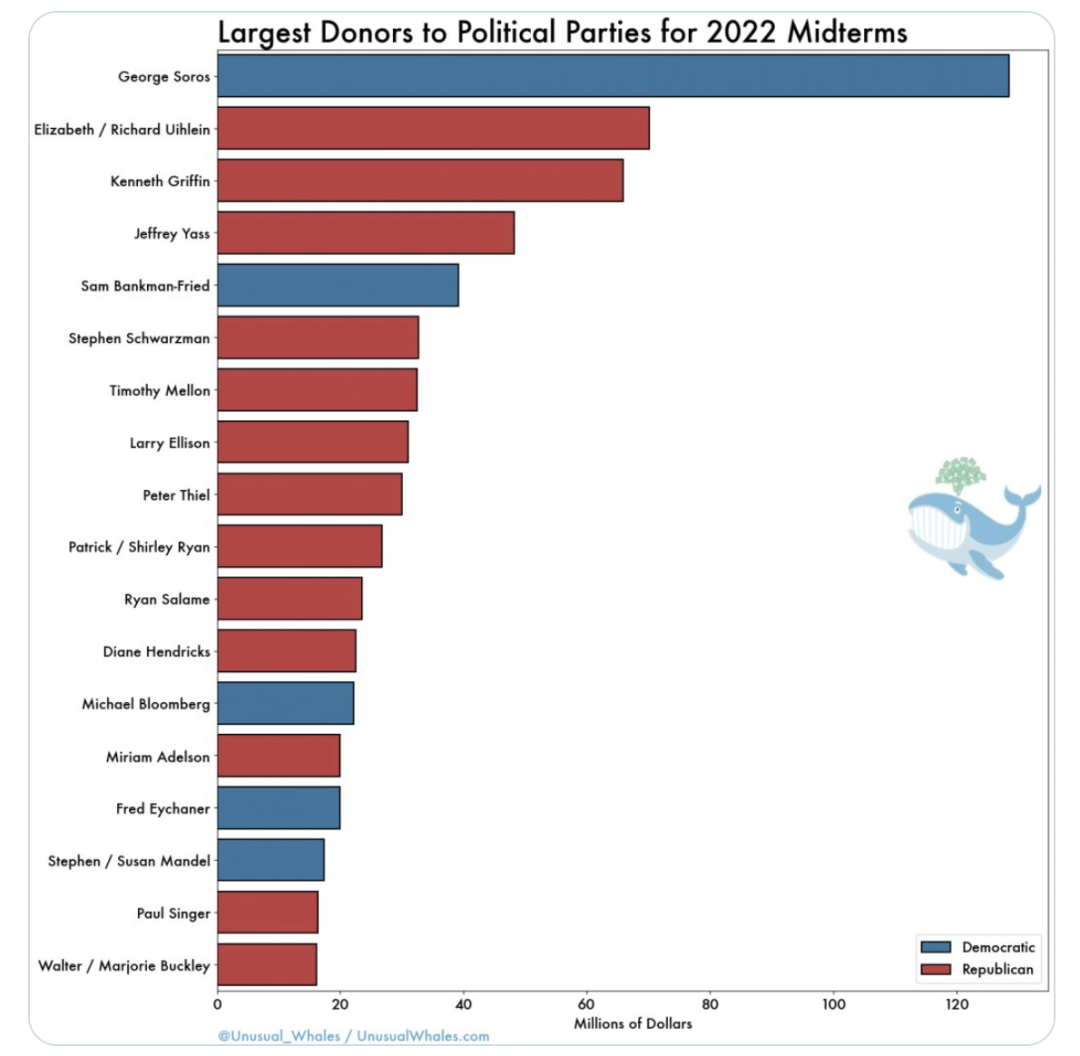

SBF 希望获得政治力量的企图也暴露得很明显 - 在即将到来的 2022 年美国中期选举中,他捐款近 5000万美金。

Sam 甚至公开表示他计划在 2024 年的总统竞选中捐款 (1亿至)10 亿美元,他对他的政治企图没有丝毫掩饰。

”“

尽管此时公众对于 Sam 的态度没有那么积极,但是真正改变大家对其看法的其实是近期在网上被流传的DCCPA - 数字资产消费者保护法案,一个被大家认为可能会几乎杀死去中心化金融整个行业的法案。

”“

从流传的信息中似乎可以看到 Sam 正在为这一法案的设立提供帮助。尽管 Sam 尽最大可能在 Twitter 上给自己增加“行业好人”的戏码,在这个法案中我们可以看到众多对去中心化金融有巨大威胁的信号。

”“

多位加密行业领袖公开对这一法案表示反对,其中最值得瞩目的是一人为大家敲响警钟的Ben Armstrong。

”“

在一期的 Bankless 访谈活动中,Erik Voorhees 也不断追问 SBF 对于监管的真正看法。这段被疯狂传播的视频片段 让整个加密社群对他有了深深的怀疑。

而这一转变便成为为接下来发生的事情的序章,大幅度助涨了社群中的 FUD 负面抛售情绪。

”“

人们意识到了他的初衷似乎和大家所想的并不一样,也迅速转变了对这个曾经加密圈偶像的看法。

”“

周三被泄露的 Alameda 的资产负债表让许多人开始担心其财务状况。如 Cory Klippsten 所言,数据显示SBF 所创立的 Alameda 绝大部分所持有的资产其实都是同为 SBF 所创立的 FTX 的代币,而这一代币同时又被 SBF 的团队以极为中心化的方式管理和增发。

”“

DylanLeClair 也对 Alameda 所流出的资产负债表进行了深入的分析,指出了很多让人所担忧的细节。

Alameda 主要持仓的 FTT 是 FTX 所发行的可以获得交易所内折扣的代币。其总市值仅为 33.5 亿美元,完全稀释市值则为 80 亿美元。对于这样的市场而言,仅仅出售价值 100 万美元的 FTT 代币就会将其整个市场价压低。而 Alameda 持仓的SRM, MAPS, OXY 和FIDA 甚至比 FTT 更差强人意。

”“

我们并不知道 Alameda 的负债是以什么样的形式计价的。如果是美元的话,Alameda 其实面临着巨大的危机,因为其所有的资产都几乎不具有足量的流通性帮助其偿还债务。如果其债务是以其他代币的形式计价的话则形式没有那么严峻,但是依旧不容乐观。

”“

众所周知在三箭资本破产事件中,Alameda 向破产的Voyager 提供了近 3.7 亿美元的借款。我们很难想象,在持有大量不具有流通性的代币资产的同时,Alameda 到底持有多少以 USD 计价的债务。

”“

情况看起来越来越不乐观。FTX 和 Alameda 在今年夏天市场去杠杆的时刻用尽全力展现其羽毛,但是他们是不是那群在即将褪去的潮水中裸泳的人呢?

”“

我并不知道这个问题的答案,但是这个问题值得被人追问和深思。

”“

再来一组更刺激的数据:

Alameda 公布的资产:58.2亿美元的 FTT 代币

FTT 代币当前的总市值:33.5亿美元

是不是很靠谱?

”“

尽管我更希望我们可以拿到 Alameda 官方的资产负债表去核验,但是 CoinDesk 的报告也足够可信了。

”“

而且我认为没被我们发现的幕后故事还有更多。

”“

看到这些,我也似乎懂了为什么 SBF 每周都要在Twitter 上为 FTT 喊单了。

”“

FTX 创造了一个具有巨大完全稀释后市值的代币FTT,而他们鼓励更多人买入代币的动机其实是:99%的代币都被1%的巨鲸账户持有,而最大的持有者则是同为 SBF 创立的对冲基金 Alameda Research,且近期其 VC 部门也被合并到 FTX 之中。

”“

那么… 你认为会发生什么呢 ?