The valuation of the public chain Aptos will reach 2.75 billion dollars if it is not online. The goal of the public chain Aptos is to build a scalable, secure, trusted and scalable smart contract platform.

Unlike Ethereum, which focuses on decentralization and security, Solana extends its performance to the extreme. Aptos tries to find a more balanced position between the two.

With the launch of the main network Aptos Autumn on October 17, the head exchanges simultaneously support the online trading of APT. The Layer1 public chain project APTOS expects that the TPS can reach 160000, and the project ushers in a period of rapid development.

It is worth noting that APTOS is an L1 blockchain, aiming to become the most secure and scalable blockchain in history. At the same time, Aptos was developed by former Meta employees, and its own popularity has become the focus of recent market attention. Of course, the core of its technological innovation is Move, which is based on Rust and can be said to be the fastest network application programming language in the world.

1. Price performance

On October 19, after APTOS was listed and traded in Huabi Global, its price showed a strong performance. After rebounding from the daily level of $7.31, the price rose to the highest level of $10.29.

2. TVL value recovery

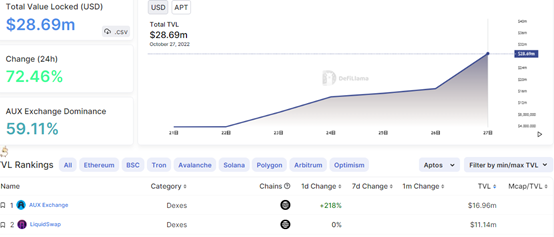

After APTOS was listed on the main exchange, its TVL on the chain also increased rapidly. According to the data on October 27, the data on the APTOS chain showed that there was a locked position worth US $28.69 million, an increase of 726% compared with the 3.47 million on October 21. Among them, AUX Exchange and LiquidSwap have the largest lock positions, reaching 16.96 million US dollars and 11.14 million US dollars, accounting for 97.9% of the total.

3. Aptos Token Economics

At 15:37 Taiwan time, Aptos officially announced its token economy overview on Twitter. The initial total supply of APT was 1 billion. The detailed token allocation is as follows:

Community:

51.02%, 510217359767 (510 million) pieces

Core contributors:

19.00%, 1900000000000 (190 million) pieces

Aptos Foundation:

16.50%, 165000000000 (165 million) pieces

investor:

13.48%, 134782640233 (134 million) pieces

Some 410217359767 (410 million) APTs of the community are held by the Aptos Foundation, and the remaining 100000000 (100 million) APTs are held by Aptos Labs.

In addition, the Aptos Foundation will distribute 410 million tokens within ten years in three types of situations:

125000000 APT (125 million) for ecosystem projects, grants and other community growth plans in support of community categories

5000000 APT to support Aptos Foundation's programs for foundation categories

The remaining 1/120 part of the community and foundation allocated is expected to be unlocked linearly every month in the next 10 years

The number of tokens held by investors is relatively small, accounting for 13.48% of the total number of tokens held, which is 134 million APTs.

From the perspective of the holding time of token holders, the lock in period of core contributors and investors is 4 years.

From the launch of the main network, all investors and current core contributors have a four-year unlocking period. The detailed unlocking conditions are as follows: no $APT will be unlocked in the first 12 months;

3/48 APTs will be unlocked every month from the 13th month to the 18th month (including the 18th month) after the release of the main website;

After the 19th month after the release of the main website, 1/48 APTs will be unlocked every month;

All APT tokens will be fully unlocked four years after the main network is launched.

Therefore, judging from the selling pressure, the market selling pressure of APT has not changed much since the launch of APT in major exchanges recently. In terms of trading volume, APT's trading volume after October 24 was in a shrinking state, which means that APT's price performance was relatively stable. From October 19 to October 24, APT continued to rise in volume, with the closing price rising by 9.32%. After the short-term shrinkage is over, we can continue to focus on low absorption opportunities and wait for the price to break through.