过去一周,Meta(前Facebook)首席执行官马克·扎克伯格可能不太开心。当地时间10月11日,该公司举行年度Connect大会并发布了新一代VR(虚拟现实)头戴设备。这一旨在提振公司元宇宙战略信心的举动,不仅没有带来良好的行业反应,反而引发舆论一波波冷嘲热讽。

《华尔街日报》通过一份Meta内部文件披露,一方面超过50%的Quest头戴设备在购买6个月后不再使用;另一方面,该公司的虚拟社交平台Horizon World月度活跃用户不到20万,与其设定的2022年底之前实现50万目标相去甚远。随后又有媒体曝出,Connect大会上展示的扎克伯格虚拟化身有腿的视频是作假,一位Meta发言人说,其实是用第三方动作捕捉技术,而非更高阶的头显动作捕捉技术来实现的。

分析师、投资机构Seeking Alpha的专栏作者Albert Lin近日撰文称,不看好Meta所描绘的元宇宙,并给出了几大理由。

Meta的CEO马克·扎克伯格一直在积极押注元宇宙,希望为用户创建一个全新的AR/VR生态系统,让他们在虚拟世界中尽情享受。

在2020年第4季度至2022年第2季度期间,Meta的Reality Labs部门的总营业亏损为180亿美元,收入略高于40亿美元。虽然早期的损失是可以理解的,因为扎克伯格表示Reality Labs在本世纪末之前不会成为一个真正的商业故事,但投资者开始质疑Facebook向Meta的过渡是否真的能成为这家社交媒体公司的可持续增长动力。

在本文中,我将讨论为什么Meta的元宇宙可能会失败,并解释为什么投资者不应该押注Reality Labs,认为它是Meta股票的下一个价值驱动因素。

用户并不真正感兴趣

《华尔街日报》最近在 10 月 15 日发表的一篇文章表明,根据内部文件,Meta 的Horizon World(核心元宇宙产品)几乎没有引起消费者的兴趣。最初的目标是到 2022年底达到50万个MAU(月活跃用户),但Horizon World到目前为止只吸引了不到 20万用户。自今年春天以来,Horizon World的用户群一直在稳步下降,大多数用户在第一个月后就不再回到虚拟世界。

这些内部文件还揭示了以下内容:

在该应用程序创建的“世界”中,只有9%的“世界”访问人数超过50人,而大多数的访问者为0。

过去3年,Oculus Quest(Meta的VR头戴设备)的留存率一直在下降,超过50%的Quest头戴设备在购买6个月后不再使用。

不到1%的用户正在构建自己的“世界”。

在对514名用户进行的一项调查中,人们表示他们找不到自己喜欢的“世界”,也找不到太多可以互动的人,头像也看起来很假,“没有腿”。

Horizon World 图片来源:Seeking Alpha

The Verge在另一篇文章报道称,根据Meta的内部备忘录,Horizon Worlds存在太多质量问题,甚至公司员工也没有经常使用它。

在2022年剩余的时间里,Meta元宇宙业务的副总裁Vishal Shah已将Horizon Worlds置于“质量锁定”(quality lockdown)状态。虽然Shah承认元宇宙的潜力,但他给团队的备忘录中的以下内容表明还有很多工作要做。

显然,Meta在说服其产品Facebook、Instagram、Whatsapp和Messenger上超过36亿全球月度用户加入元宇宙时遇到了问题。今年2月,Meta表示Horizon Worlds的月活跃用户数约为30万,但此后一直没有再更新数据。

到目前为止,用户购买Meta Quest主要是用来玩游戏,但眩晕和迷失方向的问题可能会阻止许多游戏玩家长时间使用这款头戴设备。健身是另一个受欢迎的应用场景,但7月,FTC(美国联邦贸易委员会)以反垄断为由以3-2投票阻止Meta收购VR健身应用程序制造商Within。Meta试图驳回FTC的投诉。

得益于与微软的合作,新发布的Quest Pro(10月25日上市,售价1499美元)将可以使用Teams和Office等应用程序的VR功能,但用户是否愿意购买如此昂贵的头戴设备用来工作仍是一个主要问题。

竞争正在升温

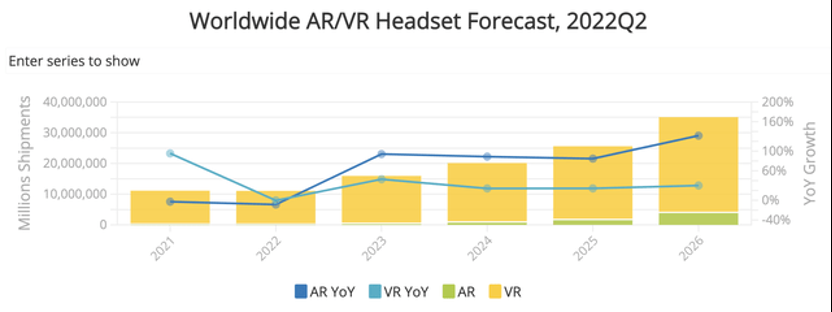

根据IDC的数据,2022年第二季度全球VR头戴设备同比增长32%,Meta继续以86%的份额保持市场领先地位,而中国的Pico(2021年被Tik Tok母公司字节跳动收购)拥有8%的市场份额。尽管鉴于当前的宏观背景,预计2022年全球销量将保持平稳,但IDC预测到2026年的总出货量将从2022年的1080万台增加到3100万台。

IDC 图片来源:Seeking Alpha

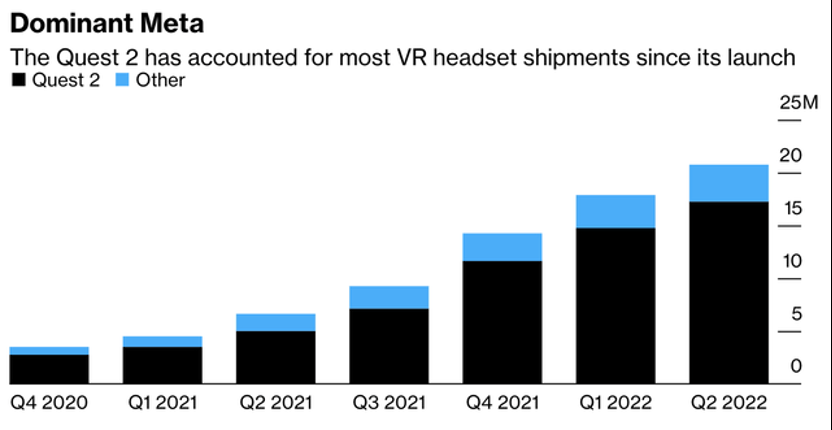

在2022年第二季度结束时,Meta Quest 2占VR头显累计出货量的大部分,为1720万部,而总数为2070万部。显然,Meta目前是VR市场的主导力量。

IDC、彭博 图片来源:Seeking Alpha

成功伴随着竞争。据MacRumors报道,苹果计划在2023年推出其AR/VR头显,售价可能高达2000美元。近年来,苹果一直在招聘AR/VR人才,并收购了该领域的多家公司。据传,这款头显拥有两个M2处理器、4K micro-OLED显示屏,具有虹膜扫描、面部表情追踪等功能。

另一方面,索尼将于2023年初推出其PSVR2,价格可能与PS5游戏机一样高。目前有超过20款来自1P(first-person,第一视角)和3P(third-person,第三视角)游戏开发商的游戏正在开发中。尽管之前的PSVR花了八个月时间才达到100万台销量,而Meta Quest 2第一季度销量为280万台。但因为其改进了眼球追踪、振动和移动镜头等功能,索尼对其VR头显的新设计仍然对Quest构成威胁。

经济学可能没有意义

从商业角度来看,构建元宇宙的最终目标是控制一个拥有庞大用户群的VR平台,并对这个生态系统内的每一笔购买“征税”。这个想法与iOS应用商店和Android的 Google Play非常相似。

苹果从年销售额超过100万美元的开发者那里抽取30%的分成,对低于这个数字的开发者抽取15%。Google Play已将其平台费用从30%降至15%。Roblox从开发者在该平台上的每笔Robux销售中抽取30%的费用。最后,受欢迎的NFT平台OpenSea只收取2.5%。

虽然扎克伯格此前曾批评苹果对应用商店的销售收取30%的巨额费用,他认为这会损害创新,但Meta在4月宣布,它将向开发者收取高达47.5%的元宇宙内销售分成(30%的Meta Quest Store费用 + 17.5%的Horizon Worlds费用)。这显然与激励创新背道而驰。

通过从虚拟世界中销售数字产品的开发人员那里抽取近50%的分成,Meta正在让创作者不要在其平台上投入太多时间和精力,除非用户群太大而无法错过。这将变成一个先有鸡还是先有蛋的情况,如果虚拟世界中没有数十亿用户,开发人员将无法忍受极高的费用。如果没有大量开发者愿意一直创造新的和令人兴奋的内容,用户也不想在虚拟世界中花费时间。

结论

在我看来,扎克伯格对Reality Labs的巨额押注对这家社交媒体公司的弊大于利,因为其虚拟世界正在呈现用户参与度低、竞争加剧和对开发人员缺乏经济吸引力的状态。这就是为什么我长期以来一直认为Meta的股票仍然是一个价值陷阱的主要原因。尽管目前投资者可能将其股票视为2023年市盈率达12倍的深度价值股,目前看似是估值低廉。

尽管Meta计划在未来几个月内将成本至少削减10%,但Reality Labs仍有望在2022年产生130亿美元的总运营亏损。同时考虑到其核心广告业务已经面临增长阻力,Reality Labs的亏损就是拖累利润率的主要因素。尽管投资者可能认为这只股票2023年具有12倍收益的深度价值,但我仍然认为风险多于回报。